A(I)cceleration, Multiple Rerating and The Repricing of Time

Macro Pulse Update 28.02.2026

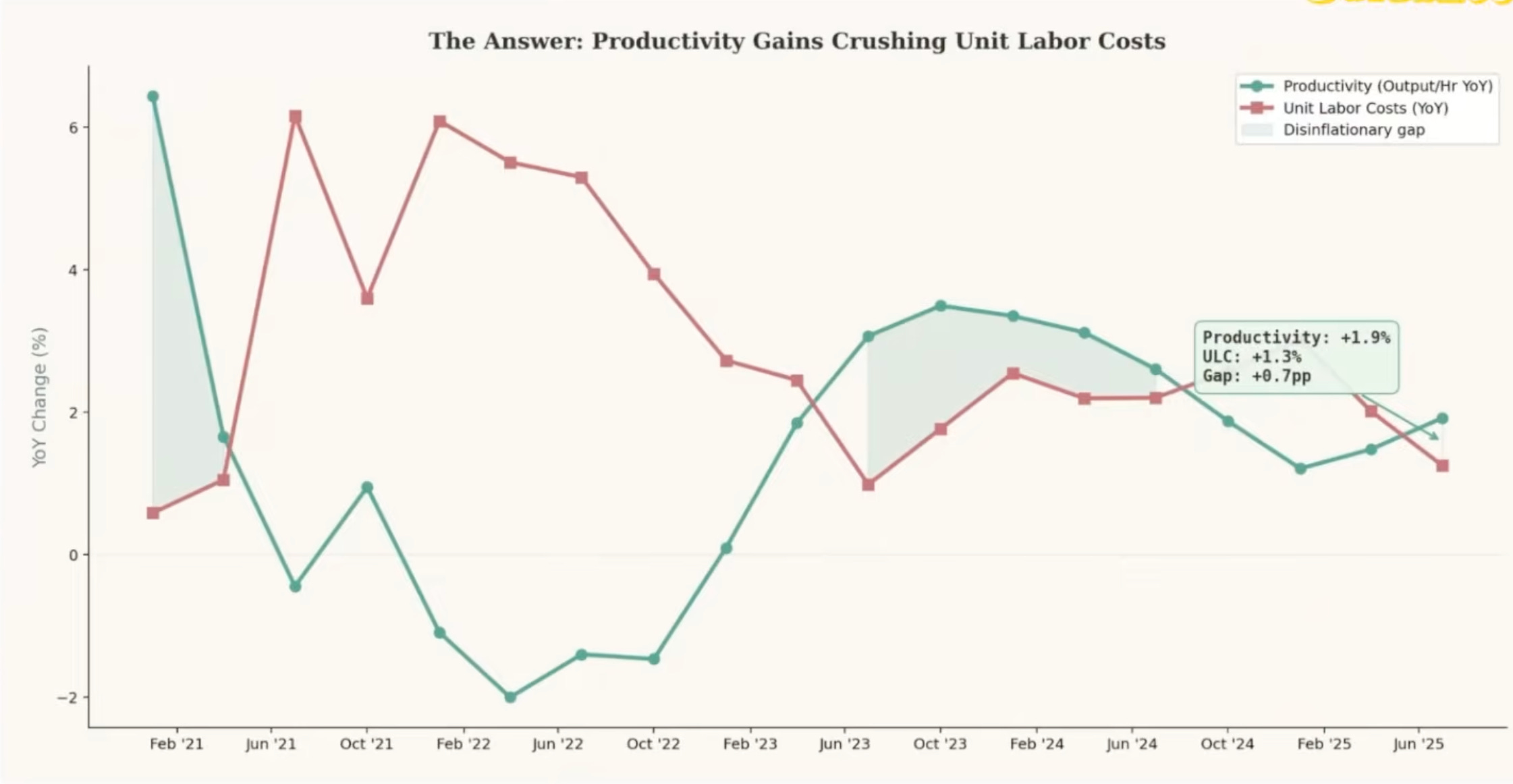

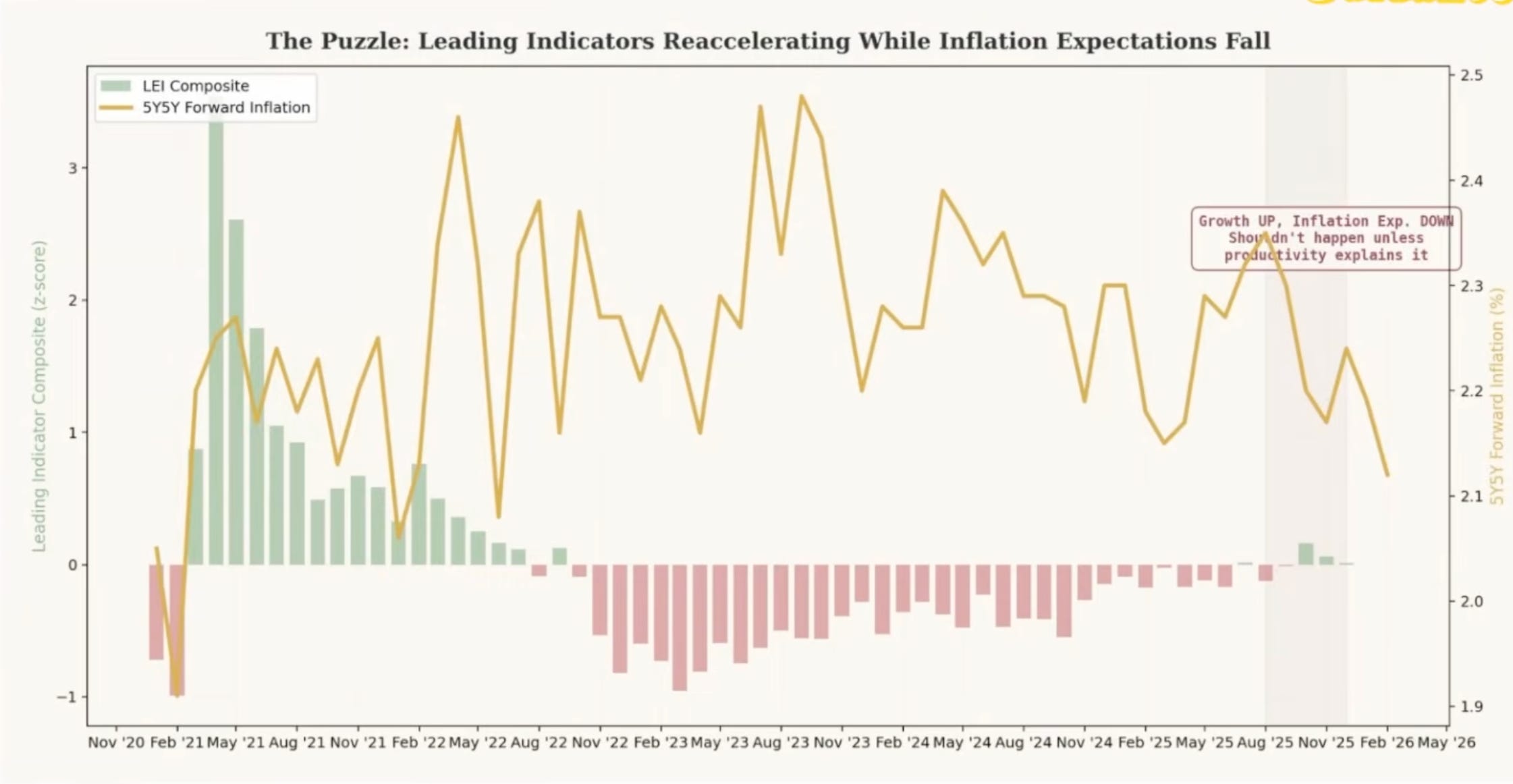

What I’m seeing is that breakevens have been drifting lower at the same time the growth data is starting to re-accelerate. That combination is weird as normally, growth firming lifts inflation compensation.

I’ve seen this pattern in three distinct places that don’t usually get discussed together:

Shenzhen (manufacturing as a learning organism)

AI agents (software compresses economy cycle time)

Macro + markets (repricing labor, margins, and the durability of cashflows)

Work harder → automate more → cut costs → ship faster.

In this AI era, I’m increasingly convinced that’s the wrong model, that framing is already stale.

1) The Shenzhen moment, Redundancy is intelligence

There is much to learn from China and that’s why I am realizing that working harder is the wrong model, it will not catch up to China.

If you actually build in Shenzhen, China, you would stop believing the story that China wins because things are cheaper.

What’s disorienting is how fast the system learns.

You can run multiple prototype iterations in days. The money matters less than the feedback loop:

PCB fab within minutes

component distributor who’s seen your failure mode 100 times

firmware freelancer who can patch a constraint in the real world, not in a slide deck

tooling changes proposed before you ask, because the ecosystem has an in-built anticipatory feedback loop

From the outside it looks redundant.

From the inside you realize that redundancy is information density.

Western systems centralize to reduce complexity. Shenzhen distributes to convert complexity into speed.

The Shenzhen advantage is best understood as an ecosystem-level optimizer:

high node density → low switching cost between specialists

high transaction frequency → fast diffusion of tacit knowledge

parallel supplier graph → constant price/quality discovery

tight physical proximity → compressed coordination overhead

short feedback loops → compounding improvement

Western manufacturing systems typically centralize to reduce variance and enforce control. That reduces complexity on paper, but it increases latency in reality.

Shenzhen does the inverse: it distributes production so that complexity becomes parallelism, and parallelism becomes speed.

Telling the West to work longer hours to catch Shenzhen won’t work.

2) AI as COVID 2.0 where the time constant changes

I think people are still treating AI like a tech-product story. It’s not.

The S&P heavily weights the IT sector at 36%.

It’s a macro shock, because it changes two things marcoeconomic markets care about:

the cost of producing output (effective labor supply)

the speed of adjustment (cycle time of the economy)

2023 ChatGPT was noisy and unreliable, so the macro conclusion was rational with minimal adoption, limited economic impact.

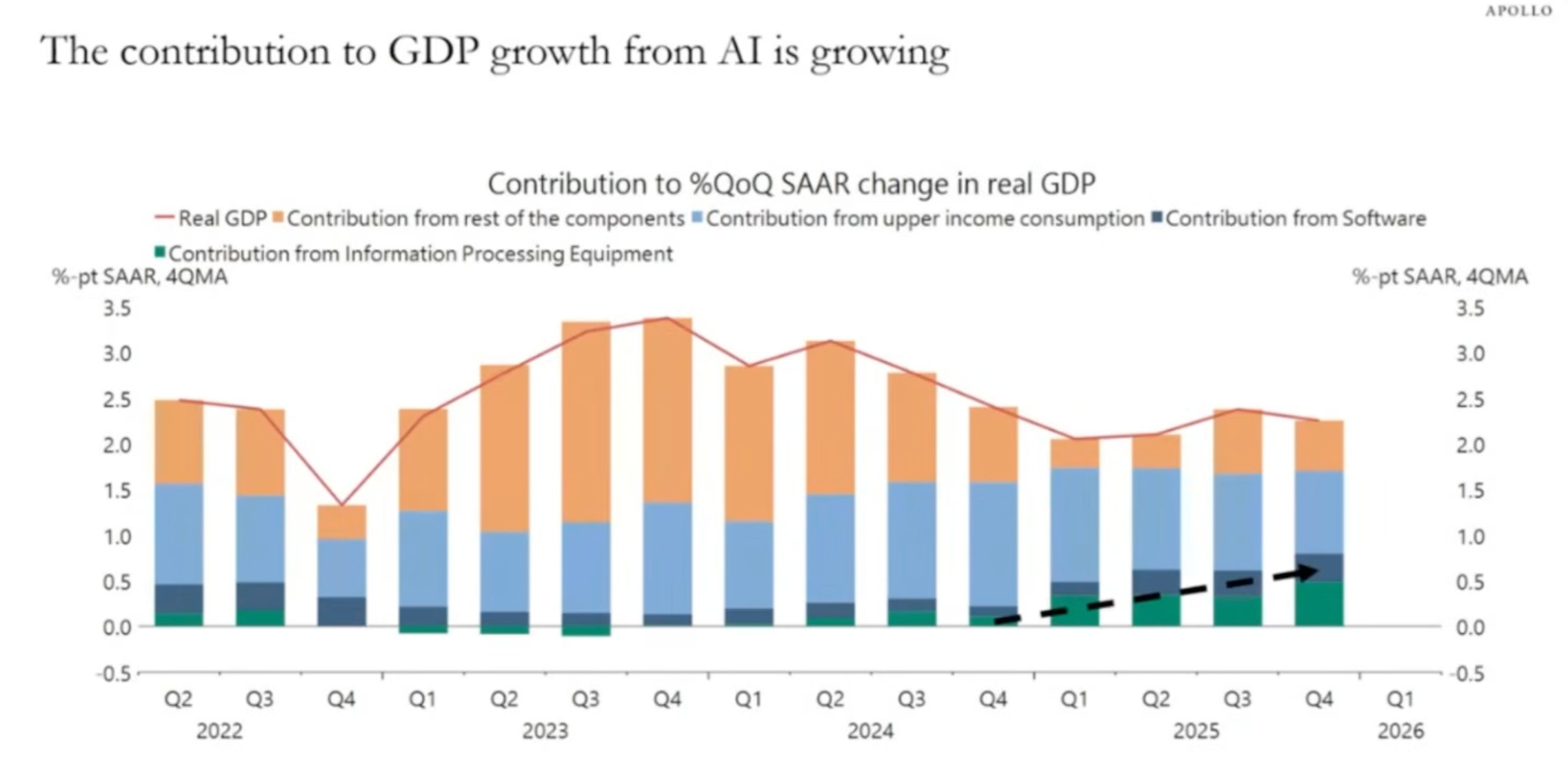

The narrative for 2026 changed because we crossed a threshold where AI can be deployed as a workflow. That turns AI into a factor of production.

And once something becomes a factor of production, it leaks into:

productivity stats

margins

hiring

capex

the inflation/deflation mix

and ultimately valuation.

Let’s go into abit of a macro economic lesson here to see how AI is affecting us.

Historically, macro cycles are shaped by constraints:

labor availability

energy

capital costs

logistics / supply chains

AI relaxes one of the big ones: white-collar labor as a bottleneck and its not by making humans smarter, by making the marginal unit of cognitive labor, cheaper, more available, more scalable and less constrained by time zones and headcount.

That is functionally similar to a positive labor supply shock in a subset of the economy.

Macro implications:

disinflationary pressure in sectors where labor is a major input cost

margin expansion for adopters

intensified competition for non-adopters

and a distributional shock (winners + losers, not uniform benefit)

This is why you can simultaneously see productivity boom narratives and white-collar recession fears

Both can be true depending on who captures the surplus.

COVID forced a step-change in behavior because constraints shifted overnight.

AI is forcing a step-change because it compresses the economy’s cycle time and that tends to show up as:

higher dispersion across sectors

structurally higher volatility

and faster narrative rotations

3) The Underpriced Macro Variable = Fiscal Capacity + Social Reaction Function

Here’s the part I think is most under-discussed.

If AI reduces the marginal demand for white-collar labor, it pressures:

income tax receipts (high earners contribute a disproportionate share in many systems)

payroll taxes (funding social insurance, healthcare, pensions)

consumption (white-collar wages are high MPC for services, housing, discretionary)

local government revenues (property, sales tax, municipal finance)

The macro question is: does AI compress the taxable wage base relative to spending commitments?

Governments will respond.

AI → productivity + displacement → policy response.

That usually expresses through some combination of:

targeted fiscal transfers (rebates, credits, consumption support)

industrial policy (subsidized capex, national champions, strategic sectors)

labor market spending (reskilling, wage subsidies, public-private programs)

regulatory steering (AI compliance, liability, hiring rules, credential reforms)

financial stability tools (liquidity facilities, backstops, implicit vol suppression)

When a state wants to stabilize real activity and social outcomes while managing a debt stock, the path of least resistance is typically:

tolerate higher nominal growth,

suppress parts of the rate complex when needed,

and let adjustment occur through currency debasement at the margin.

That’s why in stress regimes you can see supported risk assets and real assets, even when parts of the real economy are uneven.

Which is why real assets can remain bid even in a productivity narrative:

productivity can be disinflationary in micro terms

while policy response can be inflationary in nominal terms

Both can coexist.

👇🧵

Macro Pulse Update 28.10.2024, covering the following topics:

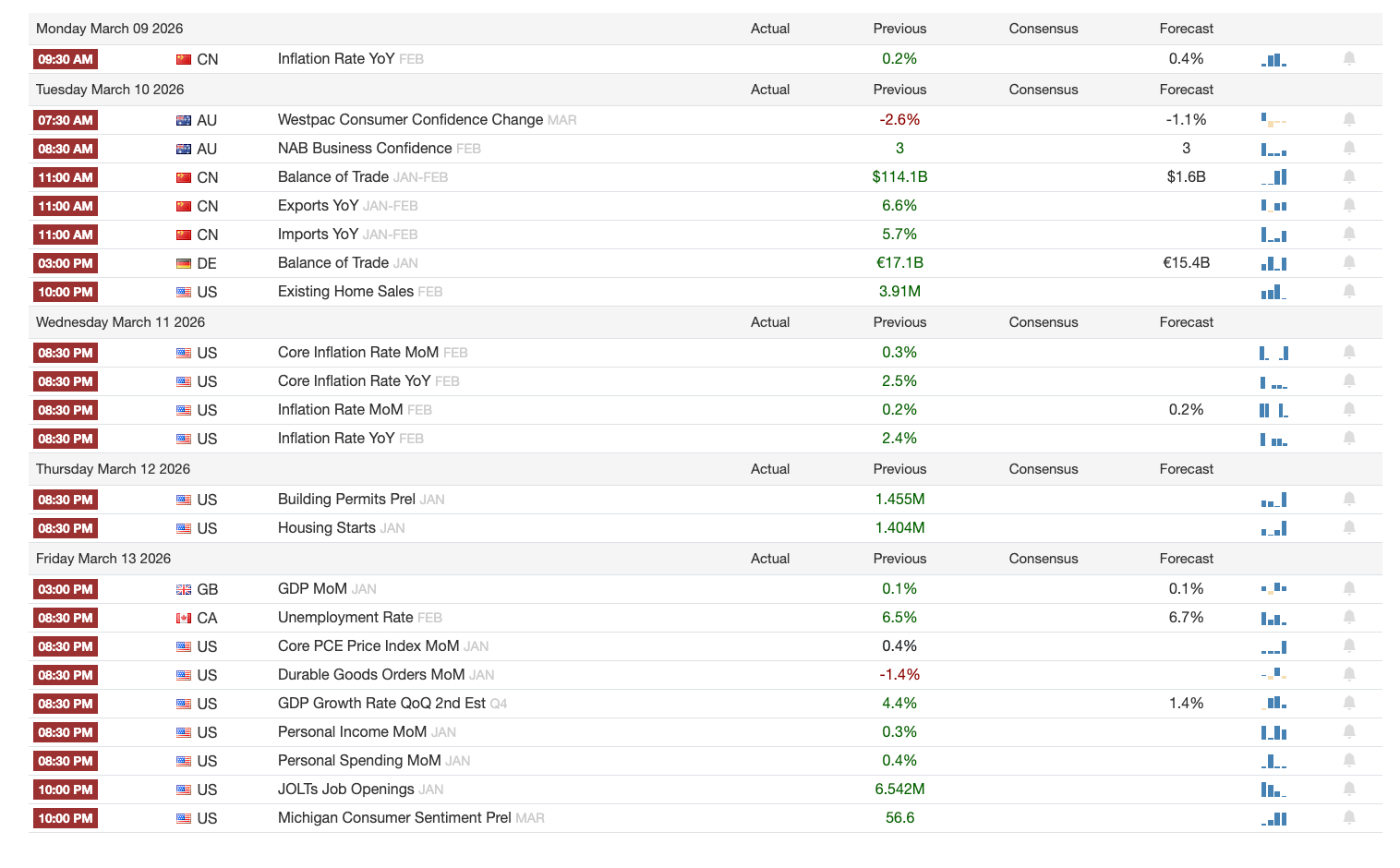

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

1️⃣ Macro events for the week

Last week

Next week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

AI sentiment spillover: Tech risk sentiment weakened as “AI valuation” debate re-ignited, amplified by Citrini-style bear narratives and cautionary tone from major exec commentary.

Geopolitics: Feb 28 reports of U.S.–Israel strike on Iran hit crypto downside in real time; tokenized gold spiked toward ~$5,500 intraday.

Cross-asset: Week to Feb 27: S&P +0.52%, Nasdaq +1.31%, Gold +3.12%, Silver +10.15%, while BTC underperformed on risk-off stress.

Retail shift: Wintermute flagged retail increasingly favoring equities over crypto since late 2024, turning retail activity vs altcap correlation negative (liquidity pulled away).

Corporate treasuries / balance sheets

Strategy (MSTR): Logged its 100th BTC buy, adding 592 BTC (~$39.8M) and raising holdings to 717,722 BTC (avg cost $76,020).

Funding: Strategy funded buys via 297,940 MSTR shares sold (~$39.7M) with $7.8B still authorized for issuance.

BitMine: Increased ETH treasury by 51,162 ETH ($98M), taking total to 4,422,659 ETH ($8.5B) and framed conditions as a “mini crypto winter.”

Staking: BitMine said a portion is staked with annualized revenue “hundreds of millions,” and plans MAVAN staking launch in early 2026.

Market integrity / investigations

Terraform vs Jane Street: Terraform estate filed an 83-page SDNY civil complaint alleging insider trading/manipulation tied to the May 2022 UST/LUNA collapse; Jane Street denied.

ZachXBT vs Axiom: ZachXBT alleged Axiom employees misused internal wallet data/tools for trading advantage amid a $38.1M Polymarket frenzy.

Stablecoins / TradFi rails

Circle: Reported $770M Q4 revenue (+77% YoY), USDC $75.3B (+72%), $11.9T quarterly on-chain volume (+247%), shares jumped ~30–35.5%.

Barclays: Began vendor consultations to build a platform for payments, stablecoins, tokenized deposits, with partner selection targeted by April 2026.

Morgan Stanley: Filed for a national trust bank charter for digital asset custody + staking (“Morgan Stanley Digital Trust National Association”).

SoFi: Enabled direct on-chain Solana deposits for 13.7M customers and cited SoFiUSD stablecoin launch in Dec 2025.

Meta: Targeting H2 2026 stablecoin payments via third parties; Stripe floated as a potential partner after Bridge acquisition and conditional OCC trust approval.

USD1: Trump-affiliated stablecoin briefly depegged to $0.9942 (one venue printed $0.9802) before recovering; WLFI alleged coordinated attack.

Ethereum / ecosystem

EF staking: Ethereum Foundation began staking (initial 2,016 ETH) toward planned 70,000 ETH deployment; rewards return to treasury.

Roadmap: “Strawmap” draft referenced targets like ~10,000 TPS L1 and up to 10M TPS L2 across forks through 2029.

Vitalik sales: Report cited on-chain tracking of ~10.7k–16.4k ETH sold since Feb 2 for ~$21.7M avg ~$2,027/ETH (per report).

Regulation / enforcement

Binance/Iran: Binance denied claims of $1B+ Iran-linked USDT transfers; Senate probe launched; Binance cited 97% exposure drop since early 2024 and large compliance headcount.

South Korea: Proposed mandatory influencer disclosure rules for crypto/stocks; police arrested two over alleged theft of 22 BTC evidence; separate incident involved leaked recovery phrase.

Automation / volatility

AI bot error: AI trading agent reportedly sent 52.43M $LOBSTAR after decimal misunderstanding; recipient sold into thin liquidity; token later surged 190%.

Winners/Losers

Top gainers: PIPPIN +21.09%, DCR +19.21%, MORPHO +12.10%, M +9.44%, JST +8.67%.

Top losers: ATOM -24.78%, BCH -21.72%, ZEC -20.62%, PEPE -19.74%, PUMP -17.02%.