Inflation persistent amid slowing growth.

Macro at a delicate balance

8 factors for a soft landing👇🧵

Macro Pulse Update 11.11.2023, covering the following topics:

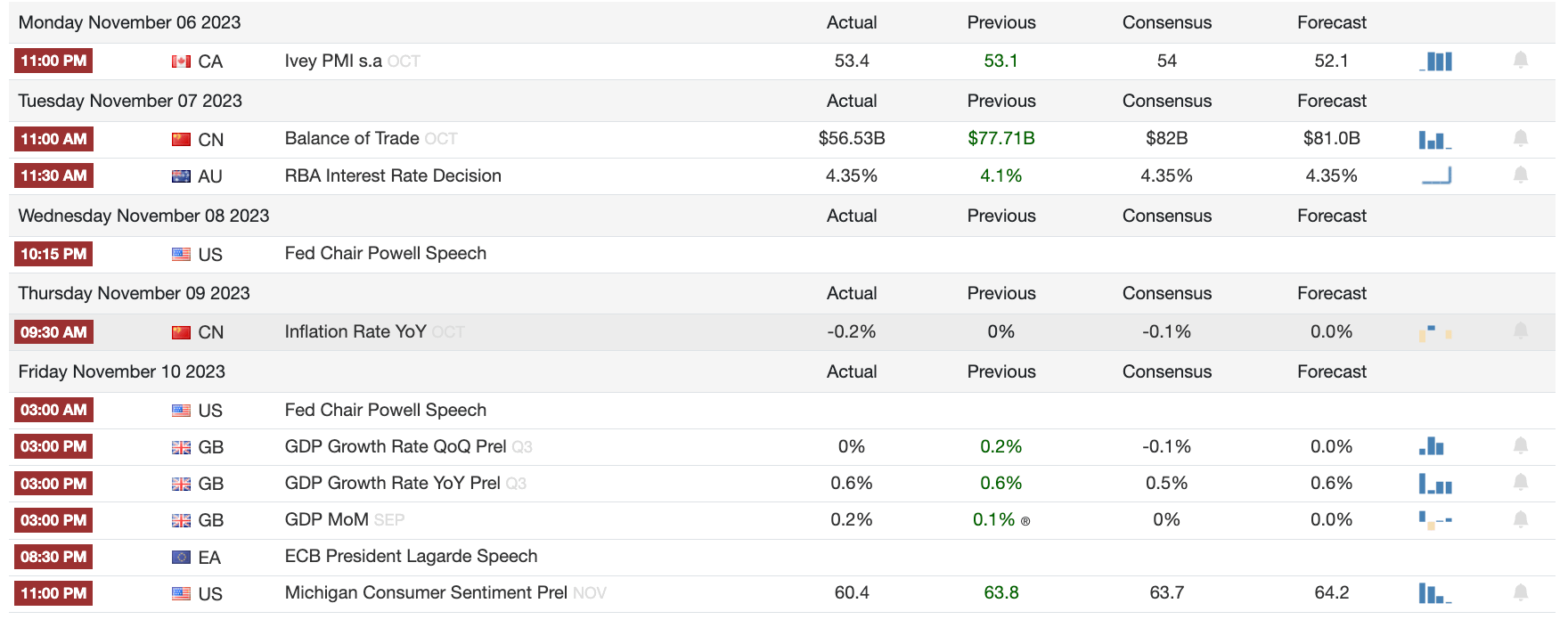

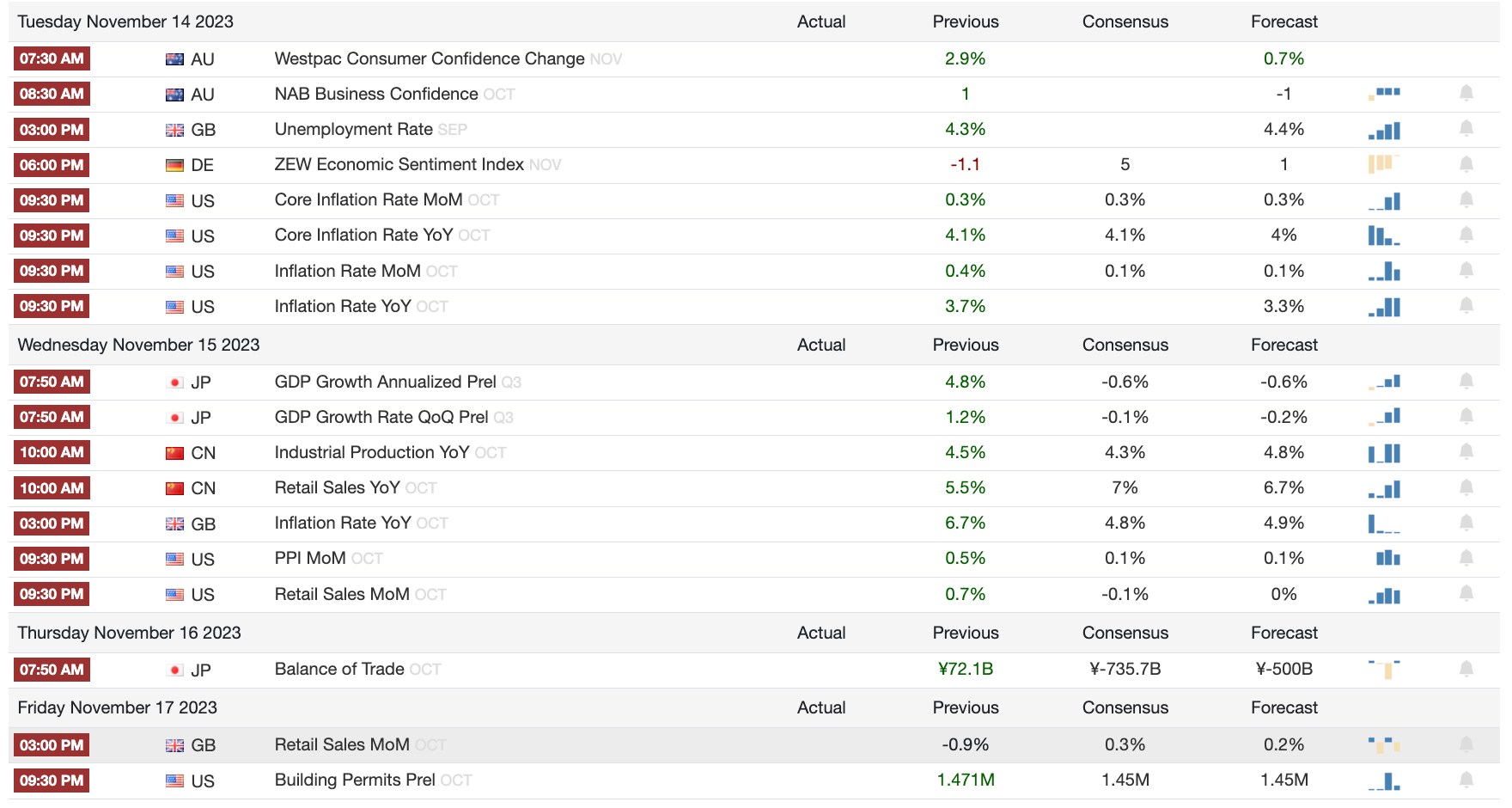

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

1️⃣ Macro events for the week

Last Week

Next Week

2️⃣ Bitcoin Buzz Indicator

Crypto Market Updates

BlackRock's Ethereum Trust: A New Institutional Milestone

SEC's Bitcoin ETF Review: A Market Game Changer

Hong Kong Opens Crypto ETFs to Retail Investors

Binance Launches Web3 Wallet Amid SEC Scrutiny

Banking and Regulatory Updates

Major Investments in Crypto Startups by SC Ventures and SBI

Global Firms Embrace Crypto Expansion

China Criminalizes Theft of Digital Collections

Country-Specific Developments

Rise in UK Cryptocurrency Scams: Lloyds Bank Report

Crypto Exchanges and Platforms

Poloniex Hack: Over $100 Million in Crypto Stolen

Celsius Emerges from Bankruptcy with New Plans

Elon Musk's xAI Unveils Grok: A New AI Chatbot

"The Simpsons" Episode Boosts NFT Interest

UV Light Incident at ApeFest: Legal Action Ensues

OpenSea Valuation Slashed Amid Market Downturn

Roblox CEO Discusses NFTs and Digital Object Portability

Altcoins

SK Telecom launched a Web3 wallet in collaboration with Aptos and Atomrigs Lab.

Arbitrum DAO approved a proposal for token staking and might use $3.9B from its treasury for this purpose.

Ava Labs cut 12% of its workforce to reallocate resources, as reported by the CEO. Avalanche's C-Chain saw a decline in user activity and transactions in Q3, with a 27% drop in TVL.

Coinbase discontinued support for Bitcoin SV, advising holders to withdraw to avoid potential liquidation.

Cardano-based DEX MuesliSwap announced an upcoming refund site amid user concerns.

Cardano partnered with Polkadot for multi-chain expansion.

HashKey exchange in Hong Kong listed Chainlink for professional investors.

Coinbase and Ether liquid staking tokens like Lido and RocketPool surged following BlackRock's ETH ETF news.

Conflux multichain protocol ceased operations after two years.

FTX sold $200 million in ETH and $30 million in SOL without significantly impacting their prices.

Evmos discontinued Cosmos support, focusing on Ethereum-based transactions.

Scroll became the third most active Ethereum Layer 2 by throughput, overtaking ZkSync Era, boosted by a Scroll Origins NFT promotion.

Genesis sought court permission to reduce its 3AC claim from $1B to $33M.

FTX aimed to sell Grayscale and Bitwise assets worth $744M, with its FTT Token jumping 90% after Gensler's comments.

Crypto lender Hodlnaut faced liquidation, as revealed in a court filing.

Blockchain game Illuvium is prepared for an Epic Games Store release.

Taiwan detained key JPEX personnel amid fraud investigations.

JPMorgan Coin introduced programmable payments, with FedEx as an early adopter.

Kraken explored solutions for industry challenges, amidst layer-2 speculations.

Monero's community wallet was emptied following an attack.

Near Foundation and Polygon Labs teamed up for a ZK solution. NEAR CEO declined Wintermute's USN token swap offer, leading to a potential lawsuit.

OneCoin's legal head admitted to money laundering and wire fraud.

Polygon's MATIC token rose 21.15% in a week, with a 54% market cap increase in three weeks. Significant accumulation was noted among addresses holding 100,000 to 10 million MATIC.

Polygon Labs launched a $85M grant program to attract developers.

HSBC collaborated with Ripple's Metaco for security token custody, with Ripple potentially reducing a $770 million SEC fine.

SafeMoon CEO's bail was delayed due to flight risk concerns.

KuCoin and Gate exchanges announced to list BRC-20 memecoin Sats.

Sui partnered with Space and Time to integrate zero-knowledge tools in Web3 games.

Sushi introduced 'Smart Pools' to enhance LP efficiency.

Tether's USDT supply hit a new high, exceeding 84 billion.

The Graph prepared to launch new blockchain data services, including AI-assisted querying.

Ton Network processed a record 104,715 transactions per second, with Toncoin hitting an 11-month high following Telegram's 'Giveaways'.

USDC announced a 7% fee reduction for stablecoin transactions, with issuer Circle considering a 2024 IPO.

WstETH joined Base after LayerZero's miss.

3️⃣ Market overview

Inflation remains persistent, requiring central banks to maintain tight policy stances. Meanwhile, economic growth is clearly slowing in major economies like China. Markets continue to react to any hints of changes in monetary policy outlook.

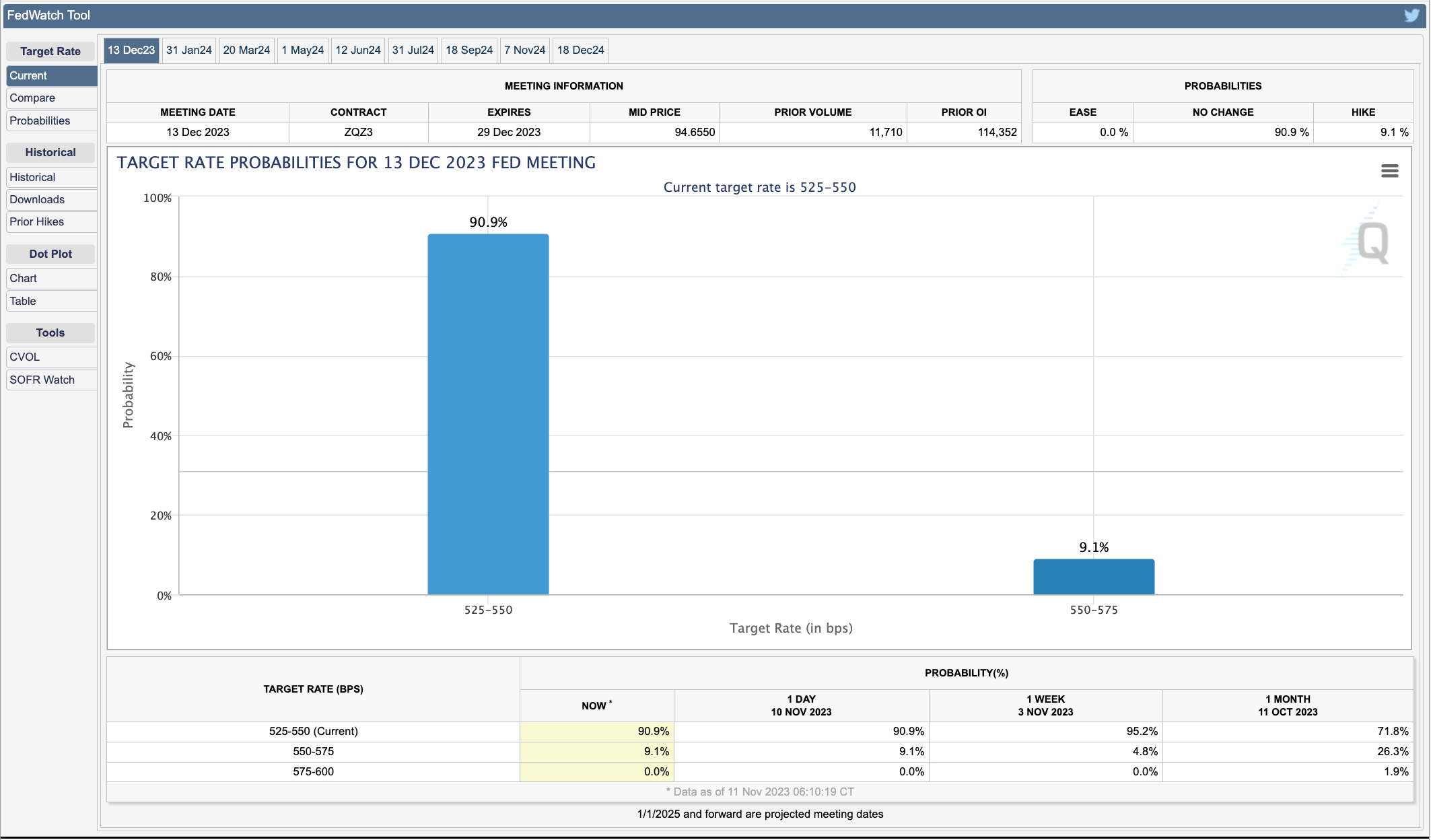

The Federal Reserve is signaling that more interest rate hikes are likely needed to control inflation, despite calls from some for a pause. This indicates the Fed's commitment to bringing down inflation even if it risks economic growth.

China continues to see deflationary pressure with both consumer and producer prices declining. This points to weak domestic demand and the need for further policy support.

US stocks snapped their longest rally in two years, showing the market is still sensitive to interest rate uncertainties. Key sectors like healthcare underperformed.

4️⃣ Key Economic Metrics

🟢 We’re likely headed towards a soft landing. Here are some factors:

Job growth slowed in October, signaling the labor market is cooling and inflationary pressures may be easing. This raises hopes the Fed can stop raising rates soon.

Wage growth moderated in October, another sign of easing inflationary pressure.

The Fed left rates unchanged at its November meeting and noted financial conditions have tightened, likely weighing on growth and inflation. Markets reacted by pushing down yields and the dollar.

The job openings rate rebounded slightly in August-September after declining over the summer. The labor market remains historically tight.

Compensation growth slowed a bit but remains high at 4.3% annually in September. The Fed likely needs to see more slowing to be comfortable easing policy.

Long-term Treasury yields have fallen about 40 basis points recently as central banks signal an end to tightening and inflation falls faster than expected. Supply and demand factors in the bond market also contributed.

Productivity rebounded in Q2 while unit labor costs declined, a positive sign for the inflation outlook. This supports the soft landing scenario.

Yields are still relatively high historically and likely to remain elevated due to large government borrowing needs, business investment demand, and possible reduced foreign buying.

Twitter: https://twitter.com/arndxt_xo/status/1723327505896276089