Markets in turmoil as inflation sticks

Oil plunges, car loans sink underwater. BOJ clings to easy money with Yen in freefall.

6 market factors that that could set off an earthquake 👇🧵

Macro Pulse Update 07.10.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ Japan Spotlight

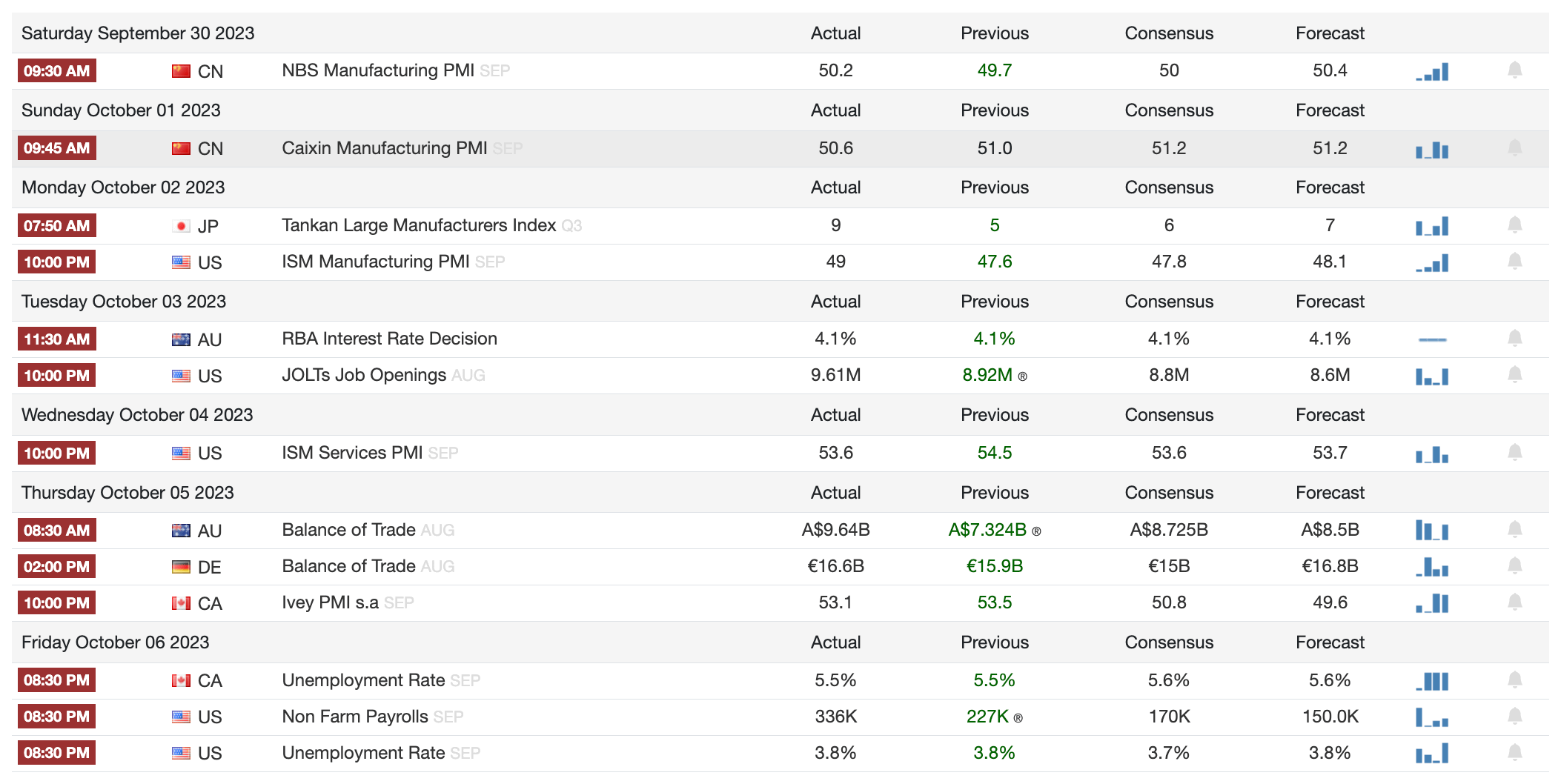

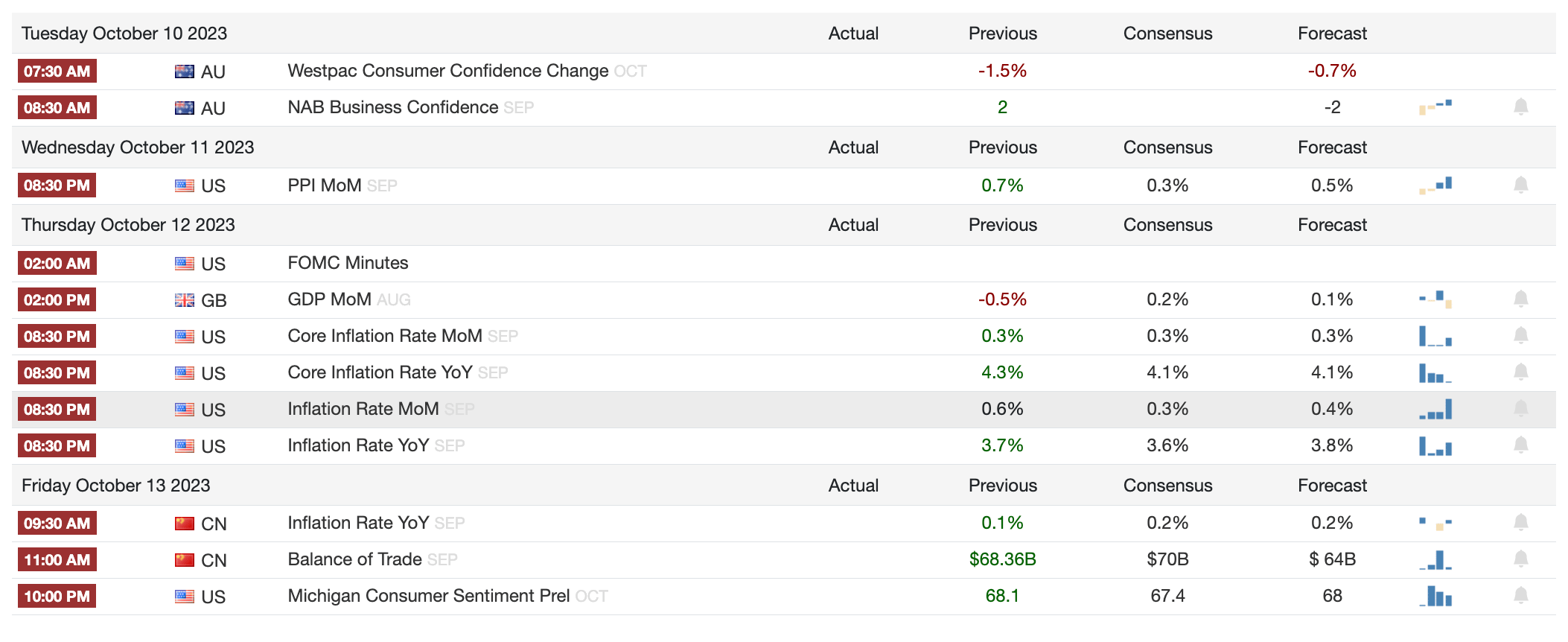

1️⃣ Macro events for the week

Last week

Next week

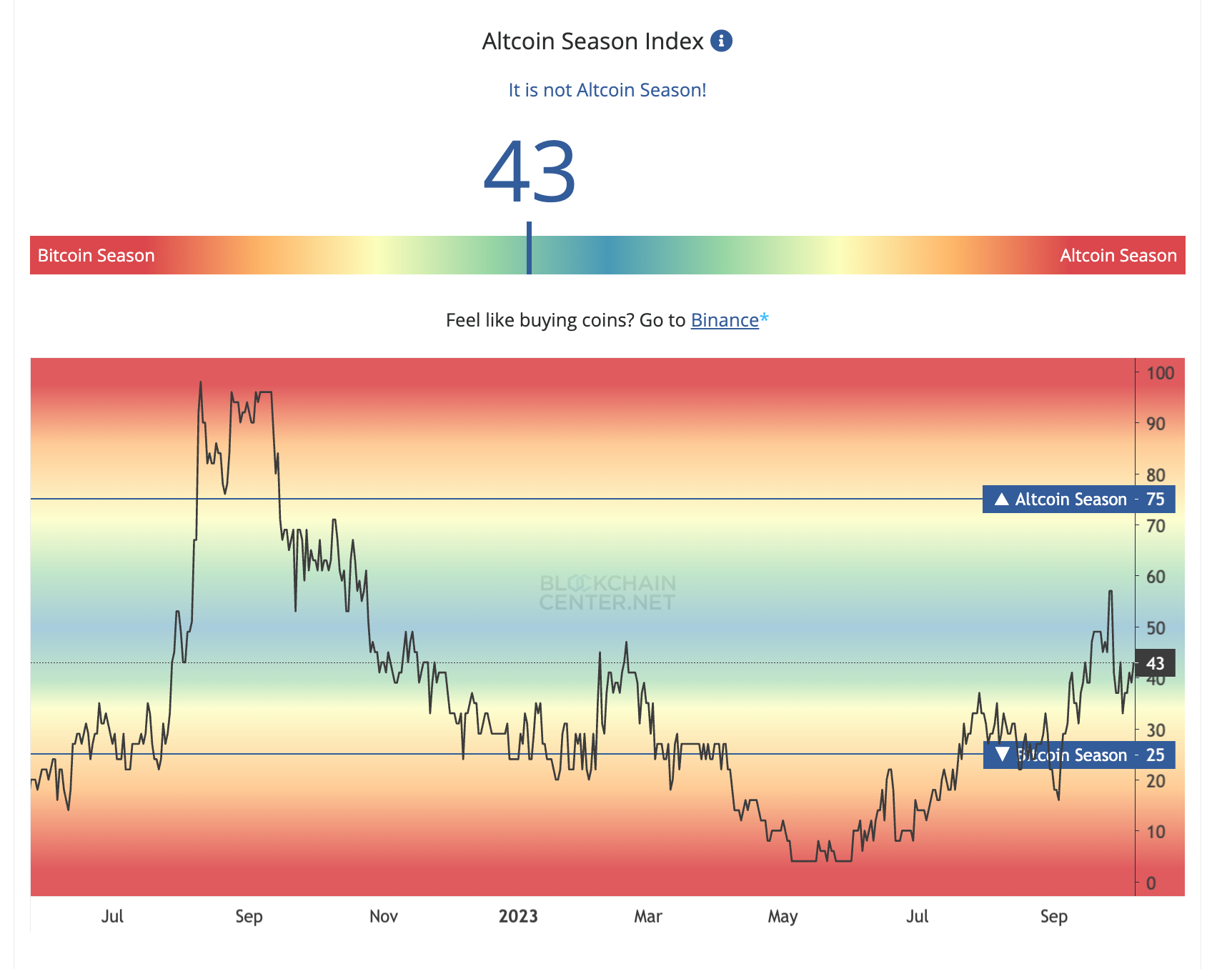

2️⃣ Bitcoin Buzz Indicator

Banking and Regulatory Updates

FTX's Fallen CEO Faces the Jury

Ethereum Futures ETFs Gain Momentum

Ripple's Legal Wins Boost XRP

Stars Arena's Meteoric Rise and Security Stumble

Challenges and Risks in the Crypto Market

Ethereum's Balancing Act of Challenges

Crypto VC Funding Plummets in Q3

Ledger Slashes Workforce Amid Market Woes

Asset Performance and Investment Trends

Solana Woos Institutional Investors

Crypto Exchanges and Platforms

Kraken Sets Sights on European Expansion

NFT News

OpenSea Simplifies NFT Creation

Yuga Labs Invests in Metaverse Expansion

Altcoins

Axie Infinity, Optimism, and Aptos to unlock tokens worth over $200M in October.

Chainlink rolled out 'Data Streams' to speed up data, boosting decentralized computing.

IOTA stepped into its 2.0 era with fresh upgrades.

Rollbit raked in $38M in betting revenues last September, RLB Token rose.

Friend.tech acted fast on SIM-swap issues, resulting in over 100 Ether drained.

Binance to halt BUSD lending on October 25.

Optimism's testnet deployed a fault-resistant system, eyeing true decentralization.

Verasity's VRA skyrocketed 71% after burning a massive 10 billion tokens.

Shiba Inu's Telegram Admin account got hijacked.

TON secured 8-figure funding from MEXC, aiming to turn Telegram into a Web3 powerhouse.

Hong Kong authorities teamed up for a crypto task force amid the unfolding JPEX drama.

THORSwap's RUNE dived 9% as operations froze over suspected shady dealings.

3️⃣ Market overview

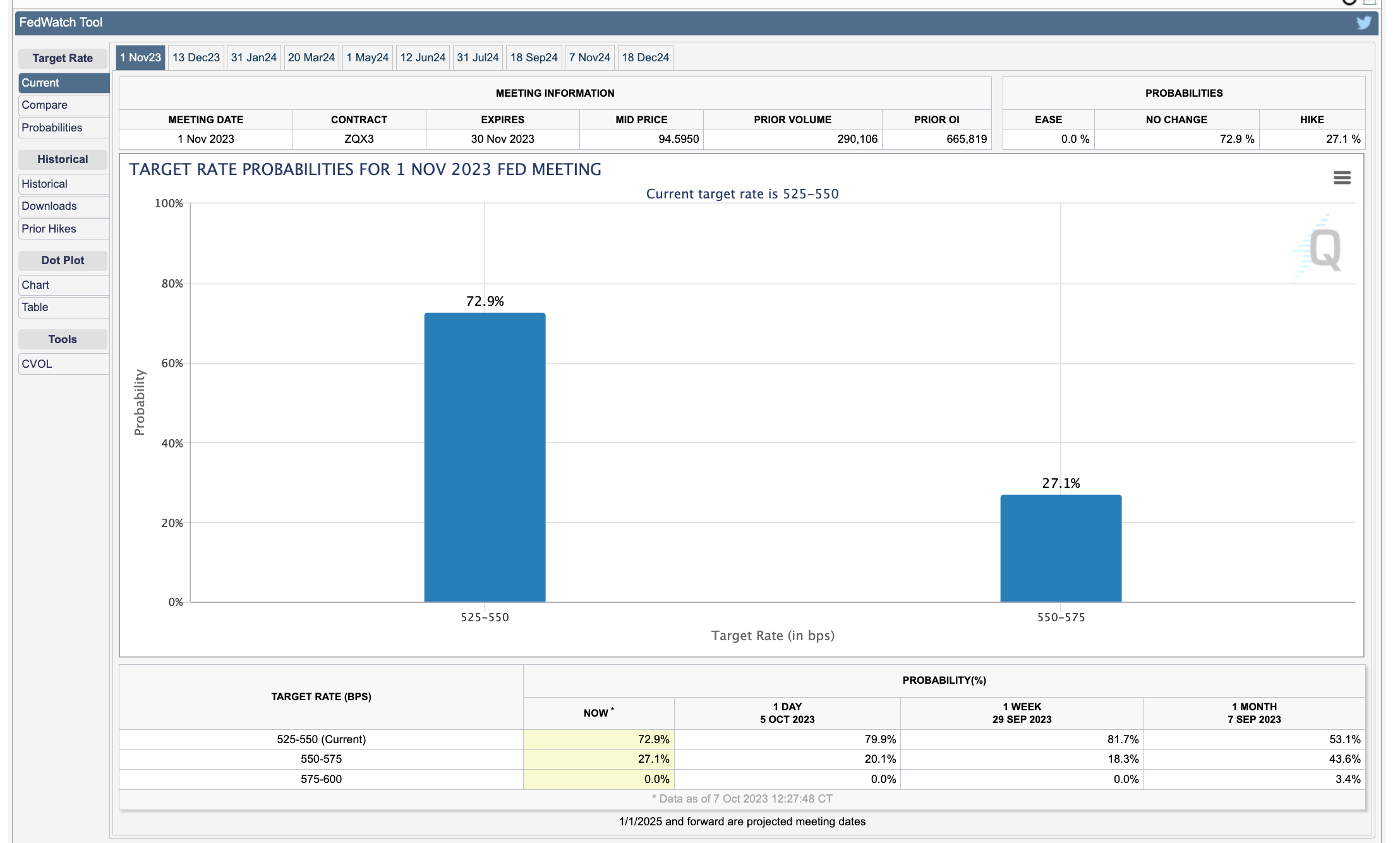

🟡 Sticky inflation and shifting central bank policies are creating uncertainty. Key data releases will continue to drive market volatility in the near-term.

U.S. labor market is showing signs of moderation as private payrolls undershot expectations in September. This could influence the Fed's future rate hike trajectory.

Biden administration expanded student loan forgiveness, with over $9 billion of debt cancelled so far. This provides relief to borrowers but adds to federal liabilities.

Equities rallied on weaker jobs data as it reduces likelihood of more aggressive Fed tightening. Treasury yields also declined. However, eurozone retail sales dropped sharply in August, pointing to impact of higher rates.

Upcoming U.S. jobs data including nonfarm payrolls will be closely watched to gauge strength of labor market. Markets seem positioned for some Fed pivot on policy, but will react to data confirming or disputing this view.

🔴 Headwinds of slowing growth, tightening monetary policy, and fiscal uncertainties driving market churn across assets. Oil, autos, stocks and bonds all facing challenges of lower demand and higher costs of capital.

Oil prices dropped sharply on concerns about slowing global growth and higher interest rates. Prices fell below $82/barrel, reversing previous gains. Production cuts by OPEC+ unable to stem declines.

Negative equity on U.S. car loans rising as used car values fall from pandemic highs. Trade-in vehicles now underwater by ~$5,820 on average, creating challenges for dealers and buyers.

Surging Treasury yields up to 2007 highs weighing on equities like S&P 500, Nasdaq and Dow amid Fed hawkishness. Investors shifting to guaranteed returns.

Treasury yield volatility spiking as measured by MOVE index, signaling continued turbulence ahead in bond markets.

4️⃣ Key Economic Metrics

🟡 Income under pressure from inflation but consumers maintaining spending via lower savings, though shifting away from goods. Moderating core inflation a positive sign for potential Fed policy easing.

Real disposable income fell 0.2% in August as income failed to keep up with inflation, though real wages rose.

Real consumer spending edged up 0.1% as savings rate declined, indicating households tapped savings.

Spending on goods dropped while services spending increased, reflecting ongoing shift post-pandemic.

Fed's preferred PCE inflation metric rose to 3.5% annually due to energy prices.

However, core PCE inflation excluding food and energy fell sharply to 3.9%, boosting hopes of nearing Fed policy pivot point.

🔴 Unwinding complex supply chain integration and reducing reliance on China will be very difficult and take considerable time. Trade environment likely to remain challenging.

Global trade volumes declined in July, with notable drops in China, Europe, and Asia. This reflects slowing demand, high inflation, tighter monetary policy, and lingering trade restrictions.

U.S. trade held up better, with June-July growth, helping buttress global trade. But outlook remains weak given expected monetary tightening.

Share of U.S. imports from China is declining, while imports from Mexico, Taiwan, India are rising, suggesting lower U.S. dependence on China.

However, China remains highly integrated in global supply chains and production of intermediate goods. True decoupling between U.S. and China has been limited so far.

U.S.-led Indo-Pacific Economic Framework aims to diversify regional trade and build resilience. But trade for members has become more concentrated on China in recent years, not less.

🔴 Money supply reduction and lending slowdown shows impact of ECB tightening. Falling inflation could influence future policy direction if sustained.

Eurozone money supply contracted sharply in August, with M3 declining 1.3% and M1 dropping 10.4% year-over-year. Tight ECB policy intended to reduce aggregate demand.

Bank lending to private sector also slowed considerably as credit conditions tightened.

Real money supply declines seen as predictor of recession, though M1 shift may be technical.

Eurozone inflation fell notably in September, down to 4.3% from 5.2% in August. Underlying inflation excluding food and energy also declined.

Drop reflects lower inflation in Germany and Netherlands, while peripheral countries were more stable. Suggests ECB policy working to reduce price pressures.

Declines drove bond yields down initially, though Italian yields spiked over fiscal concerns. Higher yields spreading to other European countries.

5️⃣ Japan Spotlight 🔴

Japan's monetary policy and currency issues; True yen impact would require BOJ policy change, but bank committed to current stance. Japan facing challenges balancing inflation, growth and currency stability

Bank of Japan stressing intent to keep monetary policy easy despite high inflation, contributing to sharp yen depreciation.

BOJ Governor Ueda said inflation so far driven by supply factors, so rates need to stay low. But uncertainty if demand conditions will sustain inflation.

Further yen falls could trigger intervention by Japan authorities to purchase yen and tighten policy. Seen as last resort option.

Finance Minister Suzuki said all options open if yen breaches 150 per dollar, but rates should be market determined.

Yen very sensitive to US-Japan rate differential which favors dollar strength. Intervention likely to be sterilized and ineffective.

Twitter: https://twitter.com/arndxt_xo/status/1710614206507335795