Bidenomics is working.

Vultures “Goldrush” into ETFs

Unveiling Macro Mayhem, Bitcoin Buzz, Fed's Policy Navigation! 🌍🧵

Macro Pulse Update 30.06.2023, covering the following topics:

1️⃣ Macro events for the week

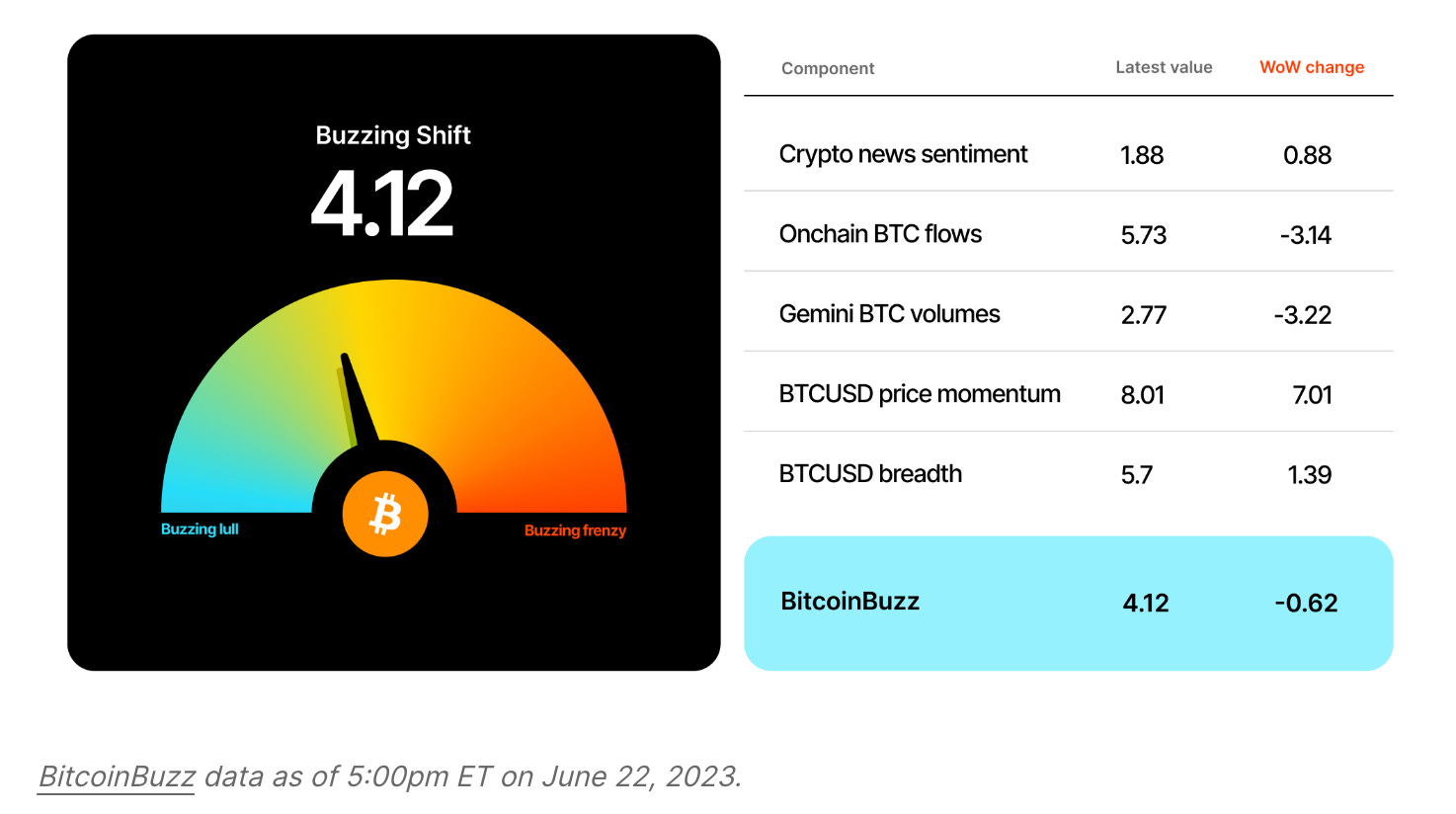

2️⃣ Bitcoin Buzz Indicator

3️⃣ US Economic Indicators

4️⃣ Bank of England Tightens Further

5️⃣ Navigating through the Fed’s Monetary Policy

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

2️⃣ Bitcoin ETFs 🟢

Bitcoin’s developments reflect the ongoing evolution of the crypto landscape. It is evident that the vultures of traditional finance's desire a share in this lucrative crypto pie.

In lieu of Blackrock’s ETF filing, which undoubtedly stirred the market, here is what we saw happen:

Bitcoin (BTC) rallied past $30K, driven by the excitement surrounding bitcoin exchange-traded fund (ETF) filings by major financial institutions like BlackRock, Invesco, WisdomTree, and Valkyrie. If approved, BTC ETFs would offer retail traders an opportunity to invest in BTC on major U.S. exchanges.

BTC dominance rose to over 51%, its highest level since April 2021, leading a crypto rally where altcoins like Ether (ETH) also surged, surpassing $1,900 USD.

To address the SEC’s concerns, ETF applicants like BlackRock are including Spot BTC Surveillance-Sharing Programs in their applications. This agreement aims to enhance surveillance of BTC markets, a factor that previously hindered the approval of bitcoin ETFs.

Key dates and timeline for the BlackRock Spot Bitcoin ETF

3️⃣ US Economic Indicators

JP comments at the FOMC emphasized the possibility of further rate hikes this year to address persistent inflation concerns. I would expect the central banks to remain vigilant in its efforts to keep inflation in check.

The US economy demonstrated resilience by surpassing growth expectations, with a solid 2% growth in first-quarter GDP. This indicates a healthier economic landscape than initially projected and reiterates the modest pace of economic expansion. Consumer spending is resilient, suggesting that further policy actions may be needed to achieve the 2% inflation target.

Q1 GDP growth was just revised up to 2%

🟢 Initial jobless claims came in slightly lower than expected, reflecting a positive trend in the labor market and signalling potential stability and growth in employment.

🟢 Housing market signalled that it was relatively healthy despite higher interest rates. Single-family starts saw a notable jump, while multifamily starts also surged. Existing home sales showed a slight increase in May, with sales rising for condos and co-ops while declining for single-family homes. The affordability migration away from high-cost housing markets continues to drive overall demand.

🔴 The Leading Economic Index (LEI) declined for the 14th consecutive month in May, mainly due to weakness in the manufacturing sector and consumer sentiment. While there were improvements in building permits and jobless claims, the LEI suggests a potential mild recession early next year.

🟢 Major US financial institutions, including Bank of America, JPMorgan Chase, Goldman Sachs, and Wells Fargo, experienced notable stock gains after successfully passing the Federal Reserve's stress test. However, cautious payout strategies may be employed due to ongoing regulatory considerations.

These highlights the need for continued attention to inflation, the resilience of the housing market, and the possibility of economic challenges in the future.

In summary Bidenomics is working as we see good metrics

4️⃣ Bank of England Tightens Further 🔴

Bank of England's responds to high inflation and developments in global central bank policies.

BOE surprised markets by raising its key interest rate to 5% in an effort to tackle stubborn inflation. This decision, the highest interest rate level since April 2008, comes as the UK struggles with double-digit inflation percentages.

With expectations of high inflation and the need for further action, it is anticipated that the Bank of England will deliver another 50 basis points rate increase to 5.50% in August and an additional 25 basis points hike to 5.75% in September, marking the peak of the current cycle.

Despite the rate hike, the British Pound (GBP) fell against the U.S. dollar (USD), highlighting economic concerns overshadowing the impact of higher interest rates.

Additionally, central banks worldwide were active, with rate hikes by the Swiss National Bank and Norway's central bank. Turkey's central bank's rate hike fell short of market expectations. Several other central banks held their policy rates steady.

BOE raised rates

5️⃣ Navigating through the Fed’s Monetary Policy 🟡

Some key factors that shape the central bank's decisions as the Fed continues to navigate monetary policy in response to economic conditions are:

Fed is committed to bringing inflation back to its 2% target and has suggested that the tightening of monetary policy may not be over yet.

Powell will assess the cumulative impact of previous tightenings.

While economic activity has continued to expand at a moderate pace, the manufacturing and housing sectors have weakened. However, consumer spending remains strong, and the labor market is robust.

The Fed has achieved its maximum employment mandate but has fallen short in maintaining low and stable inflation. Powell emphasized the need to focus on inflation now to achieve sustained strong labor market conditions in the long run.

The dot plot released on June 14 indicated that most FOMC participants expect further interest rate increases by the end of the year. However, future decisions will be based on incoming economic data.

In terms of banking regulations, changes to capital requirements are not expected to have an immediate impact on the economy and are not a key factor in the Fed's assessment.

Reference; https://twitter.com/arndxt_xo/status/1674779647358439425