🚨 Red alert! 🚨

China EV invasion of Europe sparks subsidy probe and tariff tensions.

8 factors that determine the rate hike outlook 👇🧵

Macro Pulse Update 23.09.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ China Spotlight

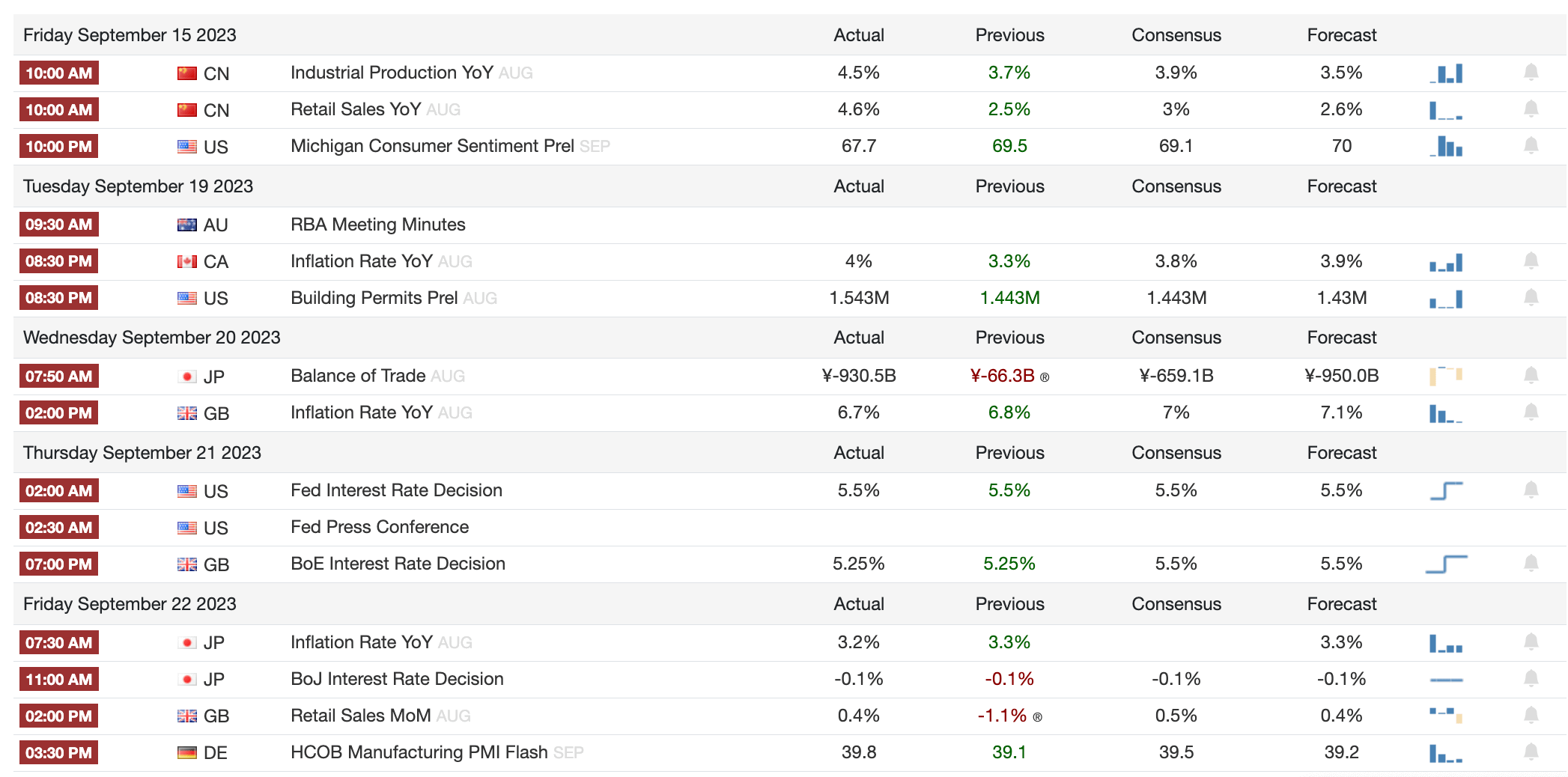

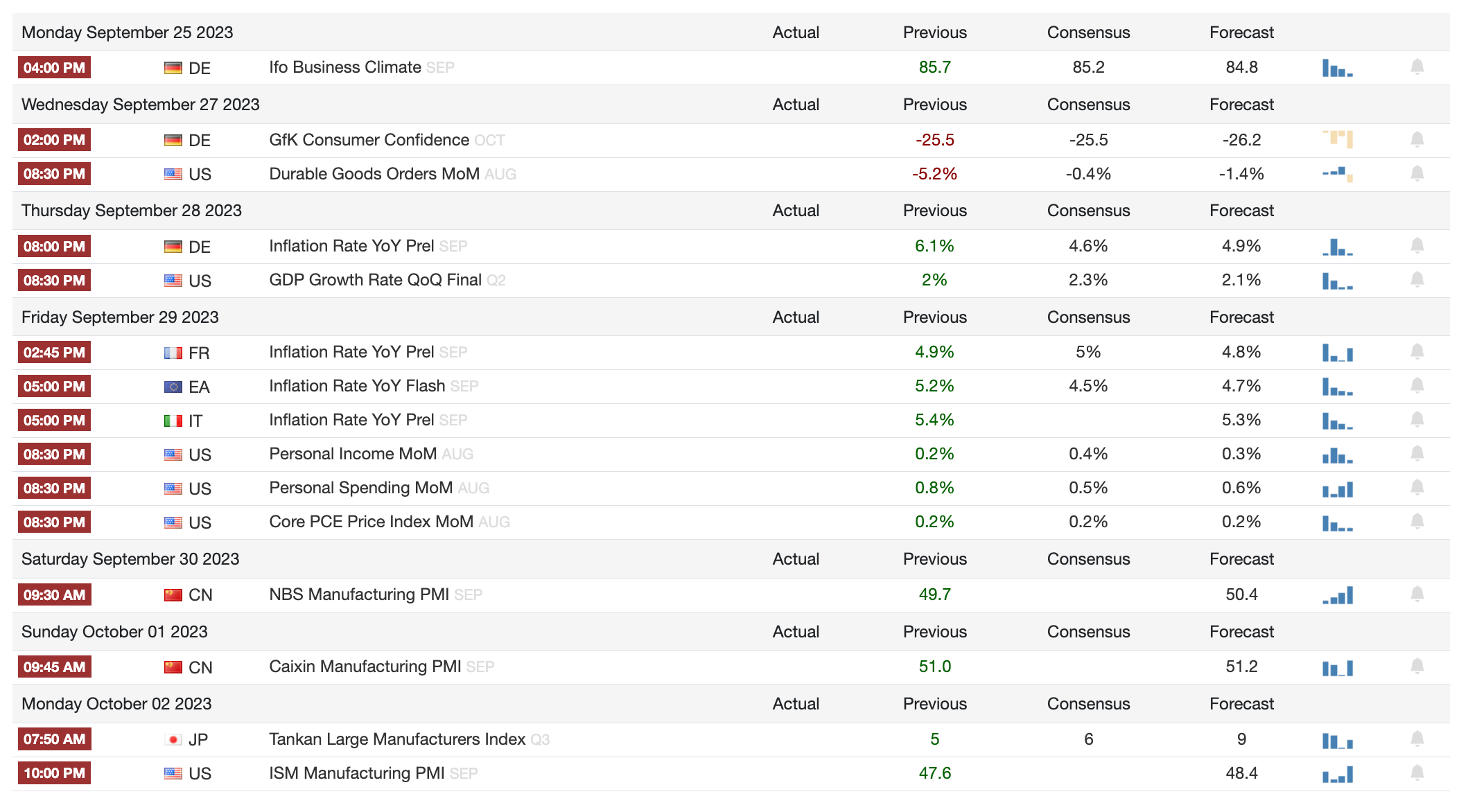

1️⃣ Macro events for the week

Last week

Next week

2️⃣ Bitcoin Buzz Indicator

Banking and Regulatory Updates

Citigroup Dives into Tokenized Bonds with BBX

Mt. Gox Credit Repayment Extension Shakes Crypto Market

Laser Digital Launches Bitcoin Adoption Fund

Binance Fights SEC Lawsuit with Dismissal Motion

FCA Tightens Crypto Advertising Rules in the UK

Crypto Exchanges and Legal Troubles

JPEX Exchange Fraud Case Intensifies in Hong Kong

Bankrupt FTX Sues Salameda to Recover Millions

Bybit Suspends UK Operations Amid FCA Changes

Tech and Security News

Google Cloud Adds 11 New Blockchains to BigQuery

Nansen Discloses Security Breach Affecting Users

The Evolving NFT Space

OpenSea's Royalty Cuts Shift NFT Creator Landscape

Polygon and Solana See NFT Ecosystem Fluctuations

Stoner Cats NFT Faces SEC Scrutiny, Prices Surge

Altcoins:

ApeCoin DAO voted to create a sister DAO for influential NFT acquisitions.

Balancer's frontend suffered a DNS attack, losing over $250K.

Wintermute transferred 7.3 million Blur tokens to two exchanges.

Canto surged 13% after announcing a move to Ethereum as a layer 2 network.

Polygon Labs suggested using CDK to help Celo migrate to Ethereum's layer 2.

OPNX's $30M bid for Hodlnaut was turned down as FLEX token tanked by 90%.

ImmutableX rose 25% due to a price surge driven by South Korean traders.

Nexo earned CSA STAR Level 1 Certification, boosting its security and transparency.

MakerDAO's MKR approached a 16-month high, fueled by whale accumulation and a bullish crypto hedge fund.

Optimism Foundation's $157M token sale shook the market following its third airdrop.

Toncoin entered the top 10, gaining 30% in a week.

Circle launched its native USDC stablecoin on both Polkadot and NEAR.

3️⃣ Market overview

Central banks remain focused on tightening monetary policy to combat high inflation, though there are some early signs of inflation peaking. This is leading to market volatility as investors weigh recession risks. The path of inflation and central bank policy will remain key drivers of markets in the months ahead.

The Fed is expected to interest rates by 0.75% in 2023 and indicated rates will remain high through 2024 to combat inflation. This led to a sell-off in stocks as investors anticipate slower economic growth.

UK inflation slowed more than expected in August, reducing pressure on the BoE to continue aggressive rate hikes. However, the BoE is still expected to raise rates.

US stocks declined after the Fed announcement, with the Nasdaq down 1.5%. Megacaps like Microsoft and Nvidia dragged down major indices.

Oil prices also declined, with WTI dropping below $90 and Brent below $93 per barrel, as recession fears mounted.

4️⃣ Key Economic Metrics

Key will be watching trends in core inflation and shelter costs. If those continue declining, it would support a less aggressive Fed stance. But further energy price spikes could renew focus on headline inflation.

🟡 Headline CPI inflation rebounded to 5.7% in August due to rising energy prices. However, core CPI inflation (excluding food and energy) declined to 4.3%, the lowest since September 2021.

🔴 Shelter inflation continues to be high at 7.3% but has fallen from a peak of 8.2% in May. As housing prices stabilize, shelter inflation should continue to moderate.

🟡 Prices of durable goods fell 2% over the past year, while prices of nondurable goods rose just 0.6% excluding food.

🟢 Declines were seen in some services like airfares (-13.3%). This indicates underlying inflation pressures may be easing.

🟡 The rise in energy prices remains a concern that could feed into other prices. But supply restrictions have likely peaked, and demand may ease with slowing growth.

🔴 The data provides ammunition for both hawks and doves at the Fed. Markets expect at least one more rate hike this year, but a pause in 2024 as the impacts of tightening are felt.

5️⃣ China Spotlight

China Economy 🔴

While recent data shows a modest rebound, the economy faces persistent drags. Policy support so far has been cautious. More policy easing may be needed to stabilize growth.

Retail sales and industrial production rebounded modestly in August, suggesting the economy is stabilizing somewhat after a weak July.

However, fixed asset investment growth continues to decelerate, especially in the property sector where investment fell 8.8% in the first 8 months.

Residential property prices declined further in August, with sales of new homes falling as well. This reflects ongoing weakness in the property sector.

Inflation ticked up slightly in August, with CPI at 0.1% after dipping into deflation in July. But inflationary pressures remain muted overall.

Policymakers have taken some steps to support growth, including easing monetary policy, but face headwinds like a declining workforce and weak private investment.

Major risks include the struggling property sector, still-weak domestic demand, and a difficult external environment with slowing global growth.

China's electric vehicle strength and potential EU retaliation 🔴

China is becoming a major exporter of electric vehicles, with exports quadrupling since early 2021. This comes as domestic demand is weak.

Europe is a key market, accounting for 20% of China's EV exports. Chinese EVs are gaining share due to lower prices.

China's EV strength is attributed to government support, access to battery minerals, and excess production capacity due to unprofitable firms staying afloat.

The EU has announced an anti-subsidy investigation into Chinese EVs, concerned about unfair competition and distortion of its market.

The investigation could lead to punitive tariffs on Chinese EVs. China argues the EU is engaging in protectionism.

Chinese EV prices are estimated to be around 20% below European models. China cites innovation rather than subsidies for its price edge.

The dispute reflects China's strengths in EVs but excess capacity driven by state support. It also shows tensions as China gains share in strategic European industries.

Outcomes could include EU tariffs, Chinese retaliation, and further escalation of trade tensions between the powers.

Twitter: https://twitter.com/arndxt_xo/status/1705541537978003787

This is some next level content, love it