Grayscale triumph over the SEC was a BULL trap.

Recession is looming. Credit deepens. All eyes on ETFs.

Here are 7 indicators showing signs of nuke 👇🧵

Macro Pulse Update 02.09.2023, covering the following topics:

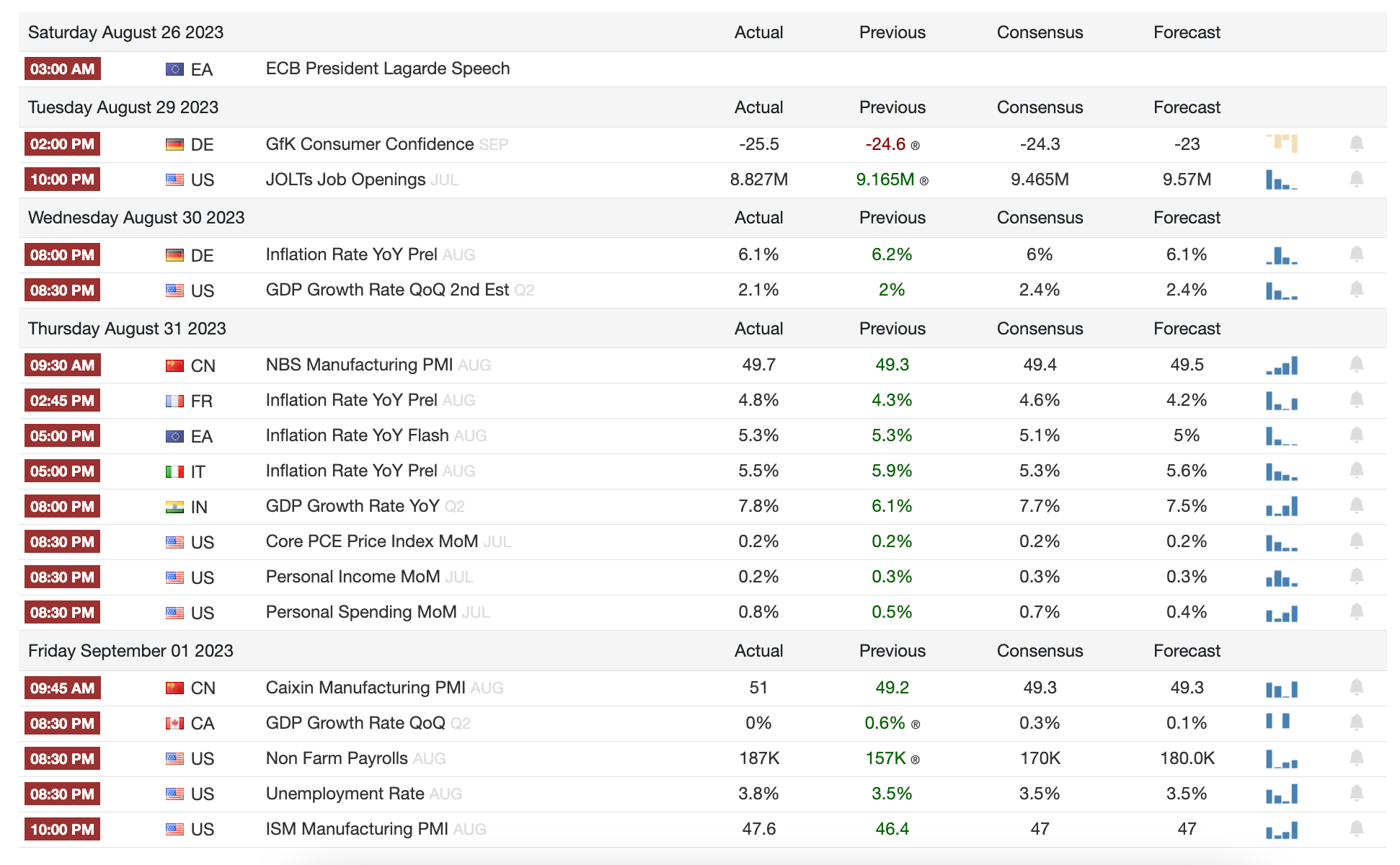

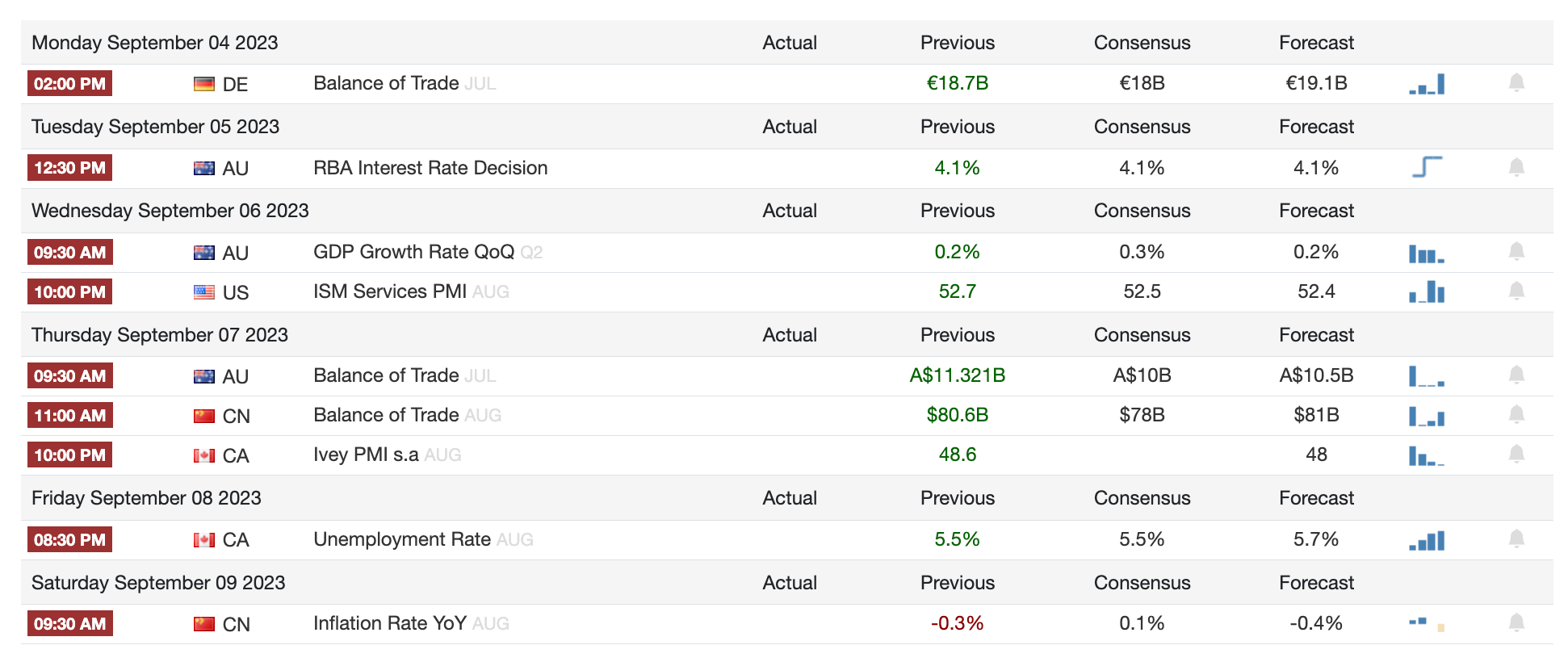

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

1️⃣ Macro events for the week

Previous week

Coming week (Key events: Bitcoin ETF filing)

2️⃣ Bitcoin Buzz Indicator

Market Movers and Shakers

Grayscale's Legal Win Shakes Up Bitcoin Market

Chainlink and SWIFT's Banking Breakthrough

Binance and EOS Thrive in Japan's Crypto Landscape

The Ethereum Market Reacts to Big Investments

Regulatory and Legal Developments

SEC Delays Decision on Bitcoin ETFs

Ronaldinho Denies Involvement in Crypto Scam

Crypto Exchanges and Platforms

Binance's Struggle with New Stablecoin FDUSD

StarkWare Unveils On-Chain Data Verification Tech

Polygon Rolls Out Development Kit for Layer 2 Chains

Friend.tech Faces Backlash Over User Policy

Altcoins

Balancer suffered $900,000 breach despite warnings; TVL fell $164M.

LimeWire used Polygon for AI Studio, LMWR rose 18%.

Aerodrome attracted $150M to Base blockchain on first day; PancakeSwap expanded to Base.

Aptos to unlock 24.8M APT tokens on November 12, 2023.

DWF Labs invested in FET, becoming the 21st largest whale.

Cryptocurrency funds saw highest outflows since March.

ApeCoin & Axie Infinity to unlock 11% of market cap on September 16 and October 20, respectively.

Bitcoin Cash jumped 15% due to its increased exposure after the ETF news, but then retraced.

Cosmos voted on liquid staking plan for DeFi.

DYDX unlocked 6.52M tokens worth $14M for community treasury, rewards on August 29.

Base to receive 118M OP tokens over six years in revenue and governance agreement.

16 Bitcoin mining companies had $4.47 billion in losses in a year.

1inch Fund acquired $10M of Ethereum.

DOGE jumped as Elon Musk's X got closer to crypto payments.

Robinhood added 200+ Ethereum and Polygon tokens to in-app swaps on Robinhood Wallet.

MakerDAO’s MKR jumped 10% as platform returned to profits.

Nexo launched crypto Mastercard for EEA citizens.

Ripple unlocked 1 billion tokens worth $500 million.

Shibarium crossed 600K wallets as SHIB whale moved $38M worth of tokens.

Lira-backed TRYB Token became world's second-largest non-dollar-pegged stablecoin.

Theta and Google Cloud unveiled project at Google conference.

Mercado Libre, Circle brought USDC to Chile; USDC to expand to Base & Optimism.

Worldcoin hit new sign-up record despite huge decline in price.

Tokenized U.S. Treasuries arrived to XDC Network as digital bond market grows.

Wintermute failed to ask Yearn Finance for YFI token loan.

3️⃣ Market overview

Data indicates US economy is moderating as expected following Fed tightening, but remains durable even as risks linger around labor market resilience. China's real estate turmoil persists but has potential for greater impact. Markets balancing cautious optimism on inflation outlook with close monitoring of key data for guidance on growth and policy direction.

🟡US Q2 GDP growth revised down slightly but still indicates economic resilience and momentum despite inflation and rate hikes. However, risks remain focused on potential impact to labor market.

🔴Country Garden's massive $6.7B H1 2023 loss highlights liquidity crisis and challenges in China's real estate sector. Defaults and debt repayments for developers in coming months will be important to monitor for broader spillover effects.

🟢 US equities extended gains on moderating economy and inflation data, suggesting potential Fed pausing of rate hikes. Investors now eyeing upcoming Chinese and US data for further clues on global growth and policy implications. Markets seem cautious but optimistic on potential turning point while remaining vigilant on economic shifts.

🔴 September faces historical weakness, investor distribution, and growing macro linkage as headwinds. But outcomes of upcoming inflation data and Fed meeting could diverge from seasonal trends. Careful tracking of key indicators like oil and China economy warranted.

September is historically the worst performing month for Bitcoin and crypto, hence the nicknames like "Septembear" and "Rektember".

Investors taking profits or getting liquidated after summer tend to sell assets, adding selling pressure in September.

Crypto is becoming more correlated to stocks, which also tend to decline in September. The high Bitcoin-Nasdaq correlation you highlighted underscores this linkage.

Key macro events to watch that could impact September performance:

US CPI on Sept 13th - important for gauging inflation outlook and potential Fed rate hike path.

Fed meeting Sept 19-20 - rate decision and guidance will significantly influence markets.

Oil prices gaining upside momentum - could affect recession odds and broader risk asset sentiment.

China's slowing economy - potential spillover effect on global growth and corporate earnings.

4️⃣ Key Economic Metrics

🟡 Labor market

Labor market and economy are on a path toward a soft landing, but risks remain from business spending slowdown and consumers' wavering confidence. Key to watch wage growth, job openings, and capital expenditures for further cooling.

Job growth remains decent but is moderating from pandemic highs to pre-pandemic levels, with 187K jobs added in August. This signals economic expansion is ongoing but slowing.

Labor demand is cooling - job openings fell, layoffs remained low, and wage growth softened. This suggests the Fed's rate hikes are having the desired effect.

Business equipment spending looks set to decline, manufacturing activity is contracting, inventories are lean. Capital expenditure pullback is a headwind.

Housing market is resilient with construction spending rising on increased residential building. Nonresidential softening though.

🔴 Credits, Debts

Surging credit card usage across income levels, especially middle and upper earners, signals strained household finances and growing reliance on credit to maintain outsized spending growth amid lagging incomes. Further increases likely if this imbalance persists.

Household Pulse survey shows a significant increase in middle to upper income households using credit cards/loans to meet weekly spending over the past 2 years.

The $75K-$149K income range has seen the largest growth, with a doubling of households reporting credit card usage since early 2021. This aligns with record high outstanding credit card balances reported in recent New York Fed data.

It reflects pressured household balance sheets as spending outpaces incomes and savings fall. Credit cards help maintain elevated spending levels.

Lower income households already relied heavily on credit cards, less increase recently. Highest incomes less affected as well.

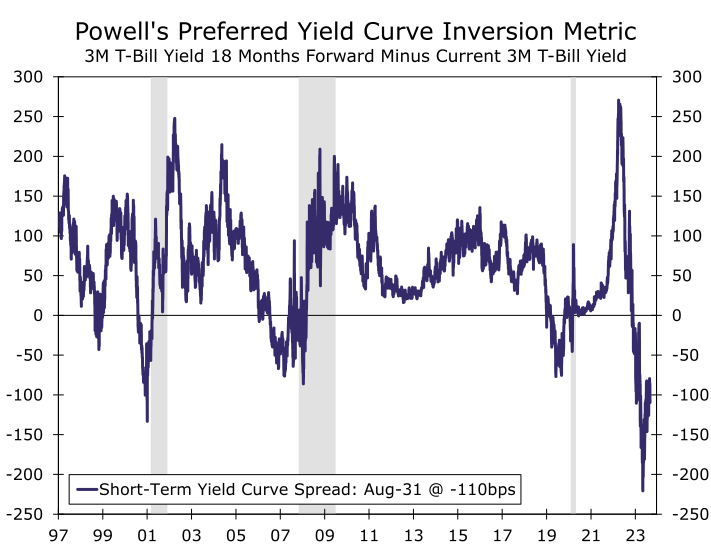

🔴 Yield Curve

The inverted yield curve, especially the short-end, is a key indicator flashing elevated warning signs of an impending recession despite some encouraging economic data. The curve shape implies skepticism around soft landing odds.

The yield curve, particularly the 10yr-2yr and 10yr-3mo spreads, remains deeply inverted. This historically signals elevated recession risk.

Long-term yields have challenges for comparison due to declining term premiums. Short-term yield curve may be more insightful.

The short curve spread that Powell cited remains sharply negative, though less than earlier this year. Still a concerning signal.

Other markets like stocks seem optimistic on soft landing odds, but the yield curve inversion persists as a warning sign.

The curve flattening/inversion implies markets expect Fed rate cuts in the future due to economic weakness.

While a soft landing is possible, the yield curve suggests high likelihood of a recession in 2024 after Fed tightening.

Twitter: https://twitter.com/arndxt_xo/status/1697931133164667253