Fed throws curveball

UK inflation falls, and Japan's inflation woes continue

Here are 4 factors you need to keep up with market mania 👇🧵

Macro Pulse Update 30.09.2023, covering the following topics:

1️⃣ Macro events for the week

2️⃣ Bitcoin Buzz Indicator

3️⃣ Market overview

4️⃣ Key Economic Metrics

5️⃣ Japan Spotligh

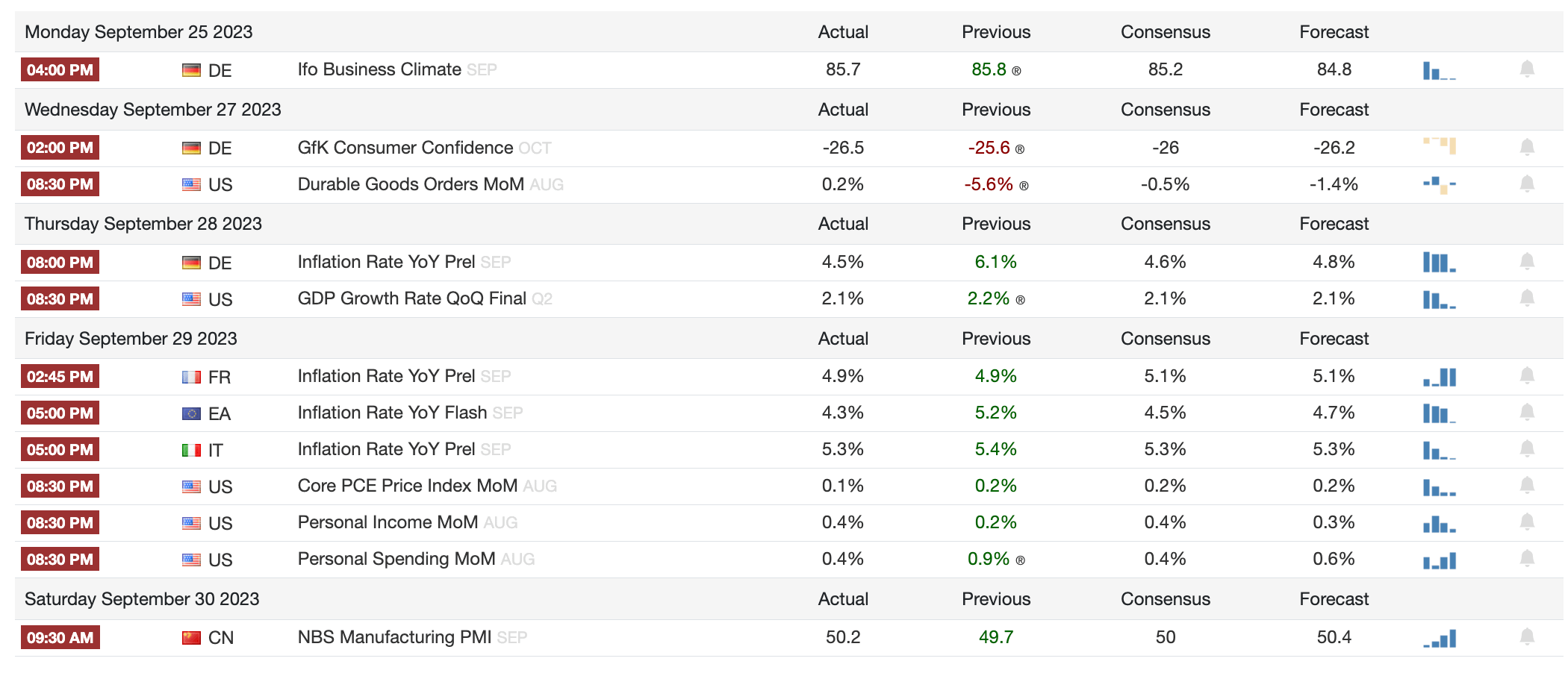

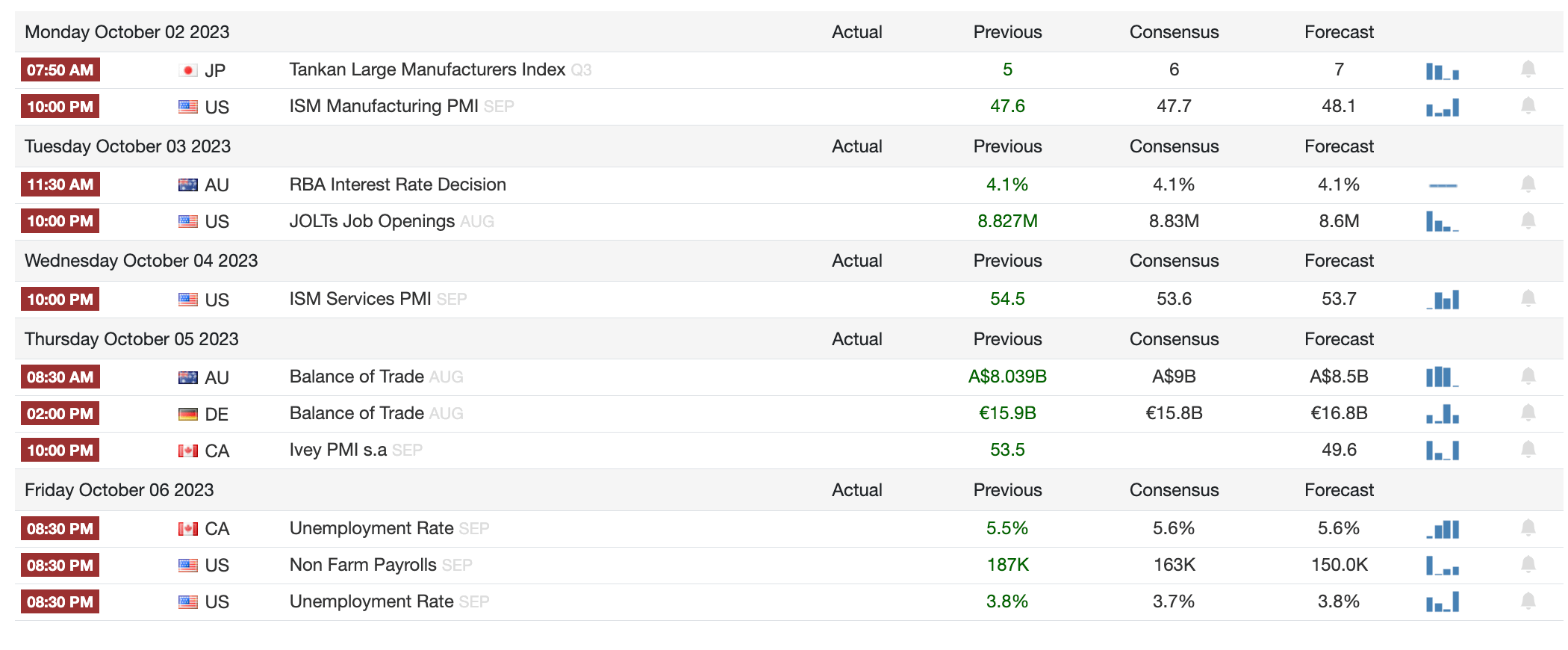

1️⃣ Macro events for the week

Last week

Next week

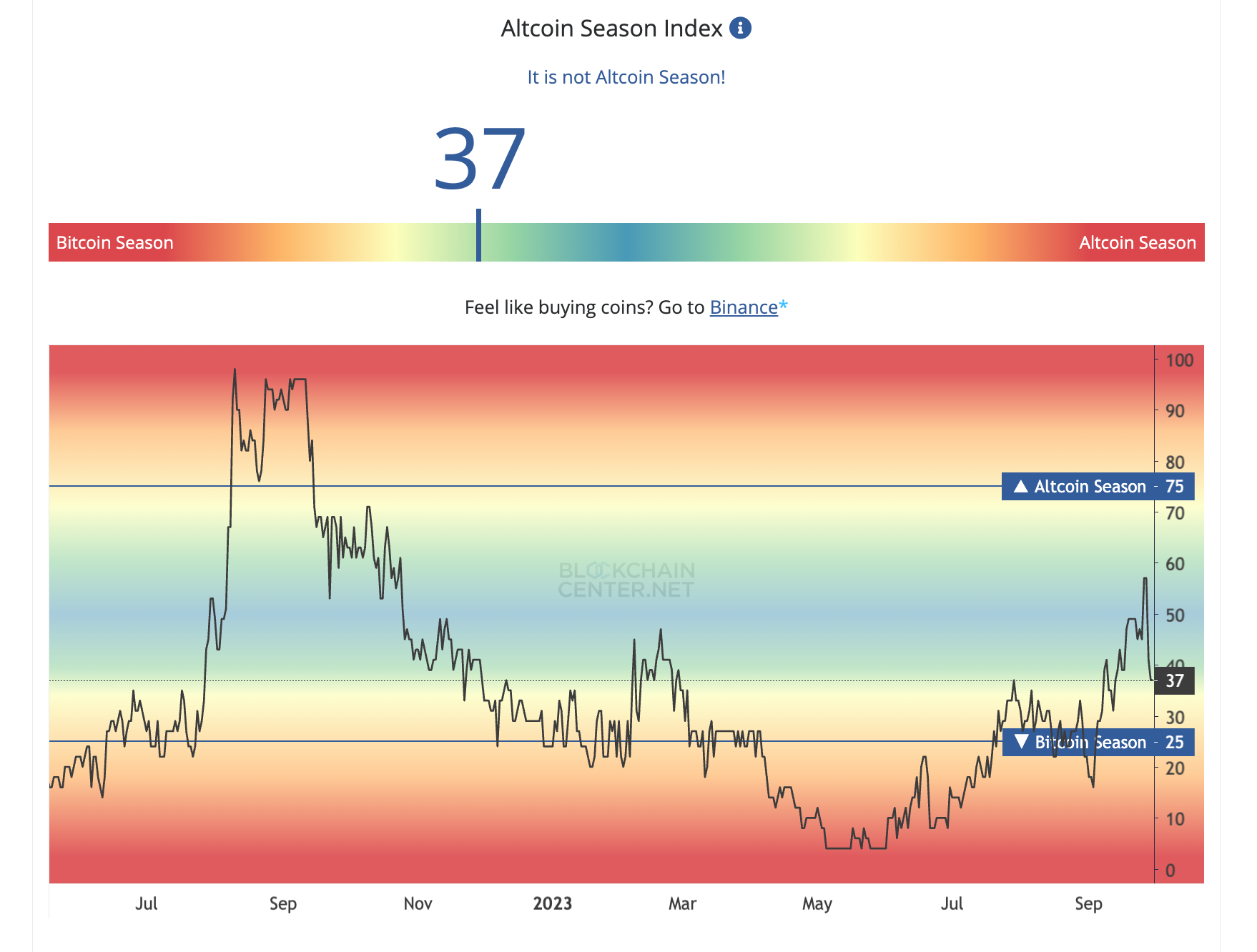

2️⃣ Bitcoin Buzz Indicator

Regulatory and Financial Landscape

VanEck's Ethereum ETF Ambitions and SEC Delays

Uncertainty Surrounds SEC's Bitcoin ETF Decisions

Project Mariana Tests DeFi for Central Bank Digital Currencies

HTX Exchange Cyber-Raid: A Lesson in Crypto Security

Crypto Exchanges and Platforms

Coinbase's Multi-Front Strategy to Dominate Crypto Market

WOO X and OpenTrade: Tokenizing U.S. Treasury Bills in Asia

Gemini Exits Netherlands Due to Regulatory Constraints

Ripple's Abandoned Acquisition of Fortress Trust

Binance Faces Regulatory Headwinds and Market Share Decline

Banking Updates

MoneyGram's Leap into Crypto with Non-Custodial Digital Wallet

UK Banks Clamp Down on Crypto Transactions

Market Trends and Investments

MicroStrategy's Latest Bitcoin Investment: Bullish or Risky?

NFTs and Digital Assets

Pudgy Penguins: From NFTs to Walmart Shelves

PayPal Ventures into NFTs with New Patent Application

The Rollercoaster Ride of NFT Market Valuations

Industry Challenges and Shifts

Epic Games Cuts Staff Amid Metaverse Revenue Struggles

Altcoins

CoinShares opened a U.S. hedge fund division for institutional clients.

Amazon poured $4B into Anthropic AI.

Taiwan set guidelines for regulating digital assets and crypto.

Microsoft's leaked plans hinted at Xbox crypto wallets.

Binance Japan and Mitsubishi partnered for stablecoin creation.

Immunefi rolled out smart contract bug-bounty vaults.

Uniswap Foundation sought $62.37M for ecosystem expansion.

Gemini shifted $282M from Genesis to safeguard users.

GMX awarded Collider's research arm a $1M bug bounty.

Kraken mulled exploring stocks.

PEPE surged 30% in a week due to crypto sector rebound and whale action.

FTX founder's trial set for a 6-week span.

Optimism's OP token dipped 10% before $30M token unlock.

81 Binance wallets moved $31M in LINK, Chainlink broadens to Coinbase.

Base eclipsed Solana as total value locked neared $400M.

Mixin Network suffered $200M loss; offered $20M bug bounty for fund return.

Terra Classic voted to cease USTC token minting.

Fake Aptos tokens caused Upbit to halt APT withdrawals.

Hashkey HK launched AVAX trading with a $1M portfolio prerequisite.

PayPal collaborated with Crypto.com to amplify PYUSD adoption.

Six-week crypto outflow streak; XRP and SOL win investor trust.

MakerDAO hit a 16-month high, surging 200% YTD due to rising revenue.

IOTA Network introduced ShimmerEVM's smart contracts and tokens.

Arbitrum shed $59M in unclaimed airdrop tokens.

Curve's founder put $35M in CRV to settle Aave debt.

Celestia airdropped 60M tokens to grow its network.

DFINITY rolled out a $20M ICP Asia Alliance Web3 incubator.

3️⃣ Market overview

There is economic strength in the U.S., but with inflation persisting as a key risk that could lead to further Fed tightening. Meanwhile, early signs of easing inflation in Europe may allow the ECB to pause rate hikes. Equity markets continue to closely track yields, economic data, and corporate earnings.

The U.S. economy continues to exhibit strength, with robust GDP growth in Q2 and expectations for further expansion in Q3. However, risks remain from potential government shutdown and auto strikes impacting supply chains.

Despite strong labor market data, the Fed may consider another rate hike soon to address lingering inflation concerns. This is in contrast to cooling inflation in Europe, which may allow the ECB to maintain interest rates.

U.S. stocks advanced this week, aided by falling bond yields. Tech stocks saw gains, while Accenture declined on disappointing earnings. Markets await important U.S. inflation data today.

4️⃣ Key Economic Metrics

🔴 Fed is striking a less dovish tone by signaling an extended period of restrictive policy to ensure inflation continues gradually downhill. Rates unlikely to fall until late 2024 at the earliest.

The Fed left interest rates unchanged but signaled rates will remain elevated for longer to suppress inflation.

FOMC median projections point to likely one more rate hike this year, keeping rates around 5.6% in 2023.

Rates expected to stay elevated through 2024, only coming down late in the year as inflation declines.

FOMC members more optimistic on economic growth for 2023 and 2024 versus previous projections.

Fed sees inflation gradually declining but remaining above target, necessitating prolonged high rates.

Goal is to weaken labor market and wage growth to further reduce inflationary pressures.

Markets reacted with higher short-term yields and a stronger dollar, signaling expectations of persistent inflation and high rates.

🔴 Q4 has multiple risks that could noticeably slow growth versus the strength expected in Q3. Key factors to watch are energy prices, policy impacts, labor disputes, and pace of consumer spending

Q3 GDP expected to show strong growth, but Q4 looks more troubling.

Lagged impact of past tightening, return of student loan payments, potential government shutdown, and auto strikes could hamper Q4 growth.

Especially worrying is rebounding oil/gas prices, which could further curb consumer spending and stoke inflation higher. Might spur more Fed tightening.

Return of student debt payments will reduce discretionary income by $100B annually, but this is small relative to total consumer spending.

Loan repayment programs will reduce monthly payments for many borrowers, offsetting the impact. Job and wage growth also helps consumer resilience.

🟡 Cooling UK inflation taking some pressure off BOE to keep hiking aggressively. But persistent core inflation and close committee vote suggest the BOE could resume tightening if inflation persists.

UK inflation eased to 6.7% in August, down from 6.8% in July, the lowest since February 2022. But core inflation remains sticky at 6.1%.

Declining inflation led investors to lower expectations for further BOE tightening.

The BOE kept rates steady at 5.25% after the inflation data, with a close committee vote 5-4. Signals potential pause in tightening.

BOE decision contrasts expectation that the Fed will hike again this year. Market still sees some chance of another BOE hike.

Pound declined further as rate differential between UK and US expected to widen with less BOE tightening.

Falling pound also reflects view that UK growth will lag US near-term.

5️⃣ Japan Spotlight 🔴

Japan faces persistent inflation above target but a reluctant central bank wary of hurting growth. Weak yen poses challenges.

Core inflation remains elevated at 3.1% in August, with core-core at 4.3%, showing sticky inflation at higher than normal levels.

Inflation driven more by goods prices than services. Wages lagging inflation leads to declines in real household earnings.

BOJ views inflation as supply-driven and transitory, so is maintaining easy monetary policy despite inflation exceeding target.

Yen has weakened as markets doubt BOJ will tighten policy. Hurts purchasing power for imports/travel but helps exports.

Economic indicators like PMIs suggest slowing growth and weakening demand ahead. Likely reinforces BOJ's stance.

Twitter: https://twitter.com/arndxt_xo/status/1708076738482475358