Macro Pulse Update 15.06.2024

Macro Pulse Update 15.06.2024

Capo says “…we could see a strong bounce soon.” 💀

Monochrome continually increases their ETF holdings

Altcoins copy 2016/2017 - it just takes longer, so the corrections take longer too.

Here’s what you need to know about the June/July accumulation for summer rally👇🧵

Macro Pulse Update 15.06.2024, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ LATAM Spotlight

1️⃣ Macro events for the week

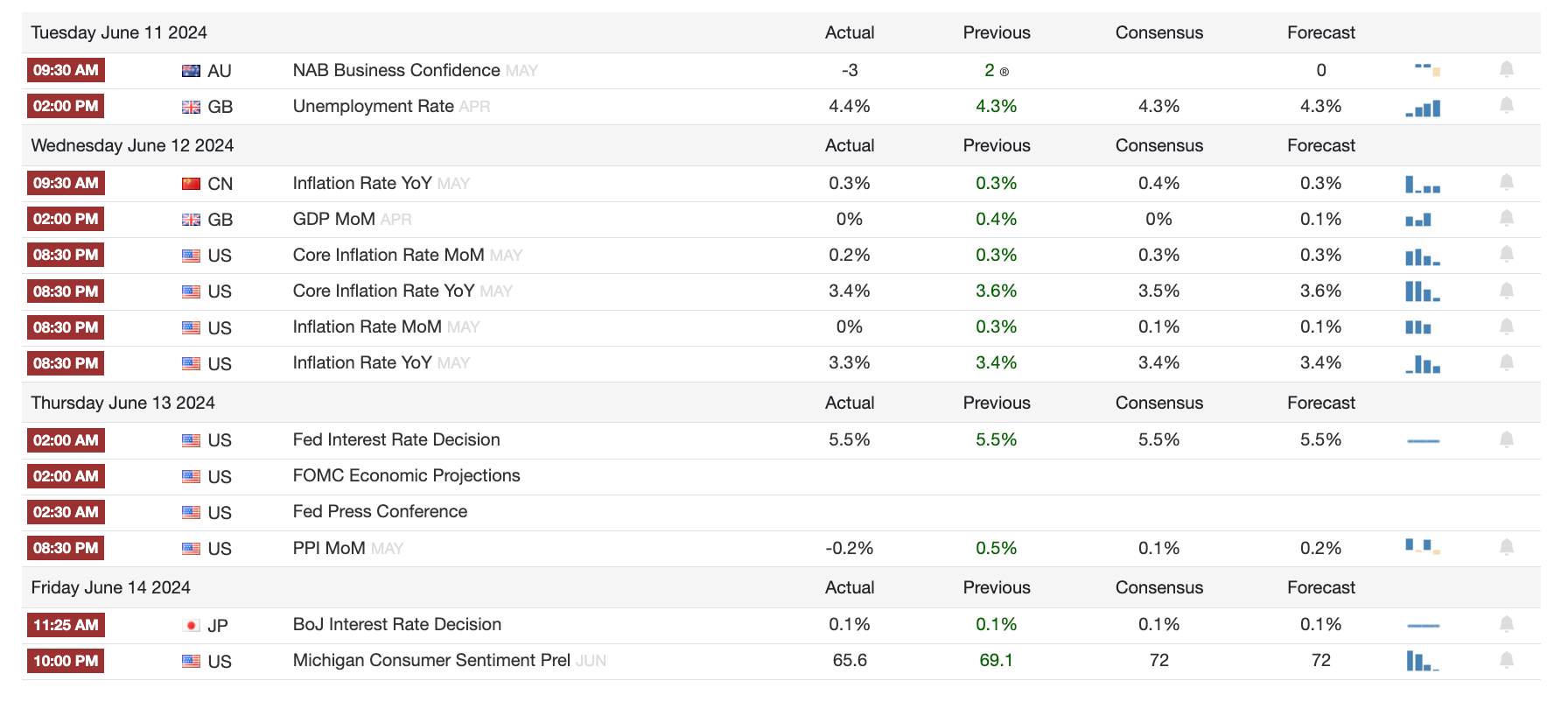

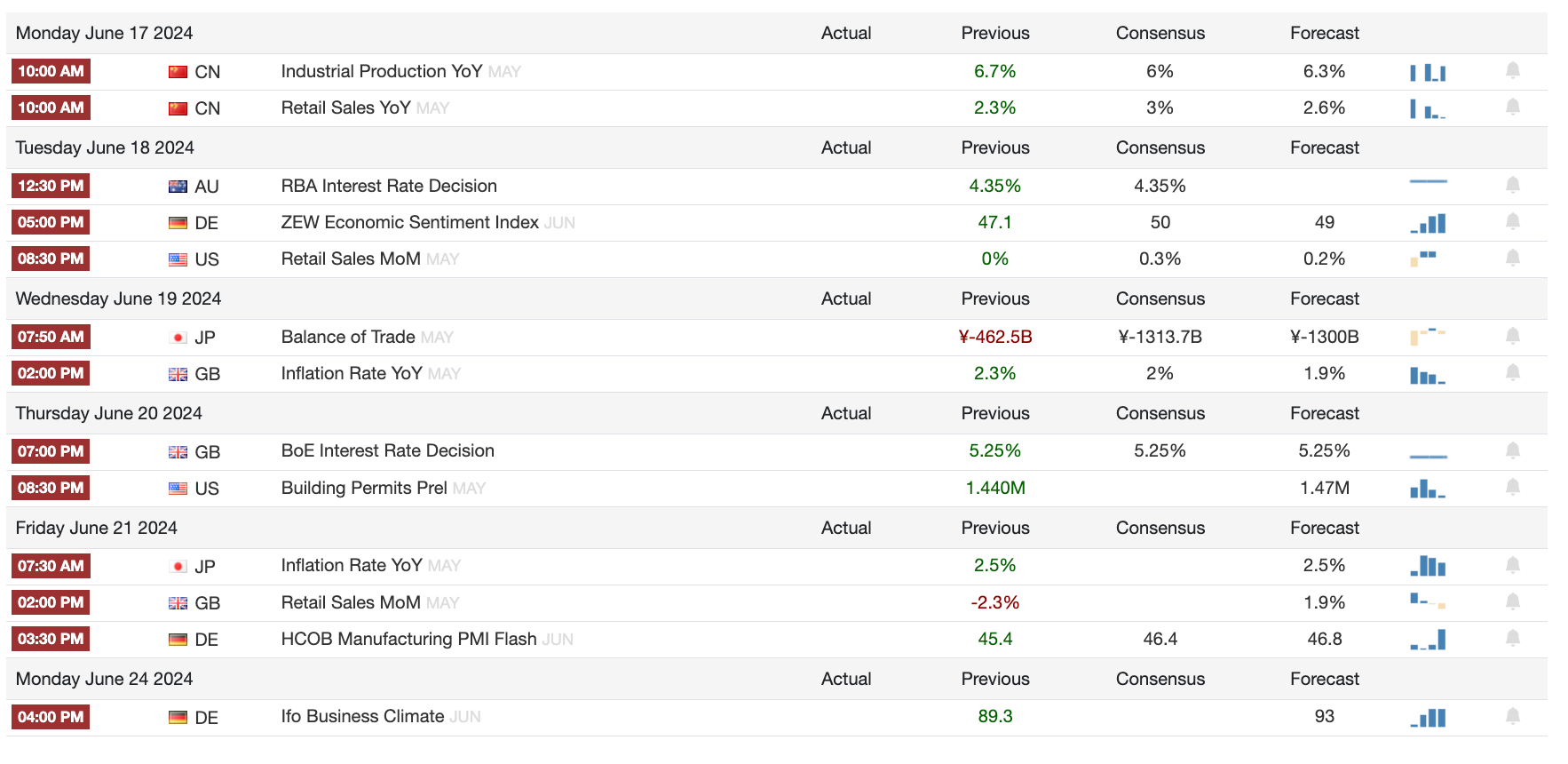

Last Week

Next Week

2️⃣ Bitcoin Buzz Indicator

Major Hacks and Security Incidents

Curve Finance Founder Faces Massive Liquidations

UwU Lend Suffers $19.5 Million Hack

OKX Hit by SIM-Swap Attack, $633 Million Stolen

Holograph Hacked, 1 Billion HLG Tokens Minted

Token and Coin Developments

zkSync Token Launch Faces Backlash Over Airdrop

Andrew Tate's DADDY Coin Surges Amid Insider Trading Suspicions

Blockchain Network and Protocol Updates

Solana Cracks Down on Sandwich Attacks

Terraform Labs Hands Control to Terra Community

Regulatory and Market Insights

Stablecoin Sector Sees Significant Growth

South Korea Introduces New NFT Regulations

NFT Market Trends

Ethereum NFT Traders Drop Below 4,000 Daily

Art and Culture in Crypto

Beeple's Latest Artwork Satirizes Crypto and Celebrity

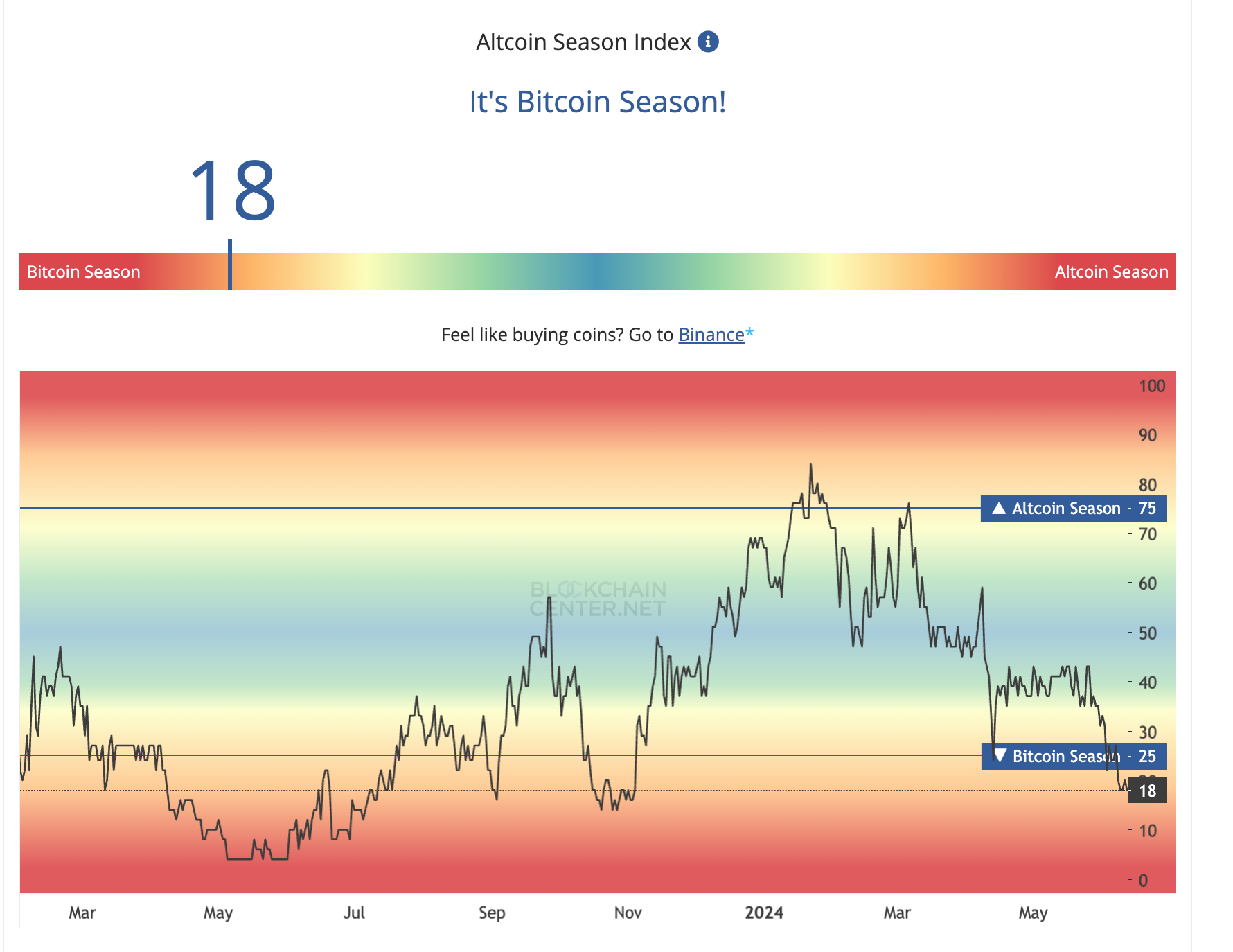

Altcoins

FLOKI celebrated 417,400 holders and planned a major move in India.

io.net's CEO left 2 days before the token launch.

Orbit Chain hacker moved $48M to Tornado Cash after months of inactivity.

Base TVL surged to $8B just days after surpassing OP Mainnet.

Cardano revealed the timeline for Chang Fork, marking the 'Age of Voltaire'.

Wintermute transferred $12M ARB to Binance.

Squads Labs raised $10M Series A and launched a smart wallet for public testing on iOS.

Aevo debuted the AZUR pre-launch contract.

Fidelity International tokenized a money market fund on JPMorgan’s blockchain.

MANTRA (OM) reached an ATH despite market stagnation.

Fireblocks partnered with Coinbase International Exchange for reliable trading.

Friend.tech decided to leave Base for its own blockchain.

Polyhedra Network started staking after resolving a ZK trademark issue.

Whales or institutions accumulated GMX from Binance.

Lykke Cryptocurrency Exchange stopped trading, preventing users from withdrawing assets.

Travala integrated Telegram Open Network.

Optimism celebrated Stage 1 decentralization with permissionless fault proofs.

Loopring smart wallets suffered a $5 million exploit.

Uniswap Labs acquired 'Crypto: The Game'.

Australia banned crypto and credit cards for online betting.

Biconomy onboarded AI agents for onchain transactions.

PancakeSwap integrated Zyfi for gas-free DeFi trading.

Binance Labs invested in Zircuit to enhance L2 with AI-enabled sequencer level security.

Ripple launched a massive fund for XRP Ledger in East Asia.

MultiversX boosted layer-2 transaction speed with Sovereign Chains.

Lido introduced 'Restaking Vaults' in collaboration with Symbiotic and Mellow Finance.

Polygon created a new grants program, unlocking 1B POL over 10 years.

Tether expected to invest over $1B in deals in the next year.

Fetch.ai, SingularityNET, and Ocean Protocol rescheduled their token merger for July 15.

VeChain’s VET and VTHO tokens became tradable on Revolut.

SushiSwap merged DAO with the 'Labs' model and introduced a multitoken ecosystem.

Thai SEC revoked Zipmex’s licenses after non-compliance.

Gnosis DAO chose Swarm for storing blobs, causing Swarm token to surge.

MetaMask introduced a pooled ETH staking service, excluding US and UK customers.

Crypto mixers, privacy coins, and layer 2s complicated tracing for law enforcement, according to the EU Innovation Hub.

Arthur Hayes joined Covalent as an advisor and received compensation in CQT token.

Circle announced Solana programmable wallets and a gas station.

MoonPay announced a PayPal fiat on-ramp for the UK and EU.

Holdstation advanced AI wallet tech with a 7-figure investment from SNZ Capital, Summer Ventures, and EVG Ventures.

Fan tokens rallied as investors bet on soccer fever.

Crypto hacks netted $19B since 2011, and illegal activity on the blockchain kept growing.

Ethena (ENA) whale lost $13 million as the token plummeted 30% in a week.

Ripple announced XRPL EVM Sidechain to enhance blockchain interoperability.

Solana Labs launched a customer loyalty platform.

Polkadot parachain Moonbeam launched a $13M Web3 gaming fund.

Chainlink’s CCIP protocol and automation went live on Gnosis.

Crypto airdrops distributed around $4 billion this year.

Layer3 raised $15 million Series A ahead of token launch and airdrop.

Symbiotic, backed by Paradigm, unveiled a restaking protocol.

Arbitrum planned Stage 2 decentralization with permissionless transaction validation.

Privado ID became the latest project to spin out from Polygon Labs.

The Graph completed the transition to a decentralized data layer.

NEAR Foundation formed Nuffle Labs with $13M in funding.

Eigen Labs acquired Rio Network and opened LRT code.

Manta Network launched a $50M ecosystem fund.

BNB Chain supported early projects with a new incubation alliance.

Trezor aimed to simplify self-custody with onboarding sessions and a new wallet.

Swiss regulator forced crypto-friendly FlowBank into bankruptcy.

Paradigm raised $850M for its third crypto fund.

Taiwan's crypto advocacy body became formally active with 24 entities.

ZapperFi aimed to build ‘road to onchain literacy’ with the Zapper Protocol.

a16z-backed gaming studio's token got listed on Coinbase.

Paxos downsized its workforce by 20%.

RWA Token ONDO surged after Upbit’s listing announcement.

Franklin Templeton highlighted two Solana projects as early ‘DePIN’ winners.

Aethir launched its mainnet on Ethereum.

3️⃣ Market overview

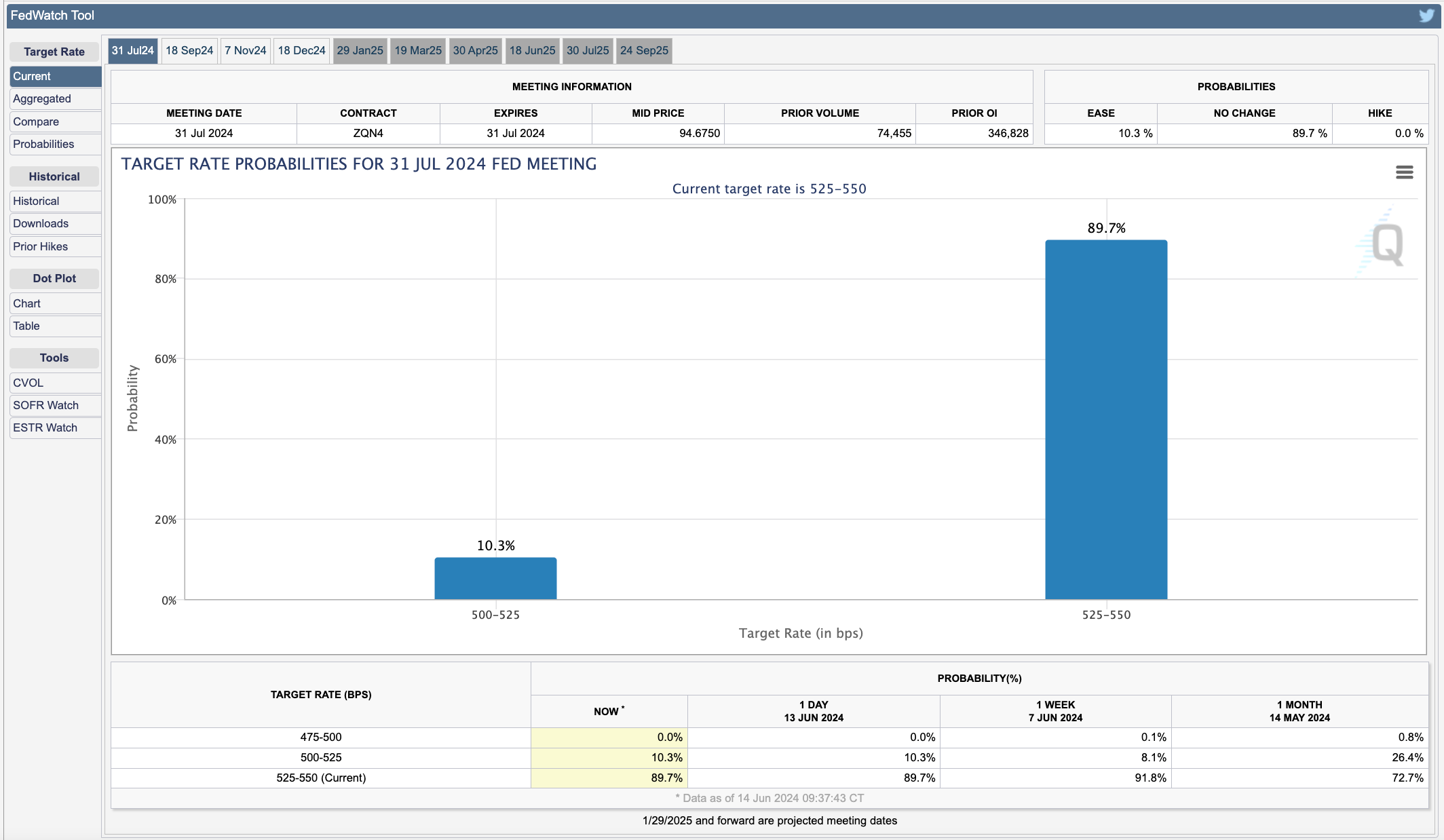

Federal Reserve officials revised their interest rate forecast, now planning only one rate cut for 2024, down from three previously anticipated. They signaled additional rate cuts in 2025, taking a cautious approach to ensure inflation moves toward the 2% target consistently.

While the FOMC maintained rates in June, it has revised its economic projections, with most participants expecting at least some rate cuts before the end of the year. The outlook for rate cuts will depend on incoming inflation and employment data, with the base case leaning towards two 25 bps cuts in September and December.

FOMC Maintains Rates and Revises Economic Projections:

The FOMC kept the target range for the federal funds rate unchanged at 5.25%-5.50% during its June meeting.

The Summary of Economic Projections (SEP) showed most participants expect at least some reduction in rates before the end of the year.

The median projection for the federal funds rate at year-end is now 5.125%, implying one 25 bps rate cut before the end of the year, down from the 75 bps of easing projected in the March dot plot.

The distribution of members' projections is still skewed toward more easing, with eight participants expecting two cuts and only four expecting rates to remain unchanged this year.

Inflation Expectations and Economic Forecasts:

The FOMC revised its inflation expectations, now seeing the core PCE deflator at 2.8% year-over-year in Q4-2023, up from the 2.6% forecast in the March SEP.

This revision is consistent with stickier inflation data at the start of the year but also reflects an inferred stalling in price growth.

The Fed made no changes to its economic forecasts for GDP growth (2.1% in 2024) and expects the unemployment rate to hold steady at 4.0%.

Chair Powell emphasized the totality of the data in determining when it will be appropriate to ease policy and stressed that the committee remains data-dependent with no pre-set policy path.

Outlook for Rate Cuts:

The report suggests it will be a close call between one or two 25 bps rate cuts this year, with the base case leaning towards two cuts - one in September and another in December.

Recent inflation data has increased confidence that the jump in price growth in Q1 was a flare-up and not the start of a more persistent trend.

However, the FOMC needs to see more benign inflation prints before a consensus emerges that a reduction in the federal funds rate is warranted.

The next FOMC meeting is in late July, and there will be three more months of inflation and employment data available before the September meeting.

4️⃣ Key Economic Metrics

While the United States is experiencing cooling inflation, which may lead to potential rate cuts, Japan is gearing up for further policy normalization. Meanwhile, Latin American markets are facing challenges due to political uncertainties in several countries.

🟢 United States:

The May CPI data showed consumer prices remained unchanged, the first flat reading since July 2022, fueling optimism about potential Federal Reserve rate cuts in September.

Core CPI (excluding food and energy) increased by a modest 0.2%, the smallest monthly increase since August 2021.

Upcoming economic indicators to watch include Retail Sales, Industrial Production, and Existing Home Sales.

🟡 Japan:

The Bank of Japan (BoJ) kept its policy steady but signaled the likelihood of further policy normalization in the future.

The BoJ noted the intensifying virtuous cycle between wages and prices and plans to decide on a detailed plan for reducing the pace of its bond purchases.

Expectations are for the BoJ to eventually hike its policy rate, possibly at the October meeting.

🔴 Latin America:

Latin American financial markets, particularly currency markets, experienced pressure this week.

The election surprise in Mexico is seen as the primary cause of the regional market volatility.

Additional policy uncertainty in countries like Brazil and Colombia also contributed to the volatility in local markets.

5️⃣ LATAM Spotlight🔴

Currency volatility, depreciation pressures, and concerns about credit ratings have emerged as a result of these country-specific factors, potentially impacting investment sentiment and economic stability in the region.

Mexico:

The Mexican peso has experienced volatility and depreciation pressure due to the election surprise, with the Morena party and its allies securing a supermajority in both houses of Congress.

A congressional supermajority raises concerns about potential constitutional amendments that could disrupt the democratic process, weaken governance, and impact Mexico's fiscal position.

Investors are questioning Mexico as an investment and FDI destination due to the possibility of a weaker legal system and less fiscal responsibility.

Brazil:

President Lula suggested that raising taxes or finding new revenue sources would be sufficient to ensure fiscal balance, without the need to cut expenditures.

Key cabinet members hinted that fiscal targets, already relaxed earlier this year, may not be achieved.

Financial markets reacted negatively to the indications of eroding public finances, pushing the USD/BRL exchange rate from ~BRL5.00 to ~BRL5.40.

The currency depreciation could lead to higher local inflation in the short term, and the Brazilian Central Bank may need to consider hiking rates again to defend the currency's value.

Colombia:

President Petro has sought to loosen fiscal policy to support economic activity, but concerns have risen about fiscal discipline and the possibility of missing fiscal targets.

The Colombian peso sold off sharply, down ~7.5% year-to-date against the dollar, due to concerns about a wider fiscal deficit.

Colombia risks losing its final investment grade credit rating from Moody's, which could contribute to financial stability risks and further depreciation pressure on the peso.