Yet, we focus on irrational criticism instead of recognizing institutional signals.

Despite 95% of crypto investors losing money, $ETH—up +50% in two months and consolidated at a macro level—is being quietly accumulated by BlackRock.

Here are 4 big indicators that tells you we are set up for a big run👇🧵

Macro Pulse Update 16.11.2024, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ China Spotlight

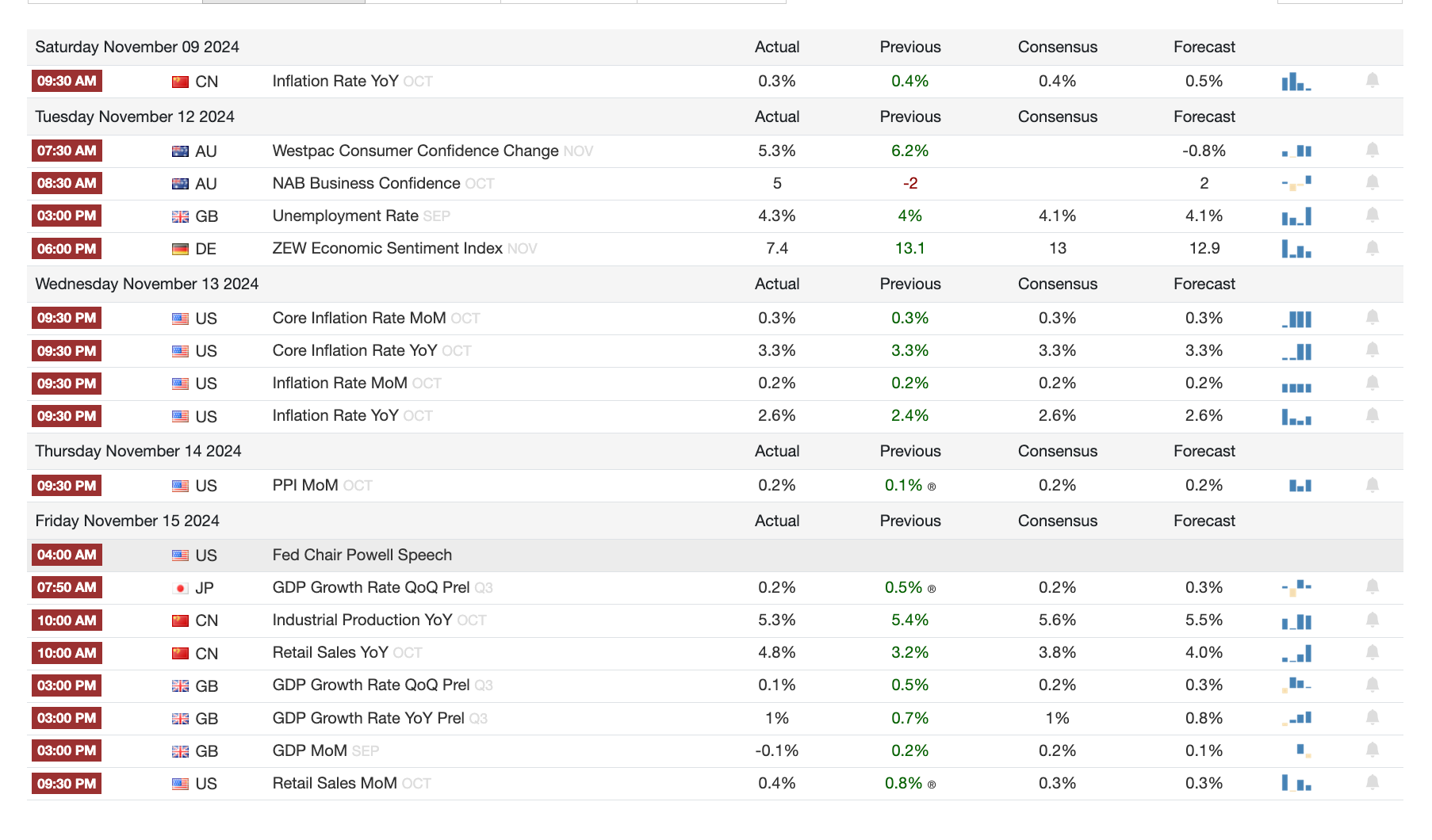

1️⃣ Macro events for the week

Last Week

Next Week

2️⃣ Bitcoin Buzz Indicator

Meme Coins and Market Reactions

Dogecoin Surges After Trump Launches DOGE Initiative

Binance Criticized Over Solana Meme Coin Listings

Regulatory Developments

XRP Hits Yearly High Amid Regulatory Speculations

Institutional Blockchain Adoption

Franklin Templeton Expands Money Market Fund to Ethereum

BlackRock Expands BUIDL Fund to Five Blockchains

Regulatory Probes and Legal Actions

Polymarket CEO's Home Raided Amid Regulatory Probe

NFT Market Trends

Doodles Teams Up With McDonald's for Holiday Campaign

OpenSea Trading Surges Amid Token Launch Speculation

98% of 2024 NFT Collections Are Now "Dead"

")

Altcoins

FTX accused Binance and CZ of causing its collapse, seeking $1.7 billion in a new lawsuit.

Canary Capital filed for a first-of-its-kind Hedera HBAR spot ETF with the SEC.

L2 news: Lisk set to airdrop 15M tokens, and Zerion launched the ZERO Network on Ethereum L2.

ConsenSys decentralizes Linea, transferring governance to the community.

Tether introduced an RWA platform to enable the tokenization of assets.

Revolut expanded its crypto exchange to 30 more European markets.

PayPal USD integrated LayerZero, enabling cross-chain transfers.

ZKSync approved distributing 325M ZK tokens to boost cross-chain liquidity.

Phantom issued an emergency patch after an update disrupted iOS wallet access.

PancakeSwap launched a Telegram bot for direct trading within the app.

Kraken’s Layer 2 Ink released fault-proof tech in its initial stage.

South Korea’s Upbit faces investigations over 500,000 KYC violations.

Aave sought community feedback on expanding to Bitcoin Layer 2 Spiderchain.

Alameda Research sued the Waves founder to recover $90 million.

World Liberty Financial, backed by Trump, integrated Chainlink and teased cross-chain features.

3AC liquidators aimed to revise claims against FTX from $120M to $1.53B.

Litecoin rebranded as a memecoin, sparking discussions in the crypto space.

Delta Prime suffered its second exploit in two months, with losses exceeding $10M.

Blur proposed adding trading fees and removing creator fee guarantees.

Coinbase launched the COIN50 index, available as a perpetual future with 20x leverage.

Bitwise debuted an Aptos staking ETP on the SIX Swiss Exchange.

3️⃣ Market overview

Crypto Market

Bitcoin’s Price Surge Leads to $700 Million in Liquidations: BTC spiked above $93,000 this week before settling below $90,000, driving over $700 million in liquidations. The price remains up over 15% for the week, with both bulls and bears impacted.

FTX Sues Binance and CZ Over $1.76 Billion Deal: FTX filed a $1.76 billion lawsuit alleging fraudulent transactions during a 2021 share repurchase. The suit claims customer funds were misused, contributing to FTX's liquidity crisis and collapse.

Tesla’s Bitcoin Holdings Top $1 Billion Amid Stock Rally: Tesla's BTC holdings surged past $1 billion after Bitcoin's rally. The company’s stock jumped over 20% this week, reflecting renewed investor optimism despite recent volatility.

Spot ETH and BTC ETFs See Record Inflows: Spot ether ETFs posted a record $295.5 million in daily inflows, pushing total AUM to $9.43 billion. Spot bitcoin ETFs saw $1.1 billion in inflows, led by BlackRock’s IBIT with $756.5 million.

Dogecoin Rallies on Trump’s Appointment of Musk to Lead DOGE Initiative: President-elect Trump named Elon Musk to head the Department of Government Efficiency (DOGE), fueling Dogecoin hype. DOGE’s price surged to $0.38 amid growing excitement over Musk’s plans for federal spending transparency.

Macro Market

Fed’s Gradual Policy Path: Jerome Powell’s emphasis on patience in rate cuts reflects confidence in the U.S. economy’s resilience and stable labor market. However, persistent inflation and potential policy shifts under the new administration may shape future decisions.

Japan’s Mixed Economic Signals: While overall GDP growth slowed, strong private consumption (+0.9%) highlights underlying consumer strength, despite weak exports and reduced capital spending.

Market Volatility Linked to Fed and Fiscal Policies: U.S. equities reacted negatively to Powell’s comments, reducing rate cut expectations for December and reflecting inflationary pressures. Specific sectors like industrials and EVs were particularly affected by policy concerns and potential tax credit changes.

Global Economic Outlook: Key data releases from the U.S. (Retail Sales) and China (industrial and investment metrics) will be crucial for gauging consumer sentiment and industrial performance in the two largest economies.

Shifts in Market Sentiment: Market players are recalibrating expectations in light of inflation trends, resilient employment data, and geopolitical developments, signaling a cautious yet watchful approach to upcoming opportunities.

4️⃣ Key Economic Metrics

🔴 US Macro Economy

Deficit and Debt Levels Are Historically High

The US budget deficit in FY2023 was 6.7% of GDP—historically high during peacetime.

Federal debt/GDP ratios remain elevated, with public debt excluding Federal Reserve holdings at 74.5%, a level last seen post-WWII.

Immediate Consequences Are Muted

Despite high debt, borrowing costs and inflation have not spiked significantly, with parallels drawn to Japan’s debt resilience.

Global demand for US Treasury securities, underpinned by the US dollar's dominance, provides fiscal leeway.

Risks Remain on the Horizon

Overleveraging could trigger investor fears of inflation or default, leading to financial instability.

Historical cases like Germany (1920s) or Greece (2010s) highlight risks of excessive debt, though the US benefits from unique privileges.

Structural Issues Drive Long-term Challenges

Aging demographics and entitlement programs (e.g., Social Security, Medicare) are primary deficit drivers, exacerbated by stagnant workforce growth.

Technological advances in healthcare could alleviate costs but remain speculative.

Action Likely Only Under Pressure

Historically, policymakers address deficits only when financial markets force their hand. James Carville’s quip about the bond market remains prescient.

🟢 Federal Reserve Eases Monetary Policy

Policy Adjustments: Recent 25-basis-point rate cut places the Federal Funds rate between 4.5%-4.75%, following a prior 50-basis-point cut in September.

Market Reactions: Equities rose on fiscal stimulus expectations, while bond yields increased due to anticipated inflation from potential tax cuts and tariffs.

Data-Driven Outlook: The Fed’s neutral stance reflects concerns over inflation, strong economic activity, and labor market resilience, balancing the lagged impact of tight monetary policy.

Commercial Property Concerns: Hybrid work has reduced office demand, increasing mortgage delinquencies. While easing could alleviate some pressure, slow policy shifts might exacerbate risks.

🟢 US Labor Productivity Growth

Strong Productivity Gains: Labor productivity rose 2.2% annually in Q3 2024, with services outpacing manufacturing for the first time, signaling adoption of labor-saving technologies.

Inflation Dampening Effect: Unit Labor Costs rose modestly at 1.9%, with productivity gains offsetting wage increases, easing inflationary pressures.

Global Contrast: The US leads industrialized nations in productivity growth, offering flexibility for monetary policy and highlighting opportunities for technological advancement in services.

Twitter: https://x.com/arndxt_xo/status/1858104556858814639