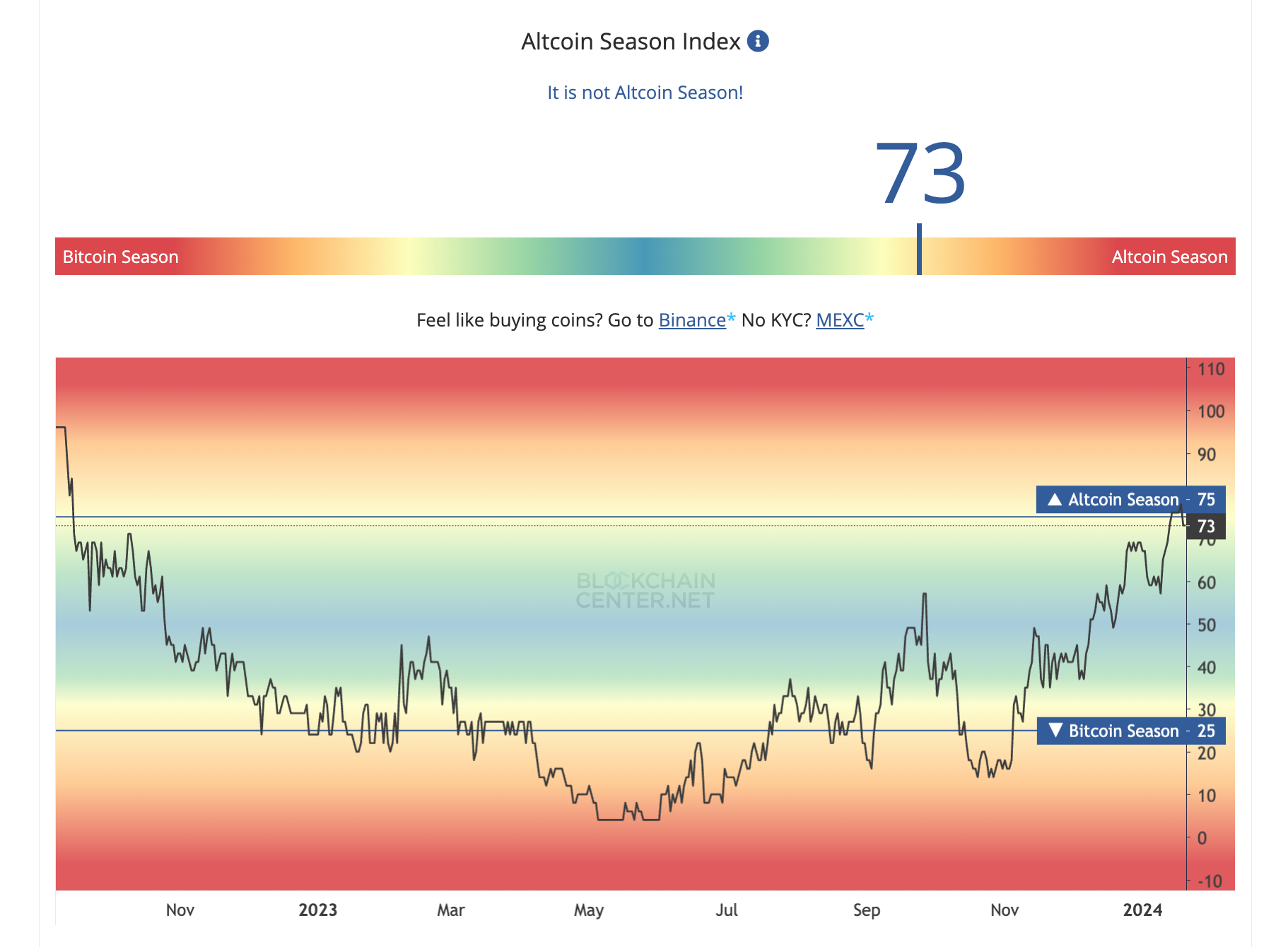

We’re in an ALTCOIN SZN!

$BTC dump left a liquidity gap, bounce incoming

$ETH may see $2,800

Here’s 3 indicators of bullish sentiments 👇🧵

Macro Pulse Update 20.01.2024, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ China Spotlight

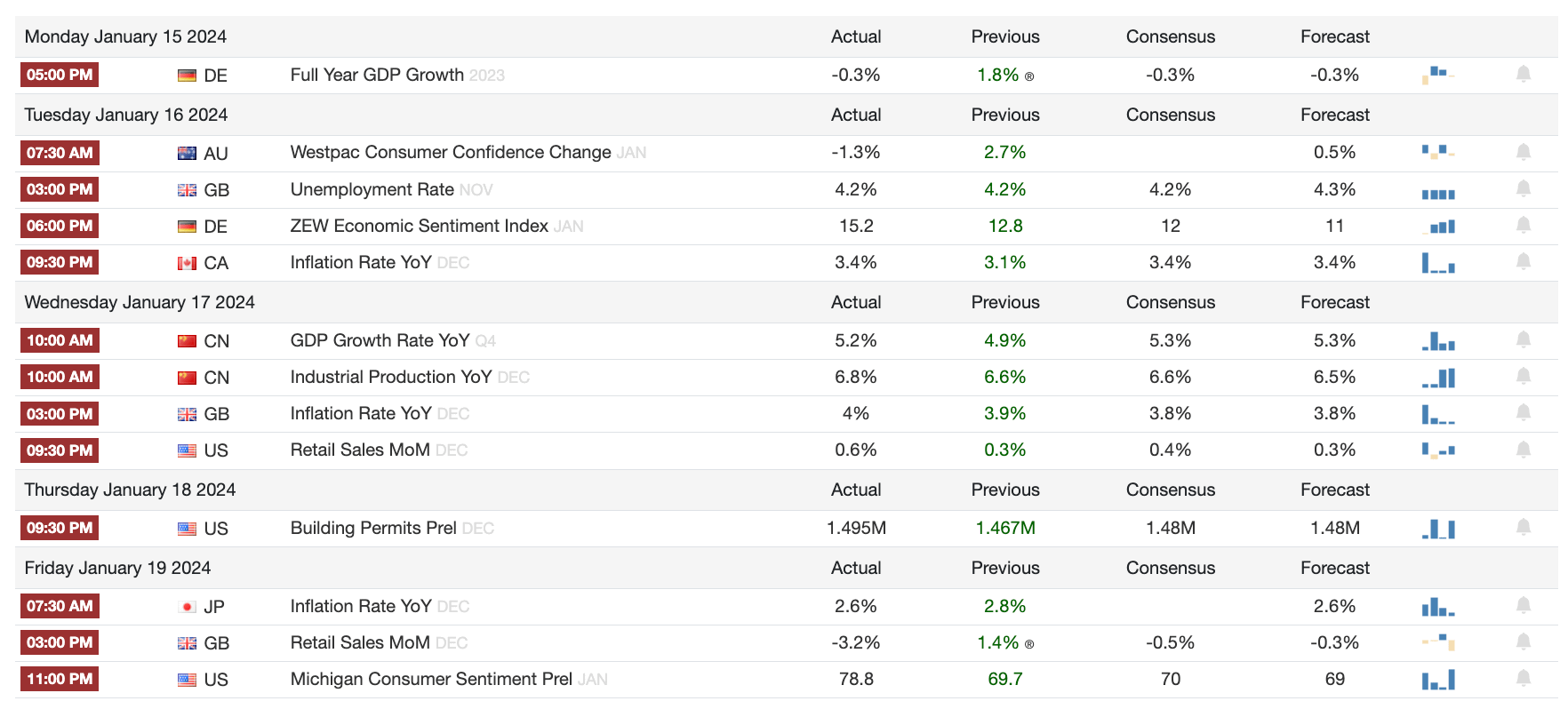

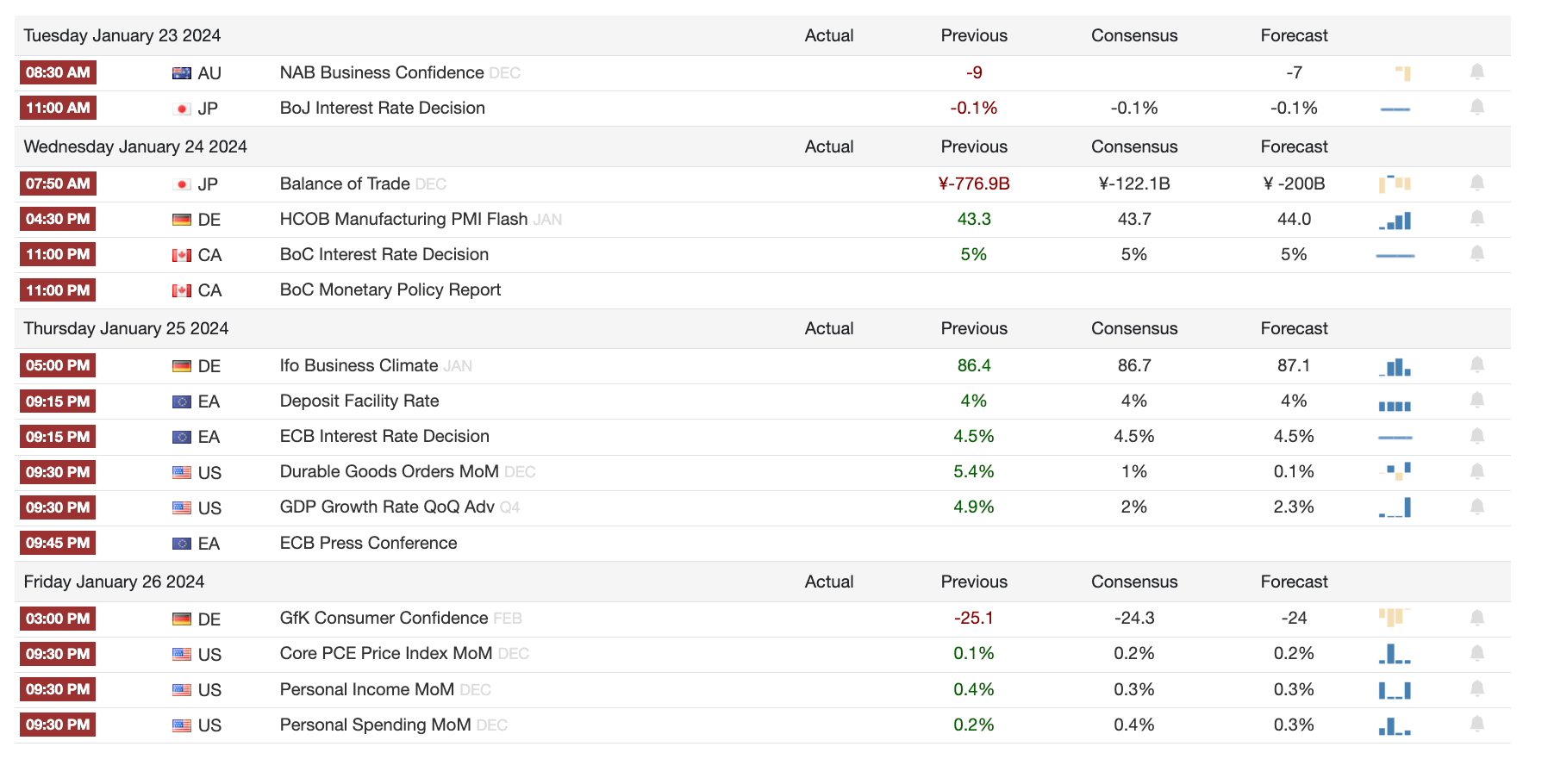

1️⃣ Macro events for the week

Last Week

Next Week

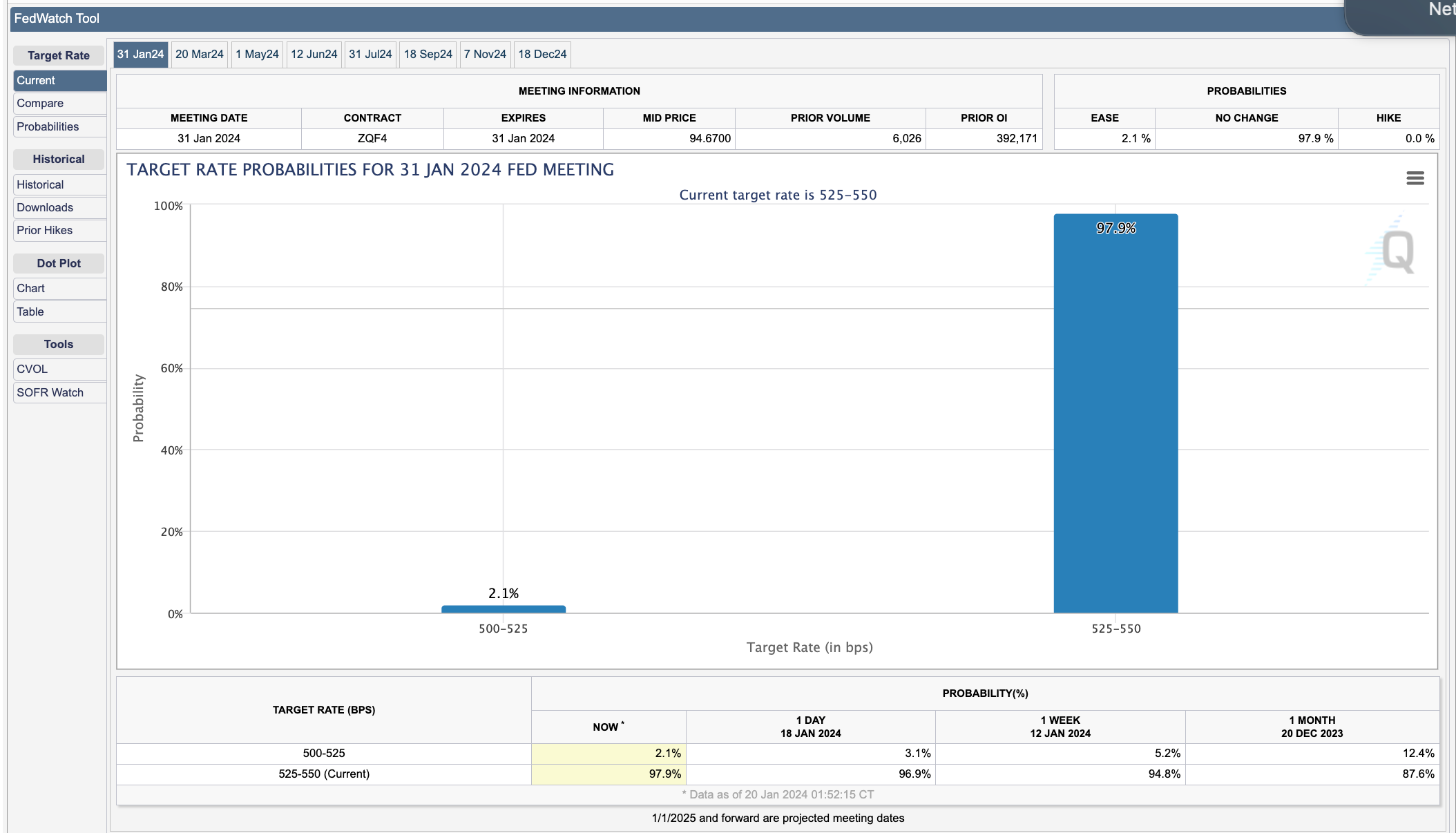

2️⃣ Bitcoin Buzz Indicator

Market and ETF Updates

Bitcoin ETFs Surge in US Market

Ethereum's Comeback: ETFs and Market Recovery

XRP in the Spotlight: False Whale Alert and Market Moves

Exchange and Stablecoin Updates

TrueUSD Faces Depegging Crisis Amid Market Fluctuations

Coinbase vs SEC: Defining Crypto Investments

Tether's USDT Scrutinized for Money Laundering Concerns

Cryptocurrency and Blockchain Developments

Hong Kong and Global Markets Embrace Bitcoin ETFs

Solana's Mobile Success and DeFi Developments

Manta Network's Challenges Amidst Token Launch

NFT and Digital Collectibles

NFT Market Cleans Up: Low Wash Trading Volumes

Trump's Unique Bitcoin NFT Venture

OpenSea 2.0: Innovating the NFT Marketplace

Altcoins

Fantom reduced validator stake requirements by 90% to 50k FTM.

Sui and Celestia achieved new all-time highs.

Google Cloud joined Flare Network as a validator, resulting in a FLR price jump.

Xai Gaming Token's value surged as its airdrop reached $140 million.

OKX secured a Dubai license while Binance launched a Thailand exchange.

Metis launched a decentralized sequencer on testnet amid significant growth.

HashKey Group completed a $100M Series A funding round, reaching a $1.2B valuation.

Chainlink integrated with Circle's CCTP protocol for USDC cross-chain transfers.

Multichain's CEO reappeared on Telegram amid investor queries.

Socket protocol lost $3.3M in a confirmed approval exploit.

Sam Bankman-Fried's parents requested dismissal of an FTX clawback lawsuit.

IRS delayed crypto reporting requirements, simplifying taxes.

Ripple considered an IPO outside the US amid SEC challenges.

SEC v. Terraform Labs trial postponed to March, possibly to accommodate Do Kwon.

Gemini received approval to operate in France, set to launch within weeks

Algorand cut block times by 20% with Dynamic Lambda upgrade.

Frax Finance's Layer 2 Fraxtal set to debut in February.

dYdX on Cosmos surpassed Uniswap v3 on Ethereum in daily trading volume.

Blockchain firm accused Polygon of suspicious transfers, causing a MATIC dump. Woo raised $9M to enhance liquidity of WOO X Exchange.

Cristiano Ronaldo's lawsuit against Binance over NFT promotions likely heading to trial.

Arbitrum launched a program to support custom chain development.

Uma token surged by 90% after indicating a focus on MEV solutions.

3️⃣ Market overview

Appetite for tech remains strong, with AI advancements and growth outlook outweighing uncertainties around the interest rate trajectory.

Bitcoin entered a consolidation phase after the initial volatility from the spot ETF approvals last week. Price has traded in a tight range between $41k-$43k as the market digests the news.

Early spot bitcoin ETF trading data is very positive, with over $900 million in net inflows in the first 3 days. IBIT saw the largest inflows while GBTC saw expected outflows due to its higher fees.

Ether continues to gain ground on bitcoin, with the ETHBTC pair pushing back above 0.06. This appears partly driven by anticipation of a potential spot ether ETF approval later this year.

Solana rebounded back above $100, likely helped by the hype around its new smartphone announcement. The Jupiter token launch at month's end is also building excitement.

4️⃣ Key Economic Metrics

🟢 Inflation shows early signs of easing but the Fed can't let up yet until wage and labor market pressures abate further. The path to lower rates is still there but the timeline remains data dependent.

Headline inflation accelerated in December, with the CPI up 3.4% year-over-year. However, core inflation declined to 3.9%, the lowest level since May 2021.

Shelter costs continue to be the biggest driver of inflation, but there are signs this could moderate as house price growth slows. Excluding shelter, inflation is quite low at just 1.9%.

Producer prices declined in December, falling 0.1% from November. This signals that pipeline inflation pressures are easing which could feed through to lower consumer prices.

The job market remains very tight with initial jobless claims staying near historically low levels. This suggests the Fed still has more work to do in cooling the labor market and wages.

While headline CPI was high, the decline in core inflation and producer prices are more encouraging. The Fed will likely take a balanced view, meaning a pause in rate cuts could happen but is not guaranteed.

🟢 EU consumer spending remains weak but leading indicators like wages point to a moderate recovery ahead. The very tight employment picture complicates the inflation fight and suggests the ECB could lag other central banks in easing policy

Retail sales volumes stagnated in November, falling 0.3% from October and down 1.1% year-over-year. Sales were dragged down by Germany and remain depressed across most categories.

Real wages are starting to recover and interest rates are seen peaking soon which could provide a boost to consumer spending in the second half of 2024.

The Eurozone job market stays resilient with unemployment hitting a record low of 6.4% in November. Rates held steady in Germany despite its recession.

Labor market tightness is driving faster wage growth over 5% annually. This makes the ECB's 2% inflation target harder to attain and is why they want to keep rates higher for longer.

5️⃣ China Spotlight🔴

China faces an uphill battle with persistent deflation and exports under pressure. But areas like EVs showcase the economy's capacity to lead in strategic sectors via state support and industrial policy.

China continues to grapple with deflation, with consumer prices declining 0.3% year-over-year in December. Producer prices also keep falling, signaling excess capacity in the economy.

Weak domestic demand and excess supply appear to be driving deflation. The government is reluctant to pursue aggressive stimulus due to debt concerns and the risk of currency devaluation.

China's exports declined 4.6% in 2023, the first annual drop since 2016, reflecting cooling global demand and supply chain shifts away from China. Exports to the US posted the largest decline on record.

However, auto exports have been a bright spot, driven by electric vehicles. China aims to become the world's top auto exporter in 2024, with EVs making up 30% of overseas shipments.

Domestically, EV adoption is soaring, accounting for 17% of China's car market. Chinese brands dominate with 84% share, pointing to the industry's potential as a global growth engine.

Twitter: https://twitter.com/arndxt_xo/status/1748664454928314601