We’re in the great divergence

$BTC celebrates its 15th birthday

Here’s 5 indicators for economy walking on tightrope👇🧵

Macro Pulse Update 06.01.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ Interest Rate Watch

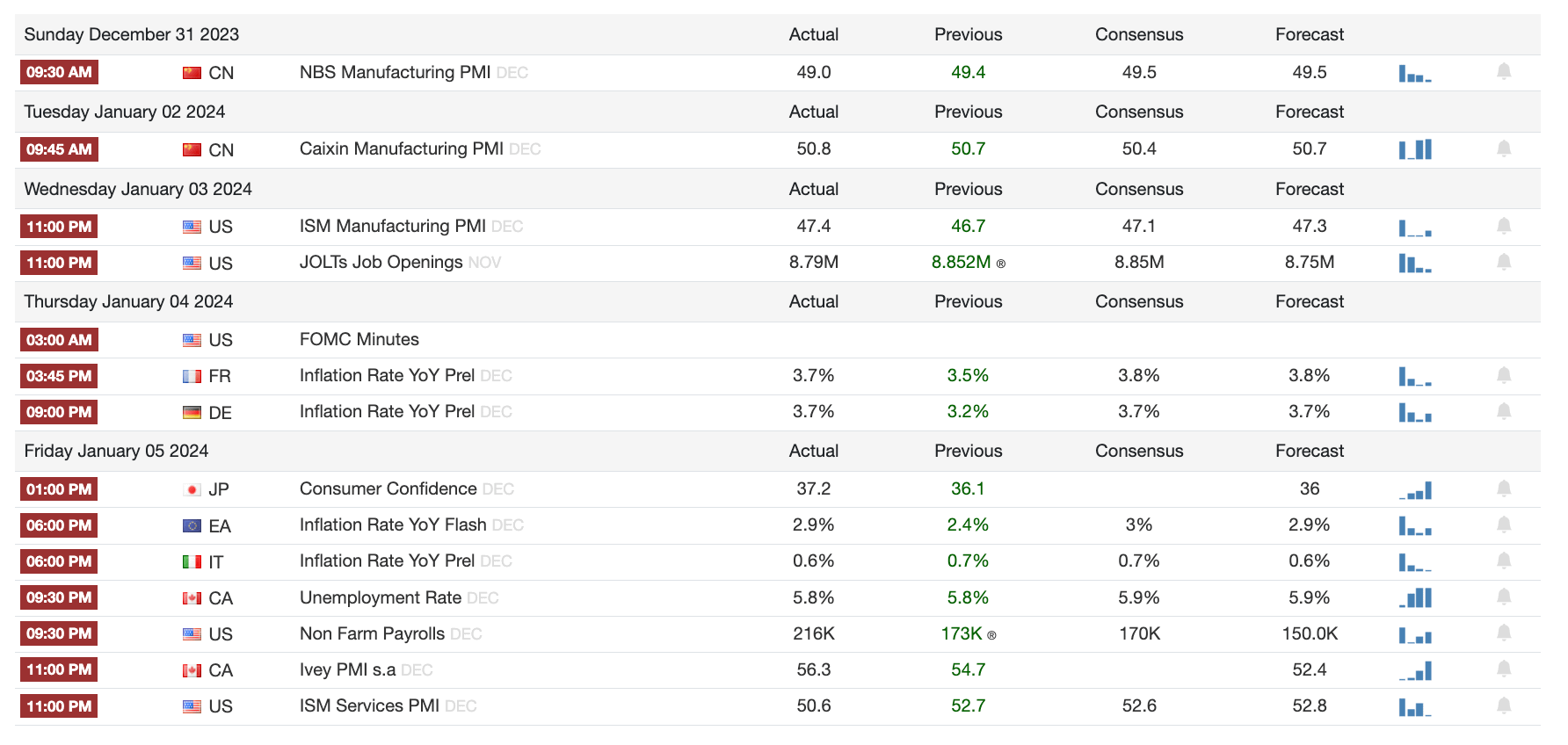

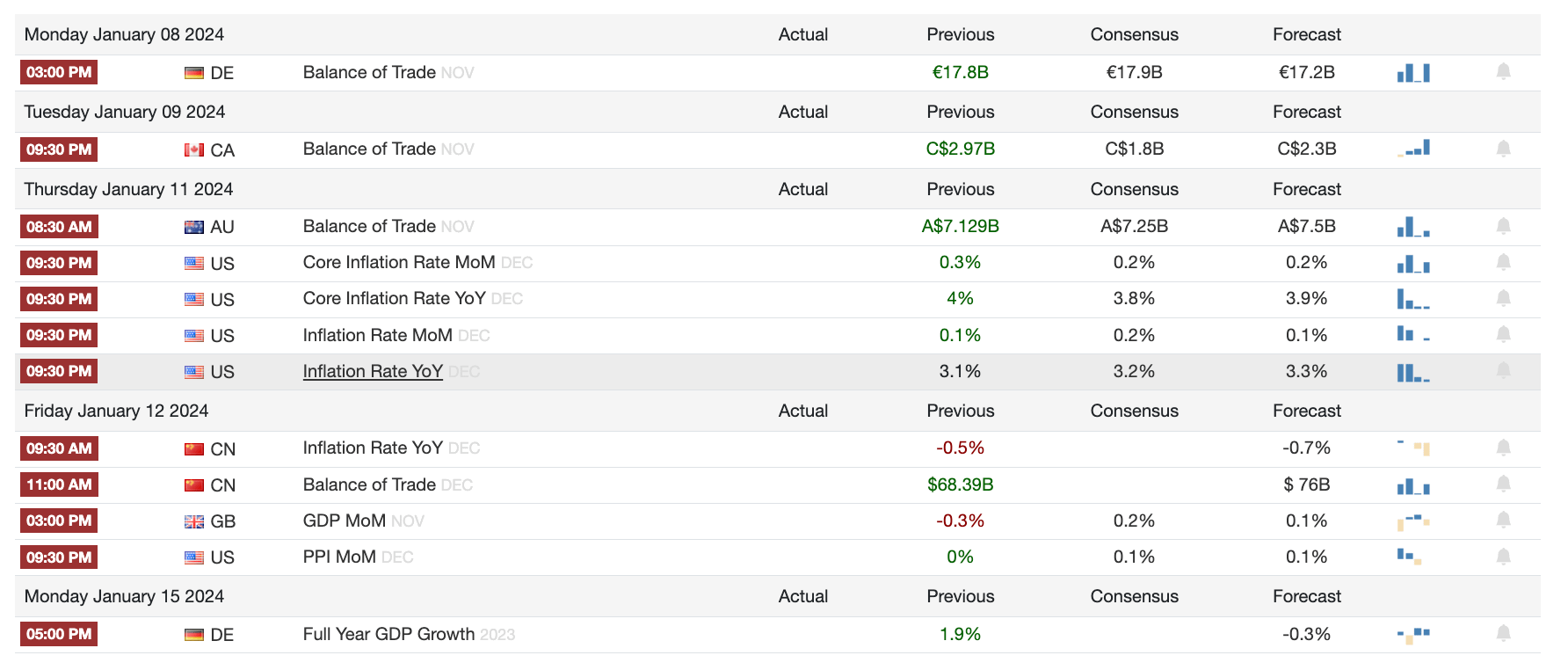

1️⃣ Macro events for the week

Last week

Next Week

2️⃣ Bitcoin Buzz Indicator

Market Updates

Goldman Sachs Joins Bitcoin ETF Race

Bitcoin's 15th Birthday Market Turmoil

Celsius Network's Ethereum Unstake Amid Bankruptcy

Orbit Bridge Heist Highlights Security Issues

Tellor's Price Volatility Raises Concerns

Binance Increases Scrutiny on Privacy Coins

Security and Regulation

Recent Security Breaches in Crypto

SEC's Growing Focus on Crypto Regulation

IRS Rule 6050I Stirs Crypto Community

Exchange and Platform News

Huobi Korea's Closure Amidst Market Challenges

NFT and Copyright Developments

Logan Paul's CryptoZoo NFT Buy-Back Plan

Mickey Mouse NFTs Enter Public Domain

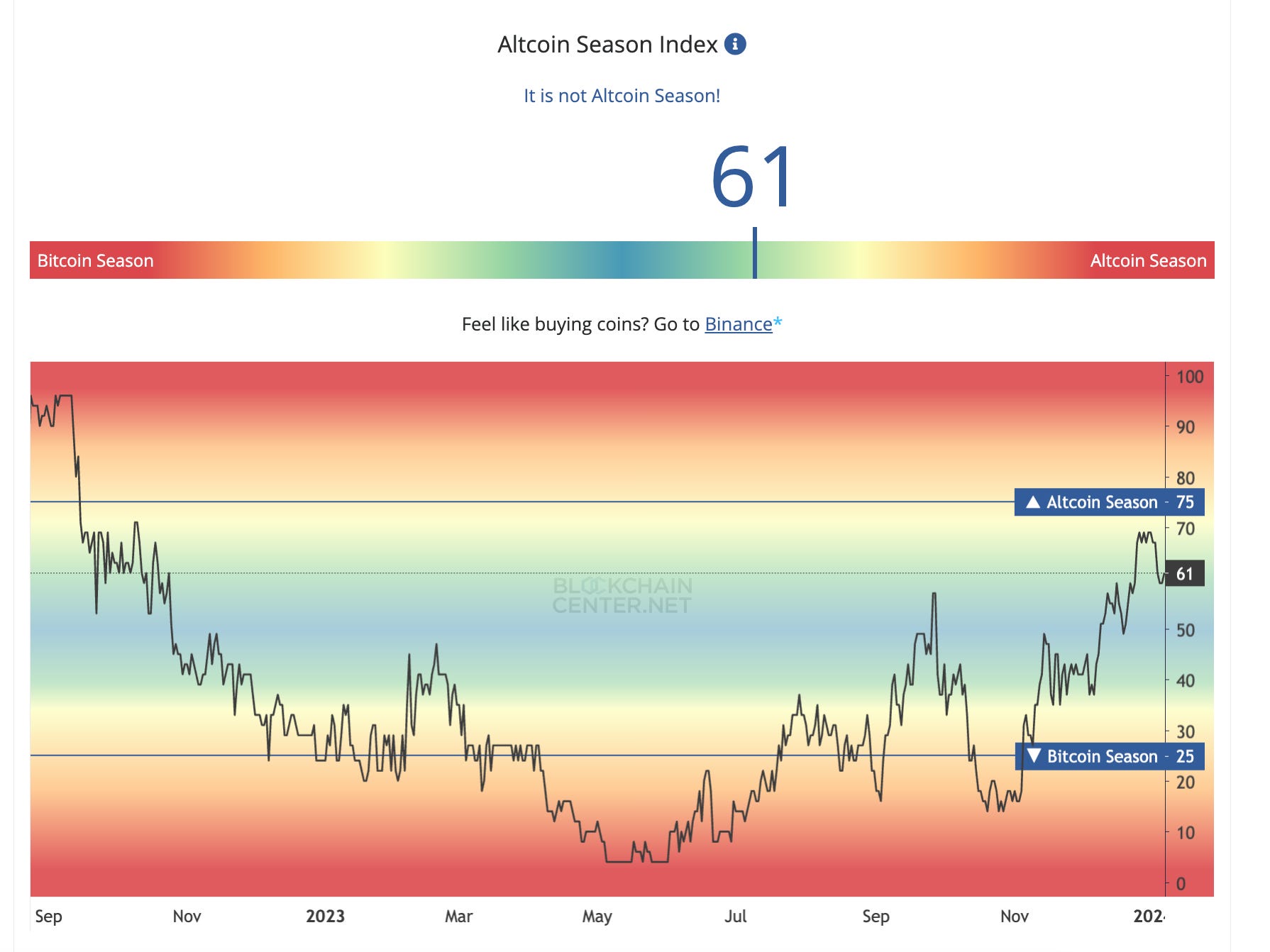

Altcoins

Major token unlocks in January 2024 will introduce over $600M in liquidity from Aptos, Injective, and Optimism.

Stake secured naming rights for Sauber's F1 team, indicating crypto's growing sports marketing push.

Fake token scams persist, with a wallet founder losing $125K to fake LFG token.

Arbitrum and Optimism prices approached all-time highs as interest in layer 2 solutions climbs.

Jupiter has an upcoming JUP airdrop planned showing continued incentive efforts.

Osmosis hits $1B monthly volume milestone highlighting Cosmos ecosystem traction.

Stacks sees 10% price boost driven by recovery and planned network upgrade.

Etherscan acquires Solscan, expanding scope into Solana ecosystem.

ENS token surges 50% on Vitalik Buterin endorsement underscoring influence.

Crypto investment inflows hit $2.2B in 2023 signaling asset class interest.

Wemade's $100M Web3 fund leads to $41M tax bill indicating regulatory hurdles.

Solana Foundation plans Brazil expansion showing developing world push.

Arbitrum enables select ERC-20 tokens for fees, increasing flexibility.

Starknet vote transitions fee upgrade from testnet to mainnet.

Celestia sees 671% gain driven by staking and modular narrative.

Beam token rises as Merit Circle transactions hit record high.

9GAG token surges following Binance investment showing memecoin interest.

SEI hits all-time high with memecoin leading 380% gain.

High Maker trading activity points to renewed market interest.

3️⃣ Market overview

Bitcoin's strong performance, the outlook for a Bitcoin ETF decision from the SEC, Ethereum's roadmap priorities, interest rate expectations from the Fed, jobs data complicating the rate outlook, stock market performance, oil price increases, and outperforming crypto assets like Sei and Arbitrum.

Bitcoin gained 156% in 2023, rising from around $16k to over $42k by year end, regaining credibility after the crypto collapses of 2022. Anticipation of a spot Bitcoin ETF decision has driven recent price momentum.

Ethereum's 2024 roadmap remains focused on six key priorities: the Merge, Surge, Scourge, Verge, Purge and Splurge. Progress has been slow and ether has struggled to break out above $2,400 despite strength in competing Layer 1s.

Minutes from the latest Fed meeting show rates are likely at their peak, but strong December jobs numbers complicate the outlook for rate cuts in early 2024.

Stocks had a shaky start in 2023 amid broader uncertainty, with fintech names hit particularly hard.

Oil prices are rising on geopolitical tensions in the Middle East that could disrupt global supplies.

Among outperforming crypto assets are Sei (SEI), up 25% to new all-time highs, and Arbitrum (ARB), up 28% with surging TVL and volumes.

4️⃣ Key Economic Metrics

Diverging economic trends across different sectors in light of tighter monetary policy. While interest rate-sensitive areas like housing and manufacturing remain under pressure, the labor market and services sector show signs of slowing but remain relatively resilient for now.

🟢 Job growth remains positive but is moderating from post-pandemic highs, concentrated in government, healthcare and hospitality sectors. Broader labor market indicators like labor force participation and hiring rates are softening.

🔴 Manufacturing activity continues to contract sharply (14 straight months per ISM index) on weak demand and grim employment outlook, while service sector growth decelerates but remains mildly expansionary.

🟢 Personal spending data shows durable goods spending declining regularly while services spending steady outside one dip in past 40 months, indicating greater consumer resilience for services.

🟡 Within construction, strength concentrated in single-family home building as multifamily cools on rising vacancies. Nonresidential constrained by financing except publicly supported manufacturing projects.

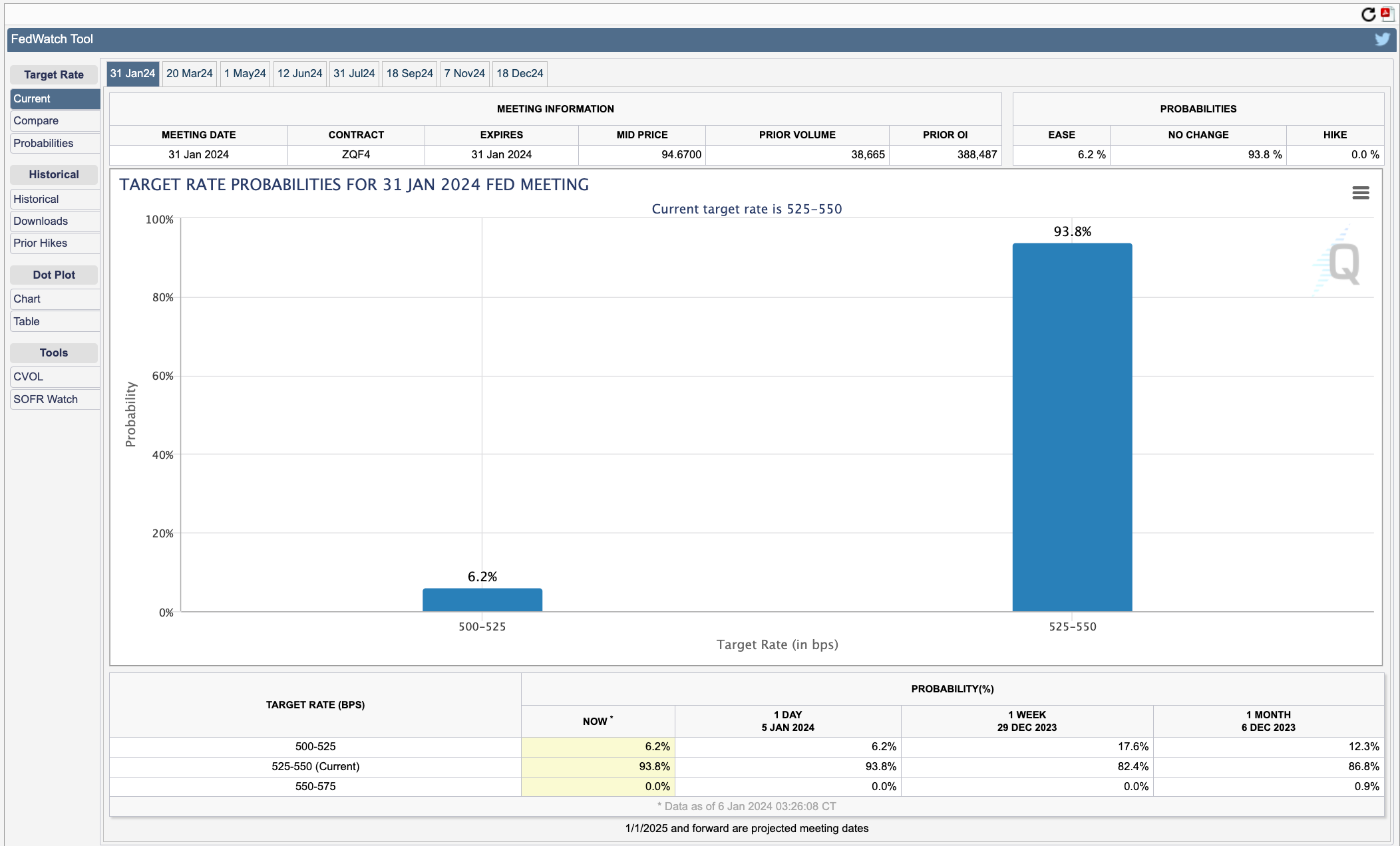

5️⃣ Interest Rate Watch 🟢

After a more dovish than expected December meeting, the Fed has since tried to walk back expectations for imminent rate cuts in 2024. While the minutes acknowledge cuts are likely this year if progress on inflation continues, there is little evidence of a debate on timing of cuts at the December meeting itself. The Fed appears to be in wait-and-see mode, sensitive to risks of both remaining restrictive for too long or easing too soon.

Dot plot and Powell's comments after Dec meeting initially signaled rate cuts in 2024, sparking market rally. Other Fed officials later tried to downplay this.

Minutes show no large debate on timing of cuts at the Dec meeting itself. Fed aims to remain restrictive for now to sustain disinflationary trend.

Next moves remain data dependent - Q1 inflation and jobs reports will determine if cuts could come as early as March, though June remains base case for first cut.

Fed walking line between risks of staying restrictive too long or easing too soon and reaccelerating inflation. Still premature to declare victory on inflation.

Twitter: https://twitter.com/arndxt_xo/status/1743626431736037854