Cointelegraph intern started the bullrun

Stocks hurt as yields spike over 5%

5 factors you need to know about the market direction👇🧵

Macro Pulse Update 28.10.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ China Spotlight

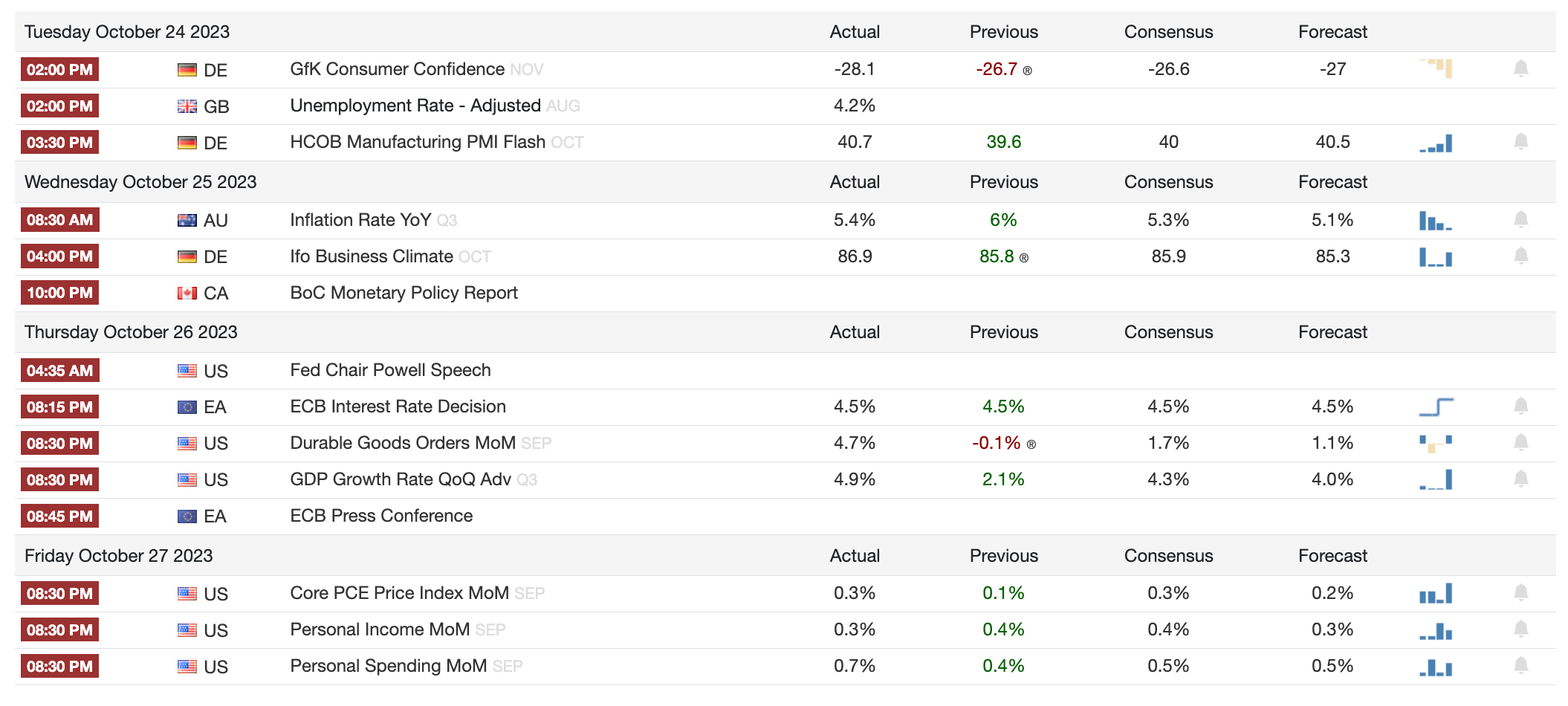

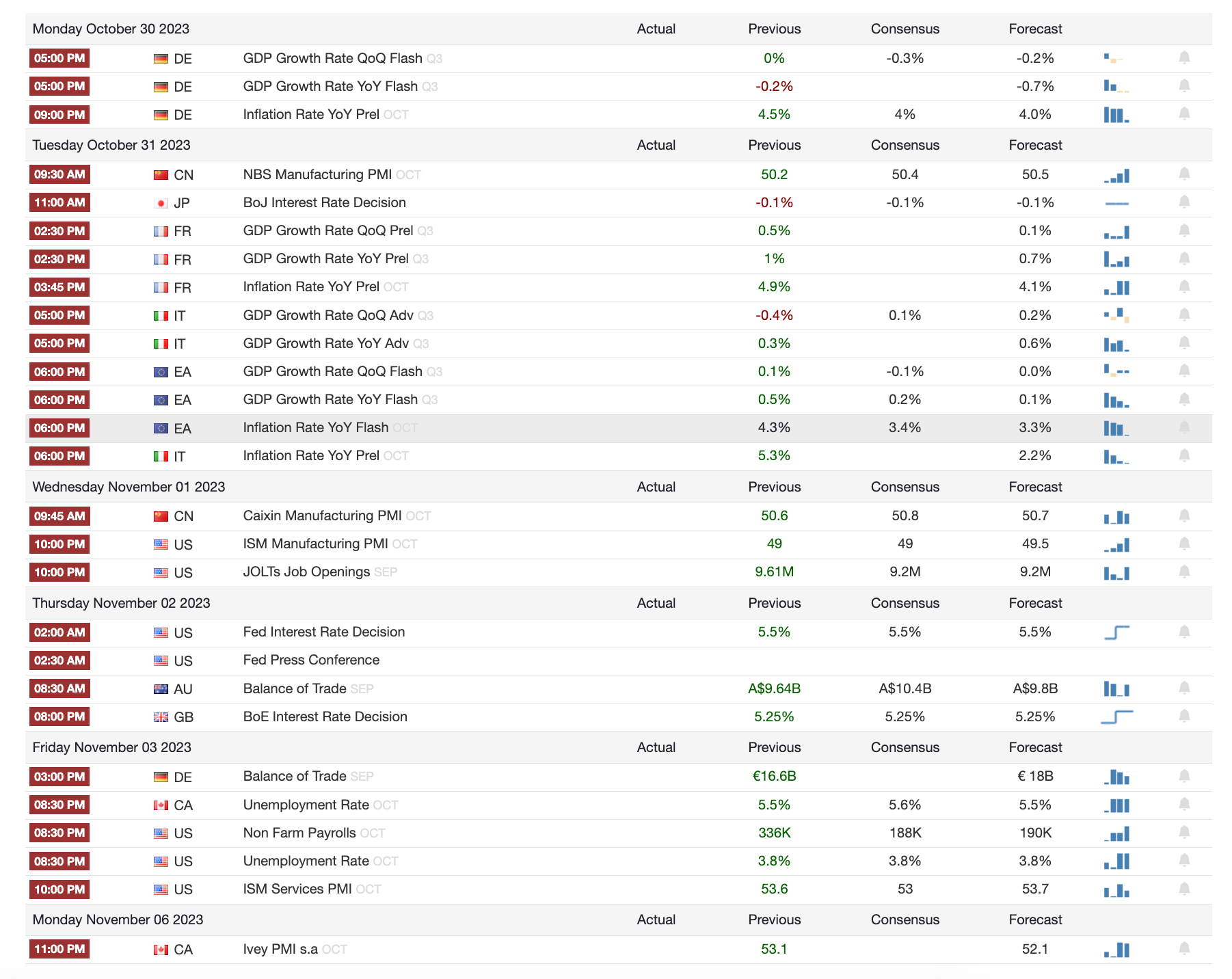

1️⃣ Macro events for the week

Last Week

Next week

2️⃣ Bitcoin Buzz Indicator

Market Movements and Investment Trends

BlackRock's Bitcoin ETF Fuels Market Surge

FTX's Financial Woes and Legal Troubles

Worldcoin's Token Transition and Regulatory Hurdles

Regulatory and Legal Updates

UK Cracks Down on Crypto with New Law

US Lawmakers Target Binance and Tether

Taiwan Introduces Virtual Asset Management Bill

Solana's Growth Strategy Amid Regulatory Caution

Public Perception and Media Narratives

Crypto Funding for Hamas: Fact or Fiction?

Partnerships and Collaborations

Mastercard's Web3 Ventures with MetaMask and MoonPay

NFT News

NFT Market Struggles Despite Crypto Boom

Yuga Labs Wins NFT Copyright Lawsuit

Avant Arte and CryptoPunks Team Up for Prints

Altcoins

Deutsche Bank and SC Ventures swapped stablecoins on UDPN for the first time.

HayCoin (HAY) by Hayden Adams traded at $3M per token with a 4.4 supply, after burning 99.99% of the total.

Binance attracted corporates through Polygon's USDC support.

DCG cooperated with NYAG for months before facing a lawsuit.

Astar Network and KDDI formed a Web3 partnership with a signed MoU.

Parity Technologies laid off 30% of staff to focus on Polkadot's core tech.

Nym launched a $300M fund targeting Web3 wallets, RPCs, and infrastructure.

BlockFi exited bankruptcy and asked clients for withdrawal requests, targeting FTX & 3AC for asset recovery.

Telegram bot Maestro refunded 610 ETH to users following a router exploit.

Polygon's ZK-based token went live on the Ethereum mainnet.

Uniswap Foundation sold $43M in UNI tokens in three days.

Arbitrum integrated Orbit stack with Celestia for data availability.

CyberConnect token rose 30% after Binance Labs invested.

Fantom testnets for Sonic Upgrade estimated a 6,700% throughput gain.

JPMorgan's Coin processed $1B in daily transactions.

Citadel Securities accused Terraform of bad faith over UST depeg allegations.

Justin Sun's HTX and associated firms made a $98M profit in Q3 2023.

Kraken notified customers of upcoming IRS data sharing this November.

LayerZero got Lido community backlash for integrating a wrapped Lido token without LidoDAO approval.

4M LUSD tokens redeemed on Oct 24 cut market cap and raised fees but increased yields for stability pool stakers.

Floki to launch TokenFi platform targeting the trillion-dollar RWA narrative.

dYdX Chain's alpha mainnet initiated its V4 transition, distributing USDC fees to validators and stakers via Cosmos x/distribution.

3️⃣ Market overview

Bitcoin surged past $35k on speculation of ETF approval after BlackRock's spot BTC ETF was listed on DTCC. CME bitcoin derivatives open interest hit record highs. A court mandated SEC review Grayscale's bitcoin ETF application.

Bitcoin's price soared past $35,000 after speculation around a spot bitcoin ETF approval. This follows BlackRock's spot bitcoin ETF being listed on the DTCC earlier in the week.

Open interest for bitcoin derivatives on the CME hit an all-time high of 100,000 BTC, signaling growing institutional interest in bitcoin as the ETF conversation heats up.

A court mandated the SEC to review Grayscale's spot bitcoin ETF application after ruling the SEC's initial denial was "arbitrary." Grayscale has since filed for a GBTC spot bitcoin ETF listing.

US Q3 GDP growth beat expectations at 4.9% annually, driven by consumer spending and exports. This puts some pressure on the Fed to maintain tight policy. Markets are pricing in steady rates in November but a 20% chance of a December hike.

Macroeconomy exhibits signs of strength but also uncertainty, with central banks carefully calibrating interest rates while monitoring risks of slowing growth and moderating inflation. Equity markets face volatility amidst the evolving economic landscape.

The US economy showed strong growth in Q3 2023, expanding 4.9% and exceeding expectations. This was driven by robust consumer spending and marks the fastest pace of growth in nearly 2 years. However, business inventory contributions are expected to decline in Q4.

The Federal Reserve is considering interest rate decisions amidst the resilient GDP growth, which underscores the continued strength of the economy despite rising rates impacting some sectors.

The ECB maintained its key interest rate at 4%, ending a sequence of 10 successive hikes, due to concerns over slowing eurozone economic expansion and falling inflation. Further rate hikes are not ruled out.

Treasury yields continued climbing this week, topping 5% on the 10-year. This is weighing on equities, with the S&P 500 down 1.5% this week.

US stock indices retreated, with the S&P 500 falling to its lowest level since May, nearly 10% off its July peak. Meta, Dow Jones, NASDAQ, and S&P 500 all declined, though IBM and Amazon shares rose based on earnings.

4️⃣ Key Economic Metrics

🔴 Markets remain sensitive to Fed policy, economic data, and geopolitical events. An end to yield curve inversions may signal recession risk is rising. New volatility in markets amid uncertainty and new information on the economy, Fed policy, and geopolitical events.

The 10-year breakeven inflation rate hit a high not seen since March, indicating rising inflation expectations.

10-year Treasury yields briefly topped 5% for the first time since 2007, reflecting concerns.

Fed Chair Powell hinted rates may not rise at the next FOMC meeting, acknowledging markets are helping the Fed's goals. His comments likely lifted inflation expectations.

Recent strong economic data like retail sales and jobless claims also suggest persistent growth and inflation, further boosting yields.

Investors are monitoring Middle East tensions for potential larger conflict and supply shocks, though oil prices remain stable.

Inverted yield curves historically precede recessions, but financial conditions remain relatively benign for now

🟢 Better-than-expected retail sales provides a mixed picture - consumer strength endures but faces headwinds, and the economy appears resilient but slowing ahead. Retail sales strength reinforced expectations the Fed will sustain higher rates for longer given the economy's resilience.

Retail sales in September exceeded expectations, growing 0.7% month-over-month and 3.8% year-over-year. This led to higher GDP growth forecasts for Q3.

Sales were strong in categories like auto, drugstores, nonstore retail, and food services. But housing-related categories like electronics, appliances, and furniture lagged due to weakness in the housing market.

The strength suggests consumer spending remains healthy despite tight monetary policy, likely helped by employment gains, rising wages, and confidence.

However, other data like declining credit card transactions had led to lower retail sales expectations. The discrepancy suggests flaws in some data or more cash transactions.

There are potential headwinds like resumed student loan payments, rising credit card debt and delinquencies, and uncertain oil prices.

While Q3 GDP forecasts rose on strong retail sales, pessimism remains about Q4 growth.

🟢 Robust household balance sheets have provided spending support, but the tailwind from rising wealth may fade as the Fed tightens financial conditions. Going forward, declining asset prices may dampen the wealth effect on spending. But accumulated savings and strong labor market may offset this impact.

The latest Federal Reserve survey shows a dramatic 37% increase in US household net worth from 2019 to 2022, the largest 3-year gain since the survey began in 1989.

Household net worth exceeded pre-financial crisis levels for the first time since 2007, driven by surging equity and home prices during 2020-2022.

Wealth grew substantially across all age groups, races, income levels and employment types, except the self-employed.

This wealth surge helps explain strong consumer spending despite declining real wages, as households tapped into increased assets and borrowing.

Healthy household balance sheets are a key reason the US economy has been resilient amid tightening monetary policy.

The growth in household wealth was broad-based, providing a buffer for consumer spending. But the Fed's tightening policies have started reversing asset price gains.

5️⃣ China Spotlight

🟢 While China's economy shows signs of bottoming out, challenges persist in sustaining momentum and reaching full potential. Policy support continues to be critical

China's GDP grew 4.9% in Q3, exceeding expectations of 4.5%. Growth in the first three quarters was 5.2%. If Q4 growth reaches 4.4%, China will meet its 2022 target of "around 5%". This would still mark a significant slowdown from recent years.

Growth was driven by fixed asset investment and consumer spending. Retail sales improved to 5.5% growth in September.

However, property investment remains a drag, down 9.1% this year. Trade has stabilized after sharp declines.

Headwinds persist - complex external environment, weak domestic demand, shaky foundations. Forecasts see 2023 GDP around 5.1%, 2024 at 4.5%.

Beyond GDP, September retail sales rebounded in categories like apparel, jewelry, food. But home-related sales still declined.

Fixed investment rose just 3.1% in Jan-Sep, the slowest in years, dragged by weak private and property investment.

But manufacturing investment grew 6.2%. Industrial production was stable at 4.5% growth. Pockets of strength persist.

Overall, data indicates some improvement, but stabilization at a slower trend growth rate amid ongoing headwinds. Property and external risks remain.

🔴 Persistently weak inflation and trade reflect soft demand, global headwinds, and souring relations. While September data was less bad, the overall picture points to lingering weakness in the Chinese economy.

China's consumer inflation remains extremely low, with prices unchanged in September versus a year earlier. This reflects weak demand and excess capacity.

Food prices fell 3.2%, driven by a 22% pork price decline. This offset rising energy costs. Core inflation was just 0.8%.

Producer prices fell 2.5% annually in September, further evidencing weak demand and oversupply.

On trade, September exports fell 6.2% annually, an improvement from the 8.8% drop in August. Exports have declined in 10 of the last 12 months.

The export slump reflects weakening global growth, worsening relations with the US and Europe, and supply chain shifts away from China.

Imports also fell in September, by 6.2%, but at a slower pace than August's 7.3% decline, marking 8 straight months of import drops.

Commodity imports like copper fell on lower prices and weak domestic demand, though oil imports rose.

Bilateral trade was especially weak with Southeast Asia, the US, EU, Japan and Taiwan. Trade improved with Russia.

Twitter: https://twitter.com/arndxt_xo/status/1718224348937601457