The AI Storage Supercycle: 16 Memory/Storage Underpriced Stock Picks

Infrastructure, Semiconductors, Memory

The thesis is simple, AI generates more data than the world has ever seen, and all of it has to live somewhere.

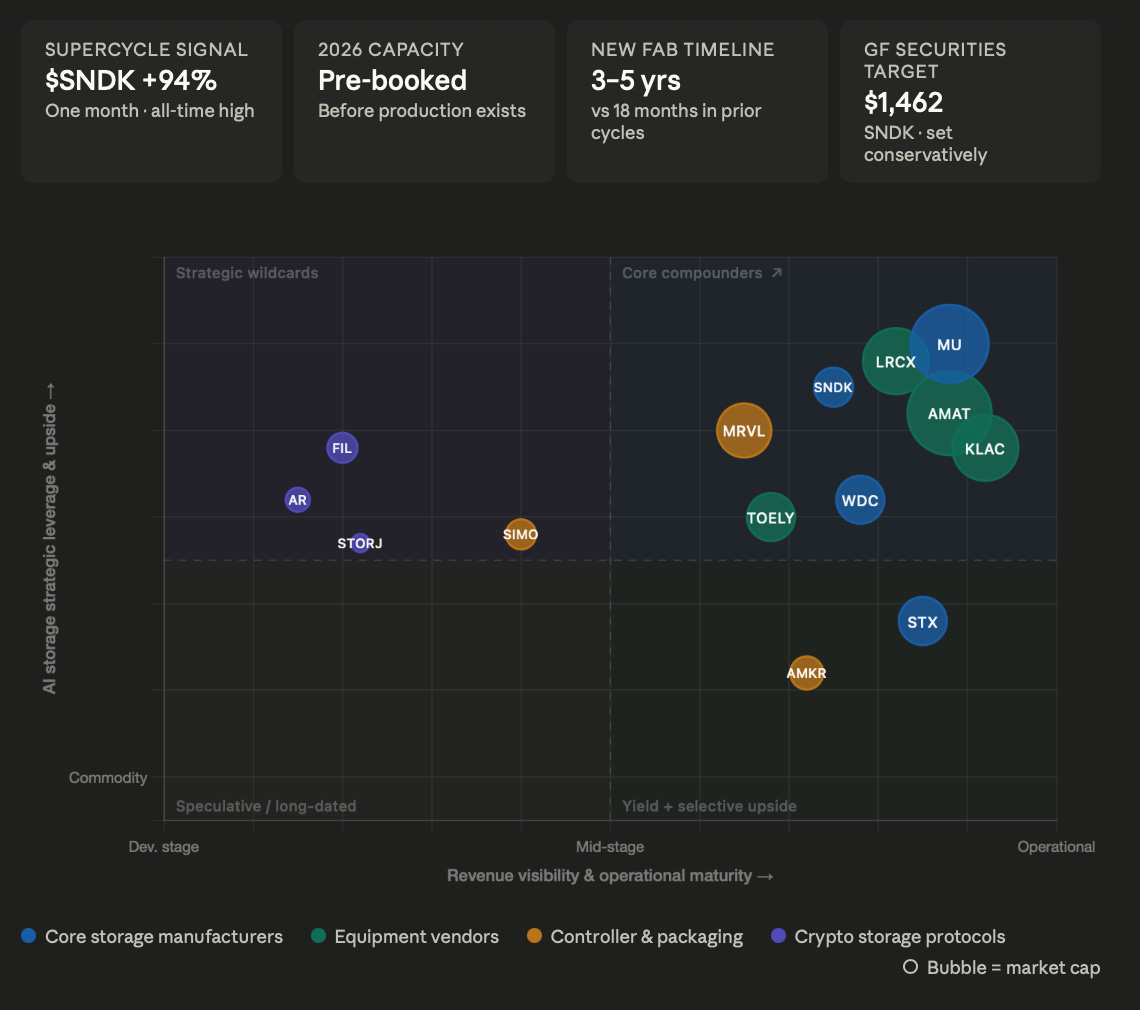

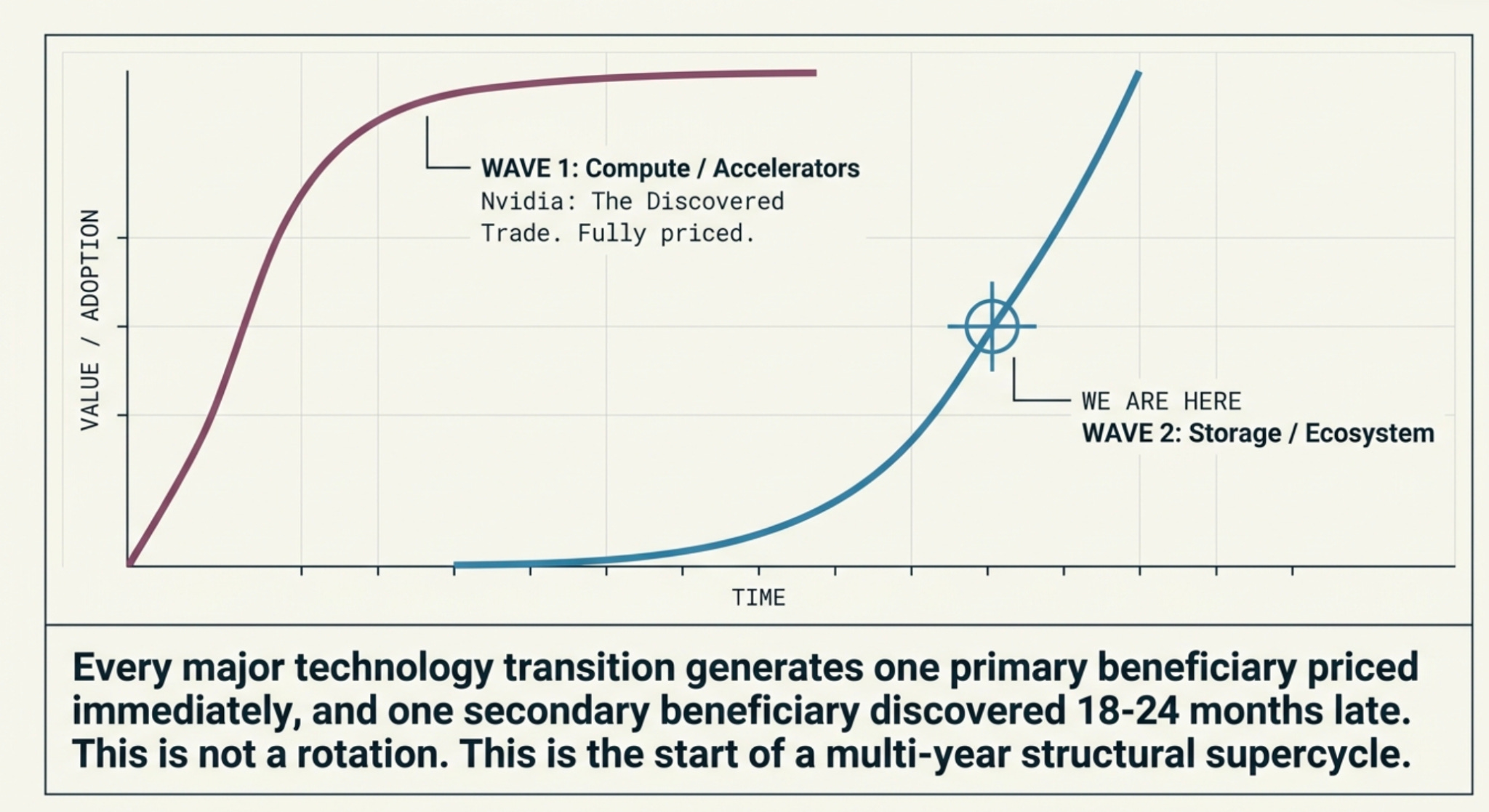

Every major technology transition generates one primary beneficiary that the market prices immediately, and one secondary beneficiary that the market discovers 18-24 months late. In the AI cycle, Nvidia was the primary beneficiary. The world understood this early and priced it aggressively. The secondary beneficiary, the one the market is only now waking up to, is storage. SanDisk up 94% in a month.

Micron holding its breakout while Nvidia sells off. Western Digital and Seagate in full send. 2026 capacity pre-booked before the year has started.

This is a supercycle with structural characteristics that have no precedent in the prior three storage cycles of 2010, 2014, and 2017. This article lays out the thesis in full: why this cycle is different, what the right vehicles are across the stack, and where the market is still leaving opportunity on the table.

The Macro Thesis: Why This Cycle Doesn’t End Like the Others

Storage supercycles have a consistent anatomy. Demand spikes from a new consumer device category:

the smartphone in 2010

the streaming explosion in 2014, the gaming and

PC refresh cycle in 2017.

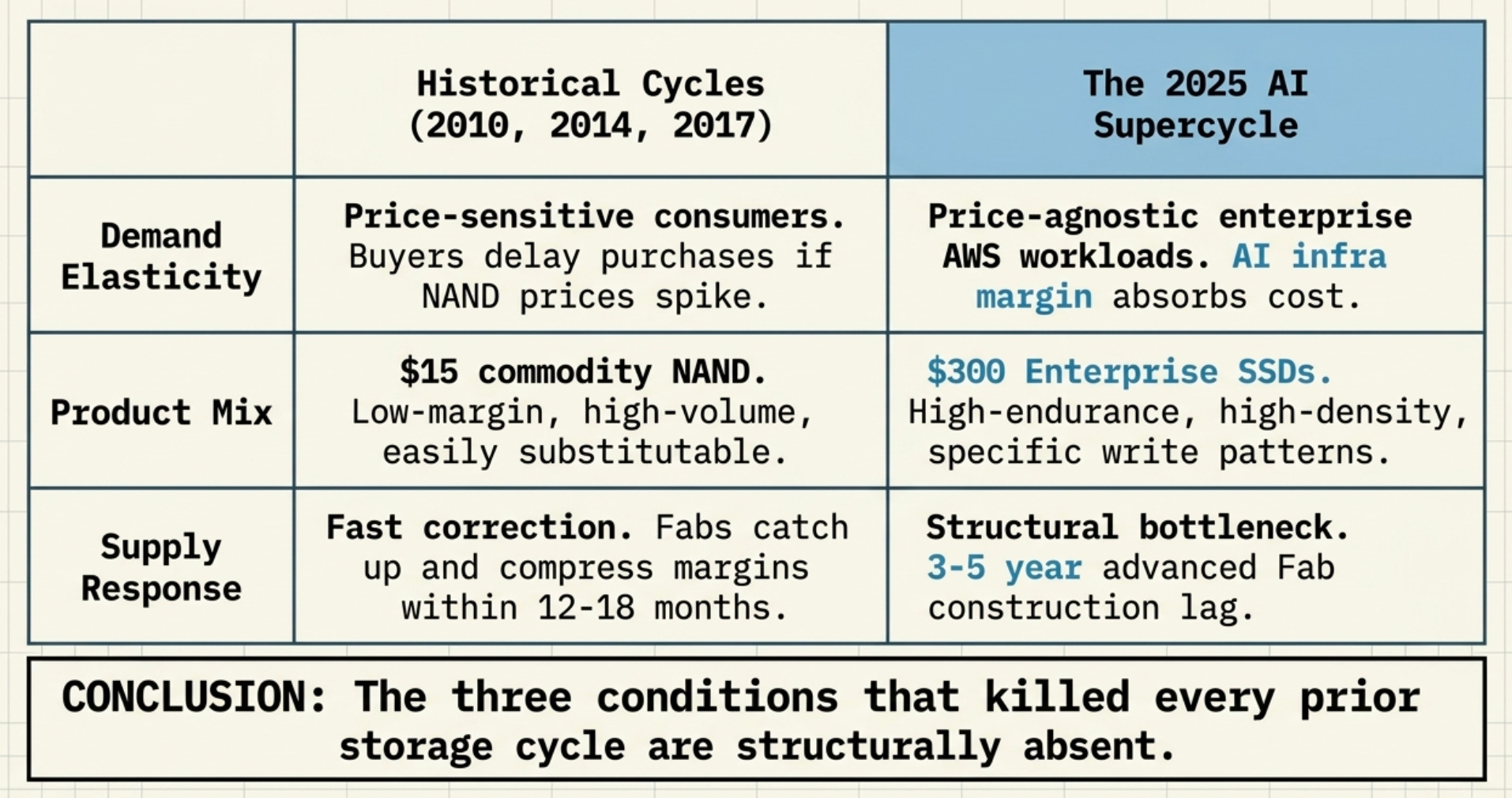

Supply scrambles to catch up. Within 12-18 months, new NAND fab capacity comes online, margins compress, and the trade unwinds. Every cycle ended the same way: supply caught demand, and the manufacturers went back to fighting over commodity pricing.

Three structural differences make 2025-2027 categorically different.

First: demand is price-inelastic for the first time.

When a consumer buys a phone with 256GB of storage, they are deeply price-sensitive. If NAND prices spike 40%, they buy less storage or wait a cycle. When AWS pre-books 2026 enterprise SSD capacity for AI infrastructure, the conversation about price never happens.

The margin on selling AI compute to enterprise customers absorbs a 40% NAND price increase without blinking. The hyperscaler CFO’s fear is not overpaying for storage, it is not having storage when the AI workload demands it. That inverted incentive structure has never existed in a prior storage cycle.

Second: product mix has permanently shifted upmarket.

Prior cycles were built on commodity NAND, low-margin, high-volume, easily substitutable. AI workloads require high-density, high-endurance enterprise flash with specific write patterns, sustained random read throughput, and power efficiency profiles that commodity NAND cannot meet.