Fed killed the recovery! 😱

New data shows economy skidding off a cliff 📉

7 factors that will go DOOM or BOOM 🧵👇

Macro Pulse Update 26.08.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ China Spotlight

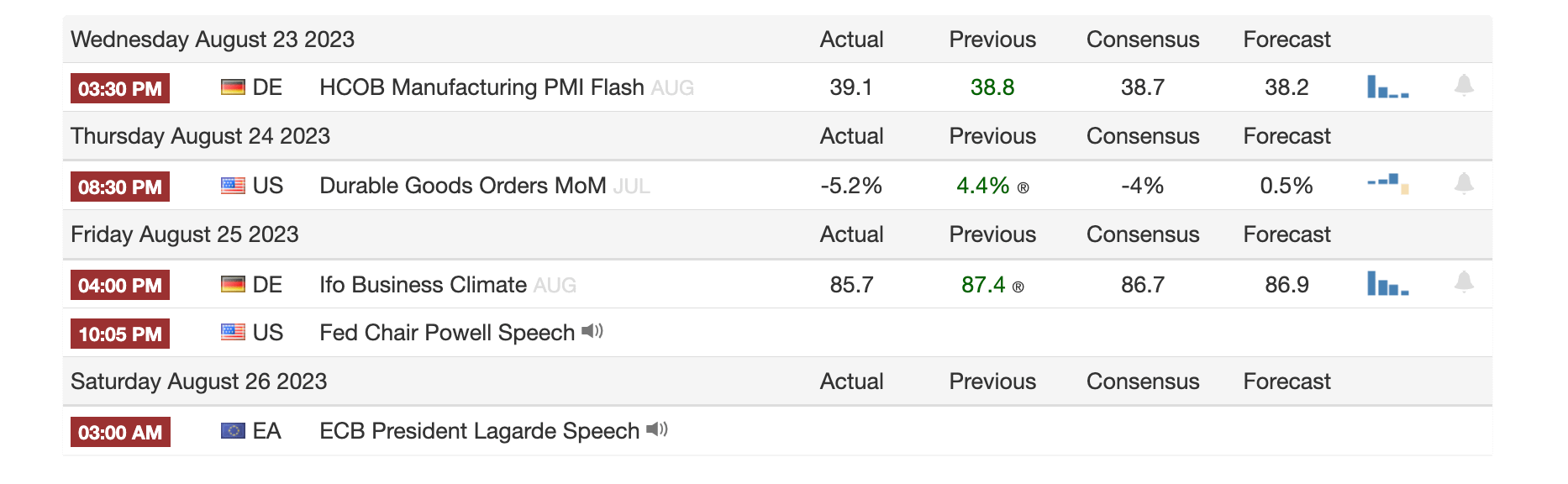

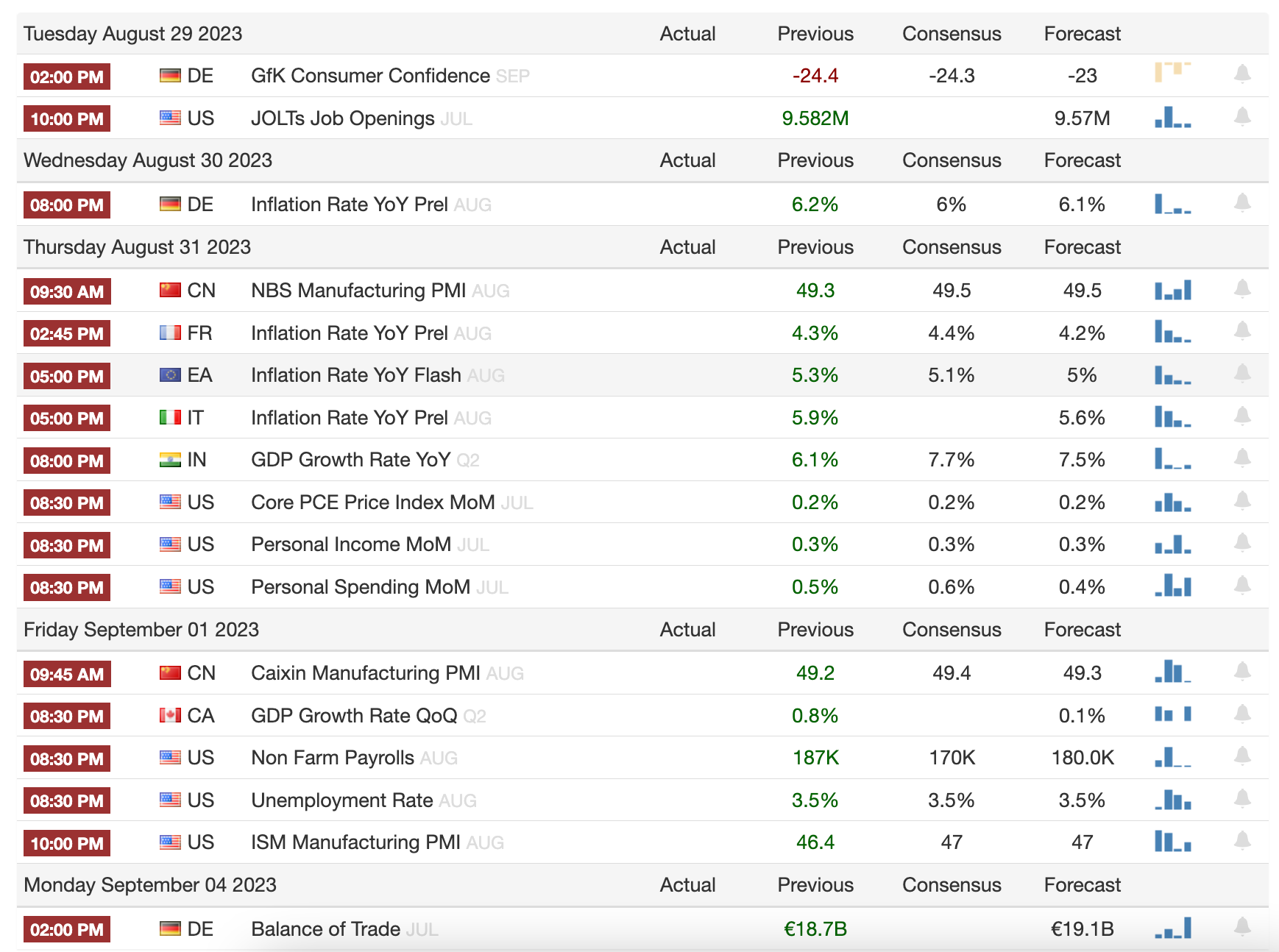

1️⃣ Macro events for the week

Last week (Key event: Jackson Hole)

Next week (Key events: Job openings, PCE, NFP, Unemployment, ISM)

2️⃣ Bitcoin Buzz Indicator

Altcoins

Arbitrum denied outage despite transaction issues

THORChain processed record volume after adding streaming swaps

Dogecoin debated switching to proof of stake, DOGE millionaire's fortune dropped from $3M to $50K

Terra website was hacked

Over $120M in token unlocks last week for Avalanche, Lido, Yield Guild Games

Less than 221 holders had 30% of XRP circulating supply, XRP was top choice of young investors in Korea, XRP whale moved 29M tokens amid price slide

Critical vulnerability was found in some Balancer V2 pools

Thailand warned Meta about crypto scams

CoinDCX cut 12% of jobs amid bear market, taxes

Maple Finance expanded to Asia with $5M investment, returned to Solana

SBF pleaded not guilty at latest FTX hearing

Binance Labs invested in Pendle Finance DeFi platform

NEAR jumped 5% after Nexo integration

99.5% of AVAX holders were in loss as bear market continued

Atomic Wallet faced $100M hack lawsuit

Quantstamp tool detected DeFi flash loan risks

Tornado Cash founders were charged and arrested by FBI

ALGO surged on Cardano partnership potential

Nvidia earnings lifted AI cryptocurrencies (FET, RNDR, AGIX)

Shibarium restart boosted BONE price 15% in one day

Smart money increased dYdX token holdings

1inch joined DeFi projects launching on Base

VeChain and SingularityNET partnered on climate change AI

Lido to complete final token unlock tomorrow

DeFi TVL was at 30-month low amid crypto winter

Litecoin has been down 95% against Bitcoin

Base-based Magnate Finance disappeared in apparent rug pull

Worldcoin's WLD crashed 44% postlaunch

Maker led DeFi tokens with least holder losses

DeFiChain was up 16% as Cake burned ETH staking rewards

Uniswap outperformed Coinbase in spot trading volume in 2023

3️⃣ Market overview

Key things to watch: the resiliency of the U.S. labor market and consumer spending as the Fed tightens policy; whether inflation is truly peaking in major economies; central bank messaging on interest rates at Jackson Hole and beyond. The path of monetary policy and its impact on growth and inflation remains crucial.

The US labor market remains strong overall, as evidenced by the low jobless claims despite some moderation in job growth. This suggests the economy continues to have underlying momentum and demand for workers.

UK consumer confidence rebounded in August, likely helped by falling energy prices, strong wage growth, and easing inflation. This could indicate the UK's cost-of-living crisis may be peaking, though risks like higher unemployment and interest rates persist.

US stocks dropped as investors grow cautious ahead of signals from the Fed at Jackson Hole on further rate hikes. Recent Fed comments indicate rates may still need to rise more.

4️⃣ Key Economic Metrics

Key to watch will be if slowing demand starts impacting the labor market more significantly. For now, risks of recession have risen but a soft landing is still possible. Some cracks are starting to emerge that point to slowing economic momentum, though a recession is not inevitable yet.

🔴 Durable goods orders declined sharply in July, especially core capital goods orders excluding defense and aircraft. This signals some weakening in business investment.

🟡 Labor market revisions showed job growth earlier this year was not as strong as initially thought. Job openings are also declining, suggesting some cooling.

🟡 Higher mortgage rates are weighing on housing demand, with existing home sales falling again in July. New home sales did surprise to the upside though.

🔴 The Fed remains focused on bringing down inflation persistently, signaling further rate hikes are on the table if needed.

Overall, data indicates the economy is losing some steam as the Fed tightens policy. But we haven't seen a substantial rise in layoffs or collapse in demand yet.

What we can expect upcoming

Consumer spending and incomes staying solid so far, helping delay recession predictions. Jobs market also still strong. But manufacturing looks weaker, though not yet signaling imminent recession. Key data to watch for any cracks spreading more broadly.

🟢 Personal Income & Spending (Thursday):

Personal spending expected to rise 0.7% in July, indicating solid consumer demand entering Q3. June saw big gains in durables spending.

Income growth should remain healthy given tight labor market and strong wage gains. This helps support spending.

🟢 Employment (Friday):

Payrolls forecast to rise 160K in August, signaling still-resilient job growth though slower than 2021's rapid pace.

Revisions showed less job growth in 2022 than originally reported, but hiring still holding up amid rate hikes.

🟡 ISM Manufacturing (Friday):

Manufacturing has been in contraction for 9 straight months per ISM data. But new orders rose in July.

Forecast is for a small rise to 47.1 in August, though still in contraction. Manufacturing often more sensitive to rates.

5️⃣ China Spotlight🔴

Overall, while a Chinese hard landing would have global consequences, the spillovers to growth in other major economies may be manageable and not lead to a global crisis. But risks depend on how severe the downturn is and policy responses. Key to watch is whether it stays contained or spreads more broadly.

Concerns are rising about debt levels in China's property sector, leading to worries about an economic "hard landing". China's non-financial corporate debt is very high at around 160% of GDP.

Modeling by Oxford Economics suggests a Chinese hard landing could modestly affect GDP growth in the U.S., Eurozone, and Japan. Effects range from 0.1-0.2 percentage points lower growth.

The effects are muted partly because exports to China are a relatively small share of overall GDP for major economies. However, risks are skewed toward more impact if global financial conditions tighten.

Impacts on inflation could be more meaningful, with around 0.7 percentage points lower CPI inflation in major economies in the model scenario. This stems from lower oil prices and weakened demand.

Twitter: https://twitter.com/arndxt_xo/status/1695394414733164830