i will present a bit of a contrarian take, polygon is NOT DEAD and it is becoming the open money stack.

@0xPolygon just spent $250M to stop being a blockchain and become a payments company

they acquired @Coinme and @0xsequence.

> coinme brings money-transmitter licenses (regulated fiat on/off ramps)

> sequence brings embedded wallets and one-click cross-chain orchestration. abstracts wallets swaps gas completely

calling it the open money stack.

blockchain rails + compliant fiat access + invisible onchain UX. this is vertical integration playbook

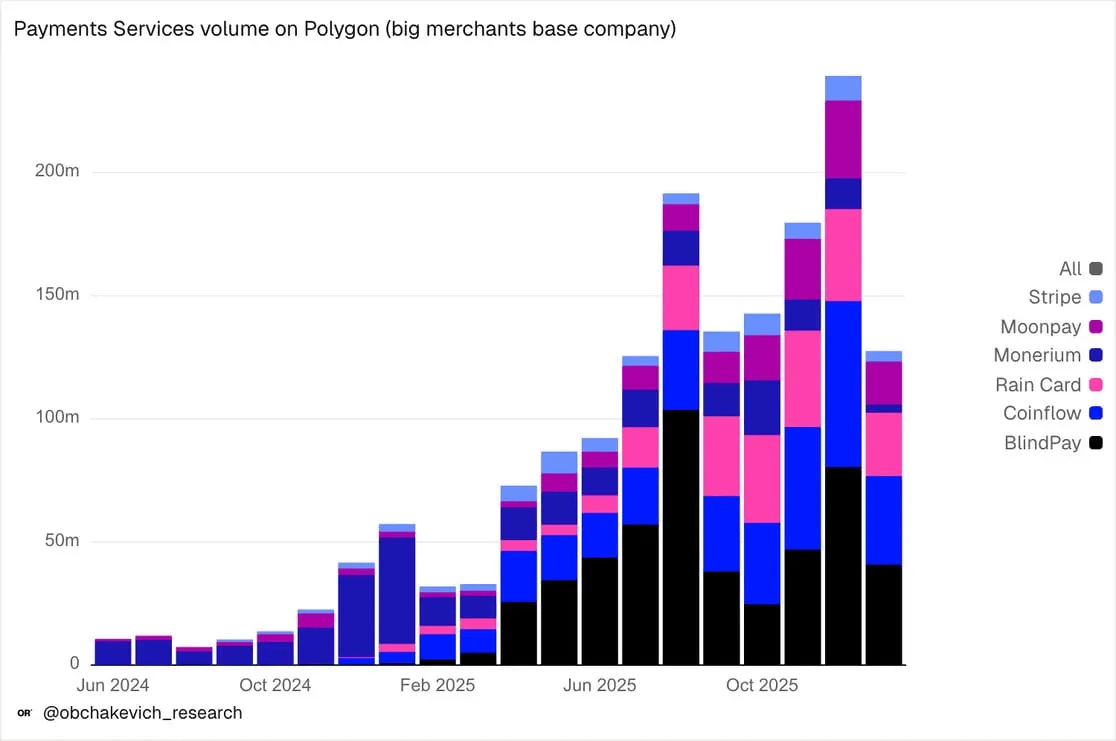

in 2025 polygon processed $1.4B payments services volume from @stripe, @blindpay and other merchants.

payments app transfers $7.7B total.

$364M jan → $1.43B dec

what polygon realized:

- being L2 scaling layer is commodity business.

- ZK tech is open source.

- sequencer fees compress toward zero. every chain offers similar speed and cost

- actual moat is owning the full payments stack from fiat in → blockchain settlement → fiat out with regulatory compliance and UX abstraction

stripe did $1T+ volume 2024.

polygon doing $1.4B on just merchant base payments. capturing even 1% of stripe’s flow would be $10B. that’s the TAM they’re chasing

my read on polygon:

- this works if merchants actually want blockchain settlement

- stablecoins are faster and cheaper than card networks for cross-border

- instant settlement vs T+2

- lower fees than 2.9% interchange

but merchants are conservative. stripe works.

why change? polygon needs to prove 10x better not 10% better to overcome switching costs also commoditization risk. if every L2 does this polygon’s early mover advantage disappears. arbitrum optimism base all have distribution and could replicate stack

my concerns as follows:

- if payments volume continues $57M → $239M trajectory and margins improve this validates thesis. if growth stagnates after acquisition that’s concerning

- also wondering about tokenomics, where does $POL fit in payments stack. if token doesn’t accrue value from payments growth then what’s point

- stripe doesn’t have token. successful payments companies monetize through basis points on flow.

- polygon’s challenge: build sustainable business model not just revenue line

honestly respect the conviction. pivoting from L2 to payments company

most L2s still optimizing for TVL and transaction counts. polygon optimizing for regulated fiat settlement volume

one strategy is futures-focused. other is present-focused. we’ll know which was right by end of 2026

market still values polygon as L2. should be valued as payments infrastructure if execution continues

if those deliver polygon rebuilt itself. if they don’t this will be an expensive mistake